Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Your employees will appreciate a robust retirement plan — and your business will benefit, too.

If you’re considering offering employee benefits, few perks are more desirable to workers than a 401(k) retirement plan. As such, many employers use robust retirement plan options to attract and retain quality employees. We’ll explain why a 401(k) plan is a popular choice for business owners and employees and share how to set one up with a top provider.

Searching for employee retirement plans and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

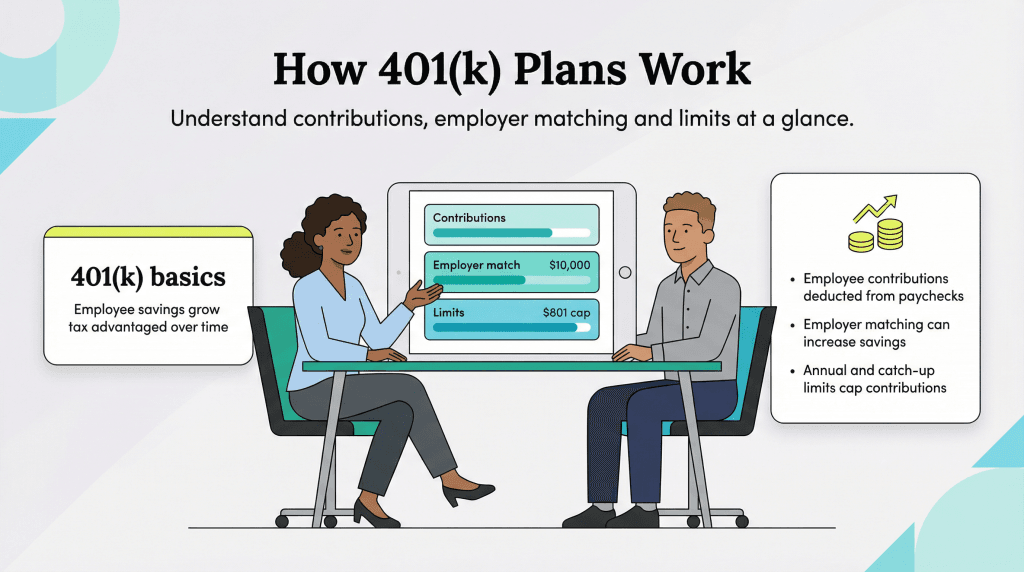

A 401(k) plan is an employer-sponsored benefit designed to help employees save for retirement. According to the IRS, a 401(k) is a feature of a qualified profit-sharing plan that allows employees to contribute a portion of their wages to individual accounts. Employees typically have several investment options for how their money is allocated.

Many of the best employee retirement investment plans can help businesses of all sizes establish or change a 401(k) plan.

These retirement plans are straightforward. Here’s how they work:

Eliza Guilbault, vice president of planning and engagement at Fidelity, noted that most workers today are responsible for funding their retirement. “We are shifting from an employer-funded pension plan to a defined contribution plan landscape,” Guilbault explained. “A 401(k) is a great way to save for the future.”

Employers sponsor these plans, but employees own the money they contribute, along with any vested employer contributions (more on vesting below).

To boost participation, employers sometimes participate in 401(k) matching. They contribute to their employees’ 401(k) accounts based on each employee’s contribution. They may entirely or partially match an employee’s contribution up to a specific percentage. For example, if an employee contributes 4 percent of their paycheck, their employer might match that amount — effectively increasing the employee’s total contribution.

Employers may implement a vesting period. This designation dictates how long an employee must stay with the organization before the matching contributions fully belong to them. Implementing a vesting schedule helps incentivize employees to stay with the company.

Sarah Chen, founder and principal at Recruit Engineering, noted that 401(k) matching can be an effective employee recruitment incentive. “Offering anything over 20 percent in matching contributions is a strong perk, and anything approaching 50 percent will likely put your company at the top of the list for the best candidates,” Chen explained.

As of 2026, an employee can contribute up to $24,500 annually. Including employer contributions, the total annual contribution limit is $72,000 per employee in 2026. Those ages 50 to 59 can contribute an additional $8,000. Employees ages 60 through 63 benefit from an enhanced catch-up contribution limit of $11,250.

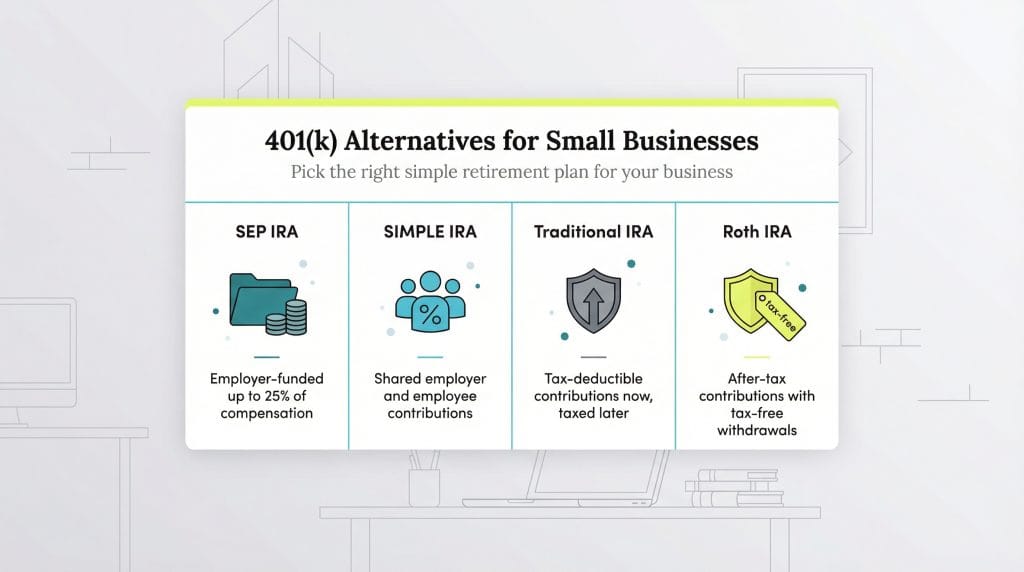

There are a few types of 401(k) plans, including the following popular ones:

Learn which 401(k) plan might work best for your business.

While offering a 401(k) plan gives employees a powerful tool to save pretax dollars for retirement, it also delivers significant advantages for the business itself, including the following:

While a 401(k) plan is a benefit traditionally offered by larger organizations, Guilbault said small businesses should strongly consider offering one, too. “Many [retirement plan] providers have solutions that are great for small businesses,” Guilbault noted. “Fidelity works with thousands of small businesses.”

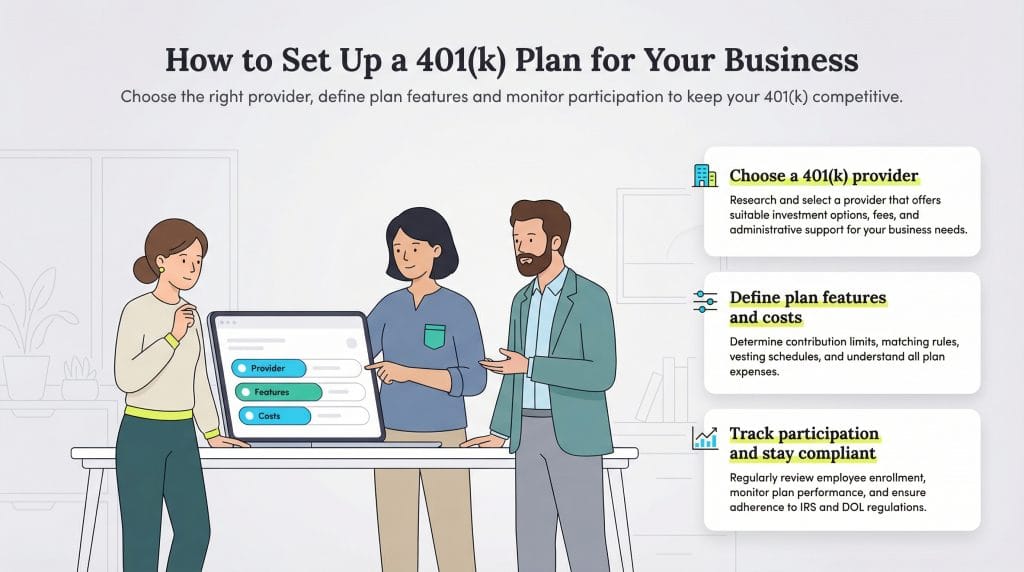

To set up a 401(k) plan for your business, take the following steps:

Numerous dedicated retirement plan providers exist. Additionally, the best online payroll services and the best professional employer organizations often provide 401(k) plan management in addition to their core services.

For example, Gusto is a multifaceted platform that offers payroll, employee benefits and human resources management software. Its payroll services can easily and accurately accommodate 401(k) contributions and matches. Read our review of Gusto HR software and our Gusto payroll review to learn more.

States have various rules and regulations about retirement plans, and the landscape has been shifting in recent years. A growing number of states now require employers to offer retirement savings options. California’s CalSavers program, for instance, applies to businesses with one or more employees who do not offer a qualifying retirement plan. Other states — including Illinois, Oregon, Colorado and New York — have enacted similar auto-IRA or state-facilitated savings programs with their own eligibility thresholds and deadlines.

Because requirements differ significantly by state, small business owners should review their state’s specific rules — ideally with a benefits advisor or legal counsel — to confirm they’re in compliance and avoid potential penalties.

401(k) plans have various features and functions, so business owners must make some decisions. Consider whether you want any of the following:

For small businesses, the costs of offering a 401(k) retirement plan can vary greatly and may include the following:

Providing a 401(k) plan incurs costs, but some expenses may be offset by tax incentives. Due to the SECURE 2.0 Act, small businesses with 50 or fewer employees can claim a tax credit of up to 100 percent of plan startup costs — capped at $5,000 per year — for the first three years of the plan. Businesses with 51 to 100 employees may still qualify for a partial credit. You may also be able to deduct ongoing administrative fees from your business taxes.

Nikita Sherbina, co-founder and CEO of AIScreen, emphasized the importance of communicating with your team so they understand the plan’s structure and benefits. “Education is key. Give employees the tools to understand the long-term benefits of the plan and encourage regular contributions,” Sherbina advised.

To ensure your plan remains attractive and effective, regularly assess employee participation rates and contribution levels. “Review the plan regularly and adjust the match to stay competitive,” Sherbina added.

A 401(k) is not the only option for small businesses looking to establish a retirement plan for their employees. Business owners should also consider the following potential alternatives.

Source interviews were conducted for a previous version of this article.