Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Accounting Cycle 101

Track your business's financial data to spot discrepancies and ensure fiscal health.

Written by: Dachondra Cason, Senior WriterUpdated Feb 02, 2026

Editor Verified:

Editor Verified

A business.com editor verified this analysis to ensure it meets our standards for accuracy, expertise and integrity.

Sandra Mardenfeld,Senior Editor

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Financial tracking is vital to business success because it helps business owners understand and monitor their financial health at all times. Proper financial oversight requires an understanding of the accounting cycle. When you create and adhere to a consistent accounting cycle, you’ll have organized, easy-to-read financial data that external parties, such as investors, can interpret quickly.

The accounting cycle tracks each transaction from the moment of purchase to the point it’s added to a financial statement. This eight-step process, often completed with the help of accounting software, monitors your inflows and outflows and summarizes them in periodic financial statements. A consistent accounting cycle makes it easier to spot discrepancies at a glance. We’ll explain the accounting cycle and break down the eight-step process.

Editor’s note: Looking for the right accounting software for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

What is the accounting cycle?

The accounting cycle is an organized set of steps for identifying and maintaining transaction records within your company. This process typically involves a bookkeeper or accountant who documents, categorizes and summarizes each transaction your business makes during a given period. The time frame of an accounting cycle can vary based on factors unique to each business. However, most business owners start a new accounting cycle annually.

Once the accounting period ends, the books are closed and financial statements detailing the captured information are created. These financial statements are shared with company stakeholders and relevant government agencies.

The accounting cycle “ensures that all financial activities are accurately captured and reported in the company’s financial statements,” said Paul Ursich, partner-in-charge of advisory services at Wiss. “The steps include identifying transactions, recording them, posting to the ledger, preparing a trial balance, making adjustments, preparing financial statements, and closing the books.”

Many businesses automate the accounting cycle with software to minimize the accounting mistakes that can occur when businesses process financial data and track business assets manually.

Did You Know?

The top accounting challenges small businesses face include staying on top of cash flow, covering unexpected expenses and classifying employees correctly.

Accounting cycle vs. budget cycle

The accounting cycle is often confused with a budget cycle. While they utilize similar data, they serve distinct functions in your company’s timeline.

Accounting cycle: The accounting cycle is the systematic process of recording, processing and summarizing financial transactions within a specific accounting period (typically monthly, quarterly or annually). Businesses use the accounting cycle to review their past financial activity and assess their overall performance.

Budget cycle: The budget cycle is different because it focuses on budget planning and financial resource management for future periods, and it usually covers a fiscal year. “It includes setting financial goals, creating budgets, monitoring performance and making adjustments to ensure that the organization stays on track financially,” Ursich explained. Budget cycles also include revenue forecasting and expense allocation.

In short, the accounting cycle looks backward, while the budget cycle looks forward. Adherence to a budget cycle enables businesses and governments to make strategic financial decisions, control costs and ensure that funds are used effectively.

8 steps of the accounting cycle

The accounting cycle consists of eight sequential steps.

The exact steps of the accounting cycle may vary according to a company’s unique needs. However, the following process for tracking activity and creating financial statements doesn’t change. Here’s a breakdown of the eight-step cycle.

Accounting Cycle 101

Identify the transactions

Record the transactions

Post the transactions

Prepare a trial balance

Fix any errors

Add the adjusting entries

Create your financial statements

Close the books

1. Identify the transactions.

The first step of the accounting cycle is to identify each transaction that creates a bookkeeping event. Bookkeeping events are sales, refunds, bill payments from accounts payable, and any other financial transactions in your business.

“Although this step sounds simple and somewhat mundane, it is one of the most critical steps of the accounting cycle,” said Ashford Chancelor, practice manager and consulting chief financial officer at vcfo. “Identifying transactions and classifying them correctly in this initial stage is a key step that will reduce the time needed in the reconciliation and review stages before the financial statements are issued.”

In accounting, transaction types include cash, noncash and credit events. Transactions can be identified through invoices, receipts and other documents that record business activity.

“For many companies, cash receipts and disbursements comprise a significant portion of the transaction volume,” Chancelor explained. “To facilitate accurate and swift identification, many companies will establish specific email addresses to which vendors will send invoices to be paid or separate bank accounts to receive payments for a pred

Next, document each transaction as a journal entry. Also known as the “book of original entry,” this is the book or spreadsheet where all transactions are recorded first.

Each entry should list details about every transaction in chronological order. If your company uses double-entry accounting, the details will include a debit and credit for each transaction. This method makes it easier to track how events affect your finances.

3. Post the transactions.

After you enter transactions into the journal, the next step is to post them to your general ledger. Posting transfers these chronological journal entries into the general ledger, where they are reorganized by account type.

Transactions posted to the general ledger should be separated into five key accounts:

Assets

Liabilities

Capital

Expenses

Income

These categories make it easy to find transactions quickly. However, if debits and credits aren’t balanced, it’s a sure sign your financial statements won’t be accurate.

4. Prepare a trial balance.

Once journal entries are posted to the appropriate general ledger accounts, it’s time to prepare an unadjusted trial balance. This document is used to review account balances and verify that the total debits and credits in the ledger are equal.

“A trial balance is an accounting report that lists the general ledger account balances at a specific time,” Chancelor said. “It is used to generate the balance sheet, income statement and statement of cash flow and is also a primary control used to ensure that the total debits equal the total credits. A trial balance helps identify errors in the general ledger before financial statements are prepared.”

To create an unadjusted trial balance, list all general ledger account balances before you make any adjusting entries. You can use the trial balance to generate basic financial statements without sorting through the general ledger. Although this can be done manually, the trial balance step is built into most accounting software platforms.

5. Fix any errors.

This step becomes essential when your trial balance’s debits and credits don’t match. To locate the issue, compare the questionable entries to the original journal entries in your spreadsheet or accounting software.

One common mistake is posting to the wrong account. In these cases, the debits and credits may still balance, but the account’s activity might look unusual. During this step, you’ll investigate and make any necessary adjustments.

FYI

The best spreadsheet software can track invoices and wages as well as offer predictive analytics to help you make informed business decisions.

6. Add the adjusting entries.

As you approach the end of the accounting period, you’ll need to add adjusting entries to your journal. These end-of-period adjustments ensure your accounts reflect the correct expenses and revenues for that specific period.

Adjusting entries typically include prepayments, accruals and noncash expenses, such as depreciation. This step is especially important for transactions that span more than one accounting period.

7. Create your financial statements.

Now that your adjusting entries are posted, it’s time to prepare an adjusted trial balance and complete your financial statements. The adjusted trial balance lists all ending balances from your general ledger accounts.

Once that’s complete, you can generate your financial statements or annual report. These documents should present your financial information in a simple, organized format. Tax authorities, employees and other stakeholders may review them to understand your business’s financial position.

The three major types of financial statements (or accounting reports) are the balance sheet, income statement and cash flow statement. These reports reflect your company’s financial standing and serve as key indicators of operational performance.

Did You Know?

An audited financial statement is a report reviewed by a certified public accountant (CPA) to ensure it complies with accepted accounting principles and auditing standards.

8. Close the books.

After you prepare your financial statements, it’s time to end the accounting period. This involves using closing entries to finalize your revenue and expense records.

The closing entry process involves transferring your net income to retained earnings. Once that transfer is complete, all temporary accounts — such as revenue and expense accounts — should be closed.

“Closing the books resets revenue and expenses back to zero so that they don’t carry over to the next accounting period,” Chancelor explained. “Net income or loss is transferred to a permanent account that records retained earnings.”

The final step is to prepare a post-closing trial balance to confirm that debits and credits remain in balance before the next accounting cycle begins. Because temporary accounts are zeroed out, the post-closing trial balance will only include balance sheet accounts.

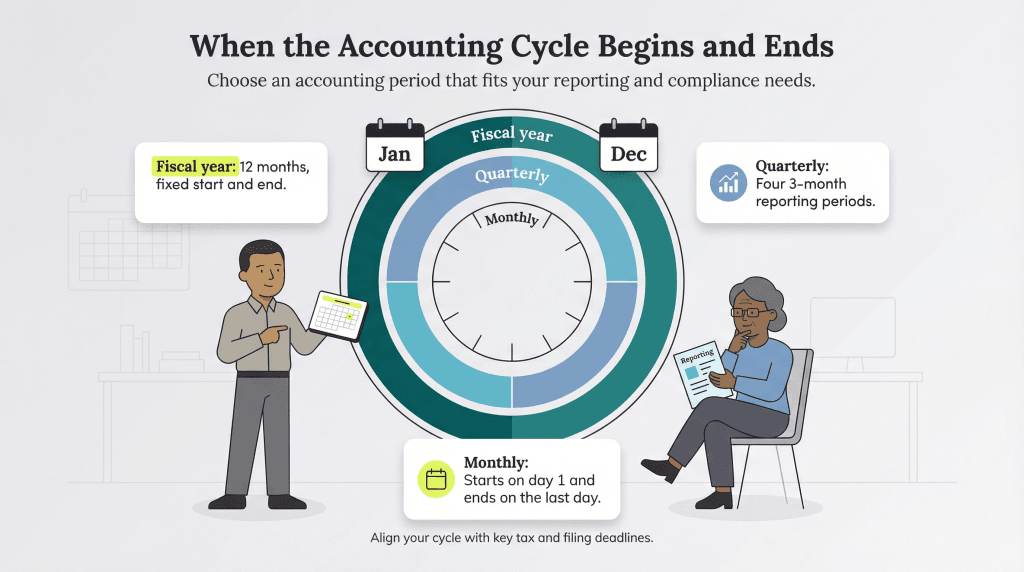

When does an accounting cycle begin and end?

Accounting cycles can vary in length, commonly organized by month, quarter or year.

The accounting cycle time frame is based on the accounting period you choose according to your company’s needs. During this period, financial statements are created and shared. To ensure compliance, many business owners end their accounting cycle annually.

Although annual cycles are common, some businesses opt for accounting periods of three or six months. According to International Financial Reporting Standards, the accounting period can also span 52 weeks. This is known as a fiscal year.

Here’s how Ursich described fiscal year, quarterly and monthly cycles:

Fiscal year: A fiscal year is a 12-month period that can start on any date. For example, if a company’s fiscal year runs from Jan. 1 to Dec. 31, the accounting cycle begins Jan. 1 and ends Dec. 31.

Quarterly: Many companies use quarterly accounting periods that divide the year into four three-month segments. If a company’s year starts Jan. 1, the first quarter would run from Jan. 1 to March 31, the second would go from April 1 to June 30, the third would span July 1 to Sept. 30, and the fourth would last from Oct. 1 to Dec. 31.

Monthly: Many businesses prefer monthly accounting periods for internal reporting and management. In this case, the accounting cycle begins on the first day of the month and ends on the last.

Tip

Consider your financial deadlines when you’re choosing a monthly, quarterly or annual accounting cycle. Many business owners select an annual period that aligns with the U.S. Treasury Department’s financial statement submission dates.

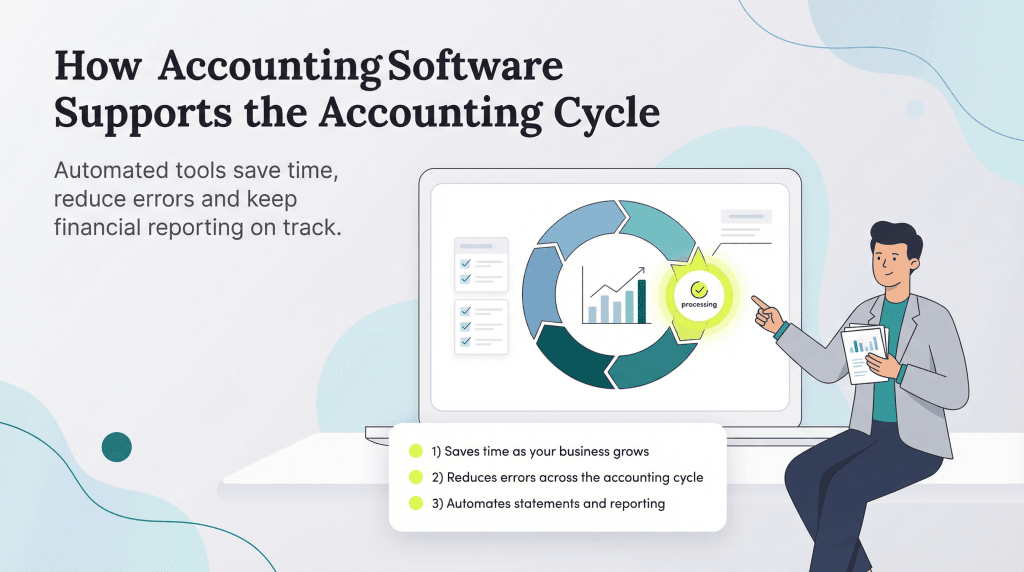

Accounting software and the accounting cycle

Accounting software streamlines the cycle by automating data entry.

Accounting software saves time and effort by automating the entire accounting cycle. As your business grows, you may find that you need more than one person to manage the steps involved. Investing in one of the best accounting software platforms can save time, reduce errors and cut long-term costs.

Even if you hire a CPA or get a bookkeeper to oversee your accounting cycle, you can simplify your responsibilities by choosing the right accounting software. These tools can record business transactions and automatically generate financial statements. A reliable platform also helps your team minimize costly mistakes and stay on track with financial reporting.

Amanda Hoffman contributed to the reporting and writing in this article. Source interviews were conducted for a previous version of this article.

Did you find this content helpful?

Thank you for your feedback!

Share Article:

Written by: Dachondra Cason, Senior Writer

Dachondra Cason is a freelance writer and business consultant in Atlanta, GA. She has over 8 years of professional experience, with a focus on finance and small businesses. Topics she has covered include creating effective business plans, fraud prevention, and digital marketing. She has also written creative content including celebrity cookbooks, plays, and social media campaign material.