Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Are the Benefits of Using Direct Deposit? A Complete Guide

Learn the pros and cons of using direct deposit payroll services and how to set them up for your business.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Direct deposit has become the standard way businesses pay employees. Instead of printing, signing and distributing paper checks, employers can send wages directly to workers’ bank accounts on payday.

For many small businesses, direct deposit helps streamline the payroll process, reduce paperwork and ensure employees receive their pay on time. However, setting up and managing direct deposit comes with responsibilities, and occasional errors can create headaches for employers and employees alike. This guide explains how direct deposit works, its advantages and disadvantages and what you need to know before offering it to your employees.

What is direct deposit?

Direct deposit is an electronic payment method that transfers funds directly from an employer’s bank account to an employee’s bank or credit union account through the Automated Clearing House (ACH) network.

When you run payroll, employees who have chosen direct deposit receive their wages automatically in their designated accounts on payday. To set up direct deposit, employees typically provide information such as their bank’s routing number, account number and account type.

Direct deposit is most commonly used to pay employees, but businesses and government agencies use it for many other types of payments as well.

“It is also used for tax refunds, retirement benefits, expense reimbursements, investment distributions and insurance claim payments,” explained Heather McElrath, the former director of communications for Nacha, the nonprofit membership organization that governs and manages the ACH Network.

Searching for payroll software or services and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

FYI

Direct deposit isn't the only type of ACH payment. The same network businesses use to pay employees can also be used to collect recurring customer payments, pay vendors and issue expense reimbursements.

How to set up direct deposit

Setting up direct deposit requires a little upfront work, but most payroll providers make the process relatively straightforward. Once everything is in place, employees can receive their pay automatically on payday, and you’ll have one less administrative task to worry about.

While the exact process varies by provider, most small businesses can set up direct deposit by following these four basic steps.

Step 1: Choose a payroll provider.

The first step is selecting a payroll provider that supports direct deposit. Most of the best online payroll services include direct deposit as part of their payroll offerings, although fees, processing times and setup requirements can vary.

When choosing a payroll provider, look beyond pricing. Consider factors such as payroll tax filing services, employee self-service tools, payroll reporting features, customer support and how quickly the provider can process payroll. Some services offer next-day or even same-day direct deposit, while others require payroll to be submitted several days before payday.

If you’re already happy with your business bank, it’s worth asking whether it offers direct deposit services. However, many small businesses find that payroll software provides a simpler way to manage direct deposit, tax filings and other payroll tasks from a single platform.

Before implementing direct deposit, take some time to understand the federal and state rules that apply to electronic wage payments. At the federal level, the key regulations come from the Electronic Fund Transfer Act (EFTA) and Regulation E.

Here’s what employers should know:

Employees must have a choice: Under federal law, employers generally may require direct deposit, but they cannot require employees to use a specific bank or credit union. Employees must be free to choose their own financial institution.

Minimum wage protections apply: In addition, any fees associated with receiving wages electronically cannot reduce an employee’s pay below the applicable minimum wage.

State rules vary widely: State laws may impose additional requirements. For example, as of 2026, states such as Texas, Virginia and Washington generally allow employers to require direct deposit under certain conditions, while states including California, New York and Illinois require employee consent before wages can be deposited electronically.

Documentation requirements may apply: In addition to consent requirements, many states require employers to obtain and retain written direct deposit authorization forms before electronic wage payments can begin.

Most payroll providers can help employers navigate state-specific rules and provide the payroll forms needed to obtain employee consent and set up direct deposit.

Tip

If you're unsure about your state's direct deposit requirements, your payroll provider is a good place to start. Many providers can supply the authorization forms and employee notices needed to stay on top of HR compliance.

Step 3: Collect employee information.

Once you’ve chosen a payroll provider and reviewed the applicable requirements, you’ll need to collect the employee information required to set up direct deposit for your workers. Most payroll providers supply their own authorization forms, although the information requested is generally similar from one provider to the next.

Employees will typically need to provide the following:

Full legal name

Bank account number

Bank routing number

Account type (checking or savings)

Bank name

Deposit instructions, if they want to split their paycheck between multiple accounts

Depending on your payroll provider, employees may also need to provide a voided check or other documentation to verify their account information.

Gathering this information may take some time initially, especially if you’re enrolling existing employees. However, once direct deposit is set up, managing payroll becomes much easier. For new hires, you can collect direct deposit information during the employee onboarding process so everything is ready before their first payday.

Step 4: Set a deposit schedule.

Once you’ve entered your employees’ information, it’s time to decide when payroll will run and when employees will receive their wages. Your payroll schedule should align with your cash flow and give you enough time to process payroll before each payday.

Direct deposit processing has become much faster in recent years. Many payroll providers now even offer same-day or next-day ACH processing, but standard ACH transfers can still take one to two business days. Federal holidays and bank schedules can occasionally add extra time to the process.

That’s why payroll generally needs to be submitted before payday. Your payroll provider will let you know when payroll must be processed and when funds need to be available in your business bank account so employees receive their wages on time.

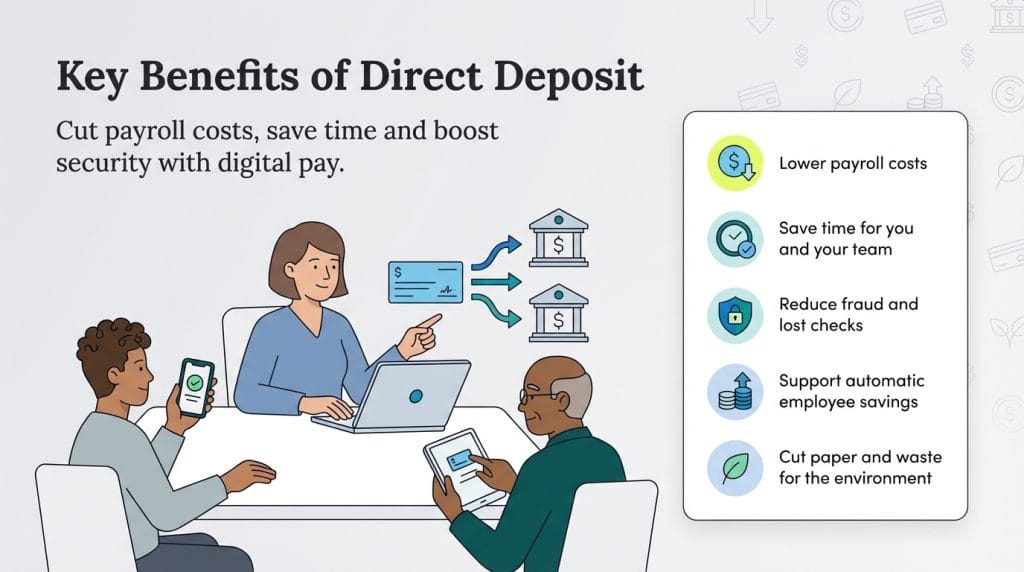

Benefits of direct deposit

Payday tends to run more smoothly with direct deposit. Employees receive their wages automatically, and employers no longer have to print, sign and distribute paper checks every pay period.

“Whether you are a 10-person operation or smaller, or a business of more than 100 employees, you can gain from direct deposit’s advantages,” McElrath said.

Here are some of the biggest benefits direct deposit can offer employers and employees.

Lower costs: Direct deposit can reduce payroll costs by eliminating the need to print, distribute and store paper checks. Because there’s no need for postage, paper or mailing supplies, even small savings per paycheck can add up over time, especially as your business grows.

Time savings: Direct deposit doesn’t just save money. It can also reduce the time spent managing payroll. Once employees are enrolled, employers no longer need to print, sign and distribute paper checks each pay period. Employees benefit too, since they don’t have to make a trip to the bank to cash or deposit their paychecks.

Enhanced security: Paper checks can be lost, stolen or altered, creating risks for both employers and employees. In fact, according to the 2026 AFP Payments Fraud and Control Survey, checks remained the payment method most frequently affected by fraud. In 2025 alone, 58 percent of organizations reported check fraud, outpacing ACH fraud and wire fraud. Because direct deposit transfers funds electronically, it eliminates many of the risks associated with paper checks.

Automatic savings options: Direct deposit lets employees automatically direct part of their paychecks into savings accounts, investment accounts or other designated accounts. “With split deposit, employees can direct a fixed amount or percentage of their pay into a savings or investment account to help build savings,” McElrath said. “As the single biggest influence on employees’ use of direct deposit, businesses can play a key role in supporting employee financial health.”

Less paper waste: Direct deposit eliminates the paper, printing and mailing associated with traditional paychecks. While the environmental impact may be modest for a single business, it can add up over time, particularly for growing companies with larger workforces.

Easier hiring and onboarding: For many workers, direct deposit isn’t a new perk or convenience — it’s simply how they get paid. According to Payroll.org’s 2025 Getting Paid in America survey, 92.65 percent of workers receive their wages through direct deposit, while only 3.30 percent are paid by paper check. Because direct deposit has become the standard payment method, offering it can help streamline onboarding and payroll administration while giving employees a familiar way to receive their wages.

Potential drawbacks of direct deposit

Direct deposit offers plenty of advantages, but it’s not without challenges. Here are a few potential drawbacks to keep in mind.

Strict deadlines: Direct deposit is time-sensitive. To ensure employees are paid on time, payroll must be submitted by your provider’s processing deadline. Missing that deadline can delay payments and create frustration for employees. While some payroll providers offer same-day or off-cycle payroll options, those services may come with additional fees.

Security risks: Direct deposit is generally more secure than paper checks, but it still requires employers to collect and store sensitive employee banking information. Businesses should have safeguards in place to protect bank account and routing numbers, along with payroll system credentials and other payroll-related data.

Banking information must stay current: A bank change can create payroll headaches if employee records aren’t updated. Employees who switch accounts should provide their new direct deposit information as soon as possible.

Correcting mistakes can be more complicated: With a paper check, employers may be able to stop payment before the check is cashed if a payroll discrepancy is caught. Direct deposits can sometimes be reversed or corrected, but the process is often more time-sensitive. Regular payroll audits can help catch errors before employees are paid.

Overdraft risks: Maintaining a healthy cash buffer is essential when using direct deposit. If there aren’t enough funds in your business bank account when payroll is processed, you could face overdraft fees, failed payroll transactions or other disruptions. Reviewing your account balance before each payroll run can help prevent costly surprises.

Direct deposit tax implications and compliance considerations

Direct deposit may simplify payday, but the compliance side of payroll doesn’t go away. From payroll tax deposits to record-keeping requirements, there are a few compliance considerations to keep in mind.

Federal tax requirements

The IRS requires employers to make federal employment tax deposits electronically, regardless of whether employees are paid via direct deposit or paper check. Businesses can submit payroll tax deposits through the Electronic Federal Tax Payment System (EFTPS), their IRS Business Tax Account or IRS Direct Pay for businesses.

The deposit schedule you must follow is generally based on your payroll tax liability. Depending on your circumstances, you may be classified as a monthly or semiweekly depositor.

State compliance requirements

States may impose additional requirements related to direct deposit, wage payments and payroll records. For example, some states require employers to provide employees with pay stubs for each pay period, while others have specific rules regarding employee consent and wage-payment methods.

Record-keeping obligations

Employers should maintain accurate records related to payroll and direct deposit, including:

Employee direct deposit authorization forms

ACH transaction confirmations

Pay stubs and payroll records

Payroll tax deposits and payment confirmations

Employee banking information

Don’t be in a hurry to purge old payroll records. Federal rules generally require employers to keep certain records for at least three years, and some states require them to be retained even longer.

Did You Know?

If managing payroll compliance becomes overwhelming, a professional employer organization (PEO) may be able to help. Many of the best PEO services handle payroll administration, tax filings and other HR responsibilities on behalf of their client businesses.

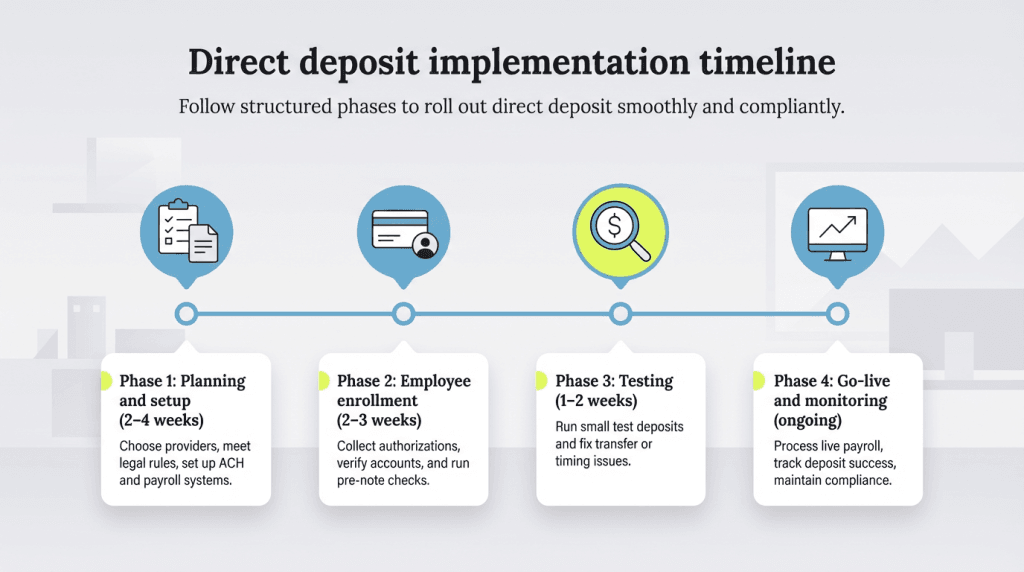

Direct deposit rollout timeline

The amount of time it takes to implement direct deposit depends on your payroll provider, your bank and the size of your workforce. Some small businesses can get up and running in just a few days, while others may need several weeks to complete enrollment and testing.

In general, the process looks something like this:

Phase 1: Planning and setup (a few days to 2 weeks)

Choose a payroll provider or bank service.

Review any applicable state requirements.

Set up your payroll software and banking connections.

Phase 2: Employee enrollment (1-2 weeks)

Distribute direct deposit authorization forms.

Collect employee banking information.

Verify account details as needed.

Phase 3: Testing (a few days to 1 week)

Run any required account-verification or test transactions.

Confirm deposits are processing correctly.

Resolve any setup issues.

Phase 4: Launch and monitoring (ongoing)

Process your first payroll run.

Confirm employees receive their deposits on time.

Answer employee questions and monitor for issues.

Direct deposit FAQs

Nacha, formerly known as the National Automated Clearing House Association, is the nonprofit organization that oversees the ACH Network. The ACH Network moves money electronically between U.S. bank accounts and powers transactions such as direct deposit, Social Security payments, government benefits, bill payments and person-to-person transfers.

In 2025, the ACH Network processed 35.2 billion payments worth $93 trillion, according to Nacha, representing a 4.9 percent increase in payment volume from the previous year.

Nacha develops and maintains the rules that help financial institutions process ACH payments safely and consistently. Although it isn't a government agency, it works closely with banks, payment providers and federal agencies to support the electronic payment system used throughout the United States.

The cost of setting up direct deposit depends on your payroll provider, bank and number of employees. Some payroll providers include direct deposit in their standard payroll service, while others charge additional fees. For example, Gusto's Simple plan costs $49 per month plus $6 per employee and includes unlimited payroll, direct deposit and direct deposit alternatives such as paper checks and payroll cards. Learn more in our Gusto Payroll review.

Most employees who receive direct deposit have access to their wages on payday, often by the start of the business day. Under Nacha rules, direct deposit funds generally must be available by 9 a.m. local time at the receiving bank on the settlement date. (Beginning in September 2026, this requirement will apply uniformly to all non-same-day ACH credits.)

Some banks memo-post incoming transactions before they fully settle, so employees may see a pending deposit in their account before the funds become available.

For employers who need more flexibility, same-day ACH is widely available through major payroll providers. Depending on when a payment is submitted, funds may become available later that day, making same-day ACH a useful option for off-cycle payroll runs, payroll corrections or paying workers who aren't on a fixed pay schedule.

Yes. Independent contractors can be paid through direct deposit just like employees.

The main difference involves tax paperwork. Contractors generally complete Form W-9 instead of Form W-4, and businesses that pay a contractor $600 or more for services during the year are generally required to issue Form 1099-NEC.

Most payroll providers support direct deposit for contractors, although some charge separately for contractor payments or offer them as part of a different plan. If your business relies heavily on freelancers or independent contractors, it's worth reviewing how your payroll provider handles those payments before you sign up.

Direct deposits are generally reliable, but payments can occasionally fail or be rejected. Common reasons include:

An incorrect routing number or bank account number

A closed, frozen or inactive bank account

A mismatch between the employee's name and bank account information

Insufficient funds in the employer's account

A payroll processing or ACH transmission error

Rejected direct deposits are uncommon, but they do happen. An incorrect account number, a closed account or another banking issue can cause a payment to bounce back. When that happens, payroll providers can usually help employers track down the problem and resend the payment.

No. Setting up direct deposit does not give employers access to an employee's bank account, account balance or transaction history. Employers typically collect limited information — such as a bank account number, routing number and, in some cases, a voided check — solely to deposit wages electronically.

Direct deposit authorization allows employers to send payments to an employee's account, but it does not allow them to view account activity or withdraw funds.

Julie Thompson contributed to this article. Source interviews were conducted for a previous version of this article.

Simone Johnson dedicates her time to educating small business owners on the best practices for both daily operations and long-term sustainability. With a longstanding passion for finance, she often guides entrepreneurs on financial matters.

At business.com, Johnson covers finance topics like business loans and grants, cash flow strategies, credit card processing and payroll forms.

Johnson has also profiled entrepreneurs and assisted companies with customer targeting and brand refinement. Recently, she has focused on workforce management, providing advice on helping employees set company-aligned goals, the pros and cons of employee monitoring, and more. Armed with a bachelor's degree in communications and a master's in journalism, Johnson brings a unique blend of expertise and insight to her advisory work.