Choosing the right employee retirement plan is critically important, but it can also be a complicated and difficult decision. Spend time evaluating each provider and the plans they offer, and don’t be afraid to bring in members of your team and outside professionals to support you during the selection process.

To understand the process even more, we spoke with business owners and leaders about how they went about choosing an employee retirement plan provider and the factors they prioritized along the way.

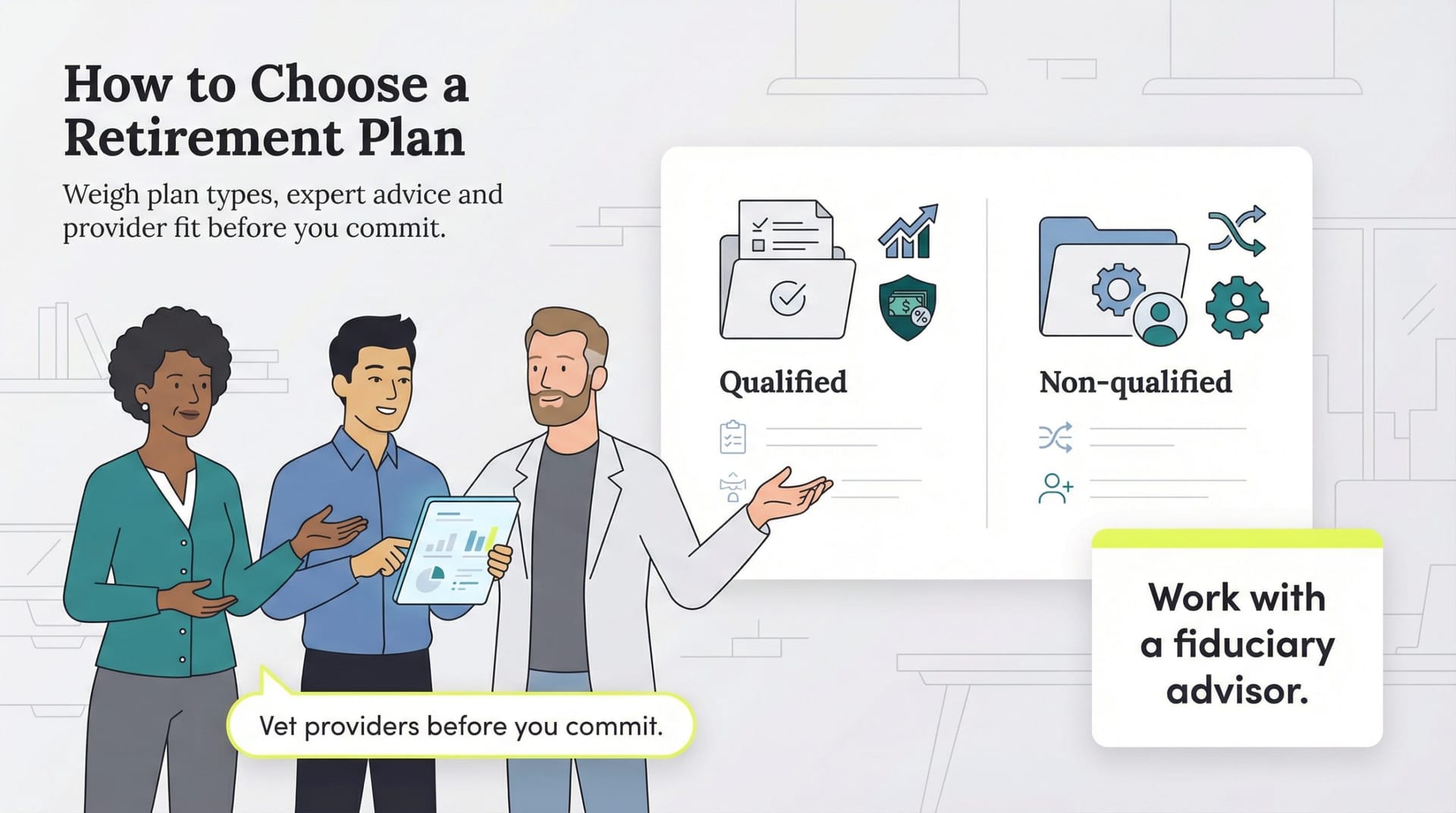

Determine whether you need a qualified or non-qualified plan

Qualified employee retirement plans refer to those qualified for special tax considerations and include familiar vehicles like 401(k)s. They are “qualified” under the Employee Retirement Income Security Act (ERISA) because they meet certain regulatory criteria.

Non-qualified plans are more flexible but do not offer the tax advantages that qualified plans do. They can be offered to a smaller group of employees and custom made to suit their needs. Qualified plans are offered to most employees in the company and come with an inflexible design.

“Identifying the purpose of the plan allows the ability to begin evaluating which type of plan is best suited for your needs,” said Adam D’Acierno, founding partner of Strategic Capital. “For example, a non-qualified plan will have different requirements for coverage and testing than a qualified plan which is more stringent in its requirements.”

Work with a reputable financial advisor

The ins and outs of employee retirement plans can be a lot to wrap your head around, so it’s wise to work with someone who understands the space already. We recommend working with a professional financial advisor who has a proven track record when it comes to managing employee retirement plans.

“The most important piece of advice I would give is to evaluate and identify an independent fiduciary advisor who can show a documented prudent process to help identify your needs, evaluate service providers, assist with implementation and ongoing monitoring of the plan is the most beneficial best practice to follow,” D’Acierno said. “They should be able to educate you at a plan level as well as the participants of the benefits involved in your company’s retirement plan.

Consider the type of plans available

There is a wide range of retirement plans to choose from, and even among certain types of plans there are variations (think traditional 401(k), individual 401(k) and safe harbor 401(k).) Spend time with a financial advisor analyzing all the types of plans and how they differ from one another. Make an educated decision based on the nuances of each plan available, and evaluate providers on whether they offer the best possible plan for your business.

“[We] recommend the company select what is called a ‘Safe Harbor’ Plan,” said Jim Cichanski, founder and chief human resources officer for Flex HR. “This is a 401K plan that contributes a certain match and will not need to do testing to ensure the highly compensated level of employees are meeting a percentage of savings of lower compensated employees. This also can save tremendous administrative time when doing the yearly audit of plans.”

Create a retirement plan advisory committee

An employee retirement plan affects the whole company, so it’s important to bring in the right voices to ensure you’re making an informed decision. D’Acierno suggested forming a retirement plan advisory committee that includes other stakeholders in the company, including employees who will invest in the plan.

“This committee normally has about three to seven members who have a level of expertise in finance, HR/payroll, or sit at executive levels,” he said. “It is important to note that the individuals responsible for making decisions for the plan are liable to the plan at a fiduciary level, so it is important for them to understand their responsibilities and for your company to provide levels of risk mitigation for those members.”

Cichanski recommended that the finance and HR departments be represented on this committee, as well as the CEO.

Thoroughly vet a provider before choosing them

Once you believe you’ve identified the right plan and right provider, put them to the test. Schedule multiple calls to ask detailed questions of company representatives, test their customer service and gather reviews from existing customers. Once you choose a provider, it’s not an easy process to switch, so do your due diligence on the front end to avoid an expensive and time-consuming hassle later.

“As you select a provider, talk to them many times and look at the customer service of that vendor. Check references out and key into the support provided by the vendor,” Cichanski said.