Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

The Pros and Cons of a Payroll Card

Payroll cards can offer a convenient way to pay employees who don't use traditional banking services.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Payroll cards are gaining traction among small businesses as a practical way to pay employees who don’t use traditional banking methods. These reloadable debit cards give workers a simple, secure way to access their wages — without paper checks, trips to the bank or costly check-cashing fees.

We’ll explain how payroll cards work, break down their pros and cons and compare them with other payment options, including direct deposit and paper checks.

Searching for payroll software or services and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

What is a payroll card?

Payroll cards are prepaid debit cards employers use to pay workers their wages. They’re loaded with an employee’s compensation each pay period and can be used to withdraw cash, pay bills or make purchases anywhere debit cards are accepted.

“[Payroll cards] allow employees to access their earnings immediately without waiting for a check to clear or relying on a traditional bank account,” explained Brian Chasin, chief financial officer of SOBA New Jersey. “These cards function like a debit card, enabling employees to make purchases in stores or online, withdraw cash from ATMs and pay bills electronically.”

Payroll cards can make a real difference for unbanked or underbanked workers, especially those who’d otherwise pay check-cashing fees or wait a few extra days to get their money. “By offering payroll cards, employers can streamline payroll processing, reduce administrative costs and provide a more secure alternative to paper checks,” Chasin noted.

According to the most recent data from the Federal Deposit Insurance Corporation (FDIC), approximately 4.2 percent of U.S. households are unbanked. That may sound small, but it still represents millions of Americans without access to a traditional bank account. For these workers, payroll cards can offer a practical way to get paid quickly and avoid extra fees.

Tip

Payroll cards can offer some protection against unauthorized card transactions, but not all cards are created equal. Choose a payroll provider that offers a zero-liability policy, real-time transaction alerts, chip technology and account monitoring.

Payroll card pros and cons

Before deciding whether to offer payroll cards to your employees, it’s worth weighing their benefits and drawbacks carefully.

Payroll card pros

No bank account needed: Payroll cards can be especially helpful for employees who don’t have traditional bank accounts or prefer not to use direct deposit.

Lost cards can be replaced: Lost or stolen payroll cards are usually easy to replace, although some providers may charge a replacement fee.

Easy access to wages: Workers can access their funds immediately and use their payroll cards to make purchases, pay bills or withdraw cash.

Cost-effective: Depending on the provider, payroll cards can be a cost-effective alternative to printing and mailing paper checks — which can cost businesses $4 or more per check once paper, printing, postage and administrative time are factored in — or paying direct deposit setup fees.

Payroll card cons

No interest: Payroll cards do not earn interest.

Can be lost or stolen: Like any physical card, payroll cards can be misplaced or stolen.

Can incur fees: Employees may face fees for ATM withdrawals, balance inquiries, fund transfers, inactivity, monthly maintenance or account closure.

Peter Lai, chief financial officer of Engage Wellness, noted that fees, in particular, can be a drawback, as they can gradually reduce an employee’s take-home pay. “Employees who rely on ATMs frequently or require cash access for daily expenses may find that these charges add up over time, offsetting the convenience of direct wage deposits,” Lai explained.

Payroll card providers

Specialized payroll card companies and many of the best online payroll services can help you set up and distribute payroll cards for your employees. Some of your choices include the following:

Money Network

Money Network offers payroll cards and an intuitive online platform for managing them. The company also provides enhanced security features, FDIC-insured funds and zero-liability protection against unauthorized purchases, helping employees access and manage their wages with confidence. Money Network has more than 20 years of experience in prepaid debit processing and serves millions of cardholders across the U.S.

Netspend Skylight One Card

Netspend runs one of the country’s largest prepaid payment programs and offers flexible enrollment, robust electronic reporting and online account management tools. Employees can log in to view deposits, track transactions and access statements through the online portal or mobile app.

Cardholders can also access 100 percent of their wages in cash by using a no-cost Skylight Check at more than 8,800 locations nationwide. Netspend’s broader reload network includes more than 130,000 cash reload locations across the U.S., giving cardholders plenty of ways to add funds when needed.

As a full-service partner, Netspend also provides implementation support, training, employee education materials and compliance resources for employers.

rapid! PayCard

rapid! offers Visa and Mastercard payroll cards as part of its broader electronic payroll platform. Employees can access their wages on payday, view electronic pay stubs, track transactions through the mobile app and manage their accounts online.

The company charges zero employer fees for card inventory, training or implementation and also provides compliance tools, including its Compliance Map, to help employers stay on top of wage payment requirements. Funds are held by FDIC-insured issuing banks, and employees can continue using their rapid! PayCard even if they change jobs or receive other eligible direct deposits.

U.S. Bank Focus Payroll Card

U.S. Bank offers payroll cards for businesses of all sizes through its Focus Payroll Card program. The bank’s prepaid payroll solution includes fraud protection, online purchasing, automated card inventory management and robust client reporting tools for employers.

Employees also get access to a mobile banking app, text and email alerts, cash-back rewards and convenient access to their wages through U.S. Bank’s prepaid platform.

Wisely by ADP

ADP’s Wisely payroll card gives employees a flexible way to access and manage their wages. Through the Wisely mobile app, cardholders can track balances, monitor spending, pay bills and manage their accounts on the go.

Wisely also offers access to tens of thousands of surcharge-free ATMs nationwide, cash-back rewards at participating retailers and fraud protection features such as instant card lock if a card is lost or stolen. Employees may also qualify to receive direct deposits up to two days early, depending on their employer and banking setup.

For employers, ADP positions Wisely as a payroll payment solution built to support wage-payment compliance across all 50 states while helping businesses move away from paper checks and offer employees more flexible access to their wages.

FYI

If your business already uses ADP for payroll, adding Wisely may be one of the easiest ways to roll out payroll cards without introducing another payroll vendor. Our ADP Payroll review breaks down the platform's pricing, features, support options and integration capabilities.

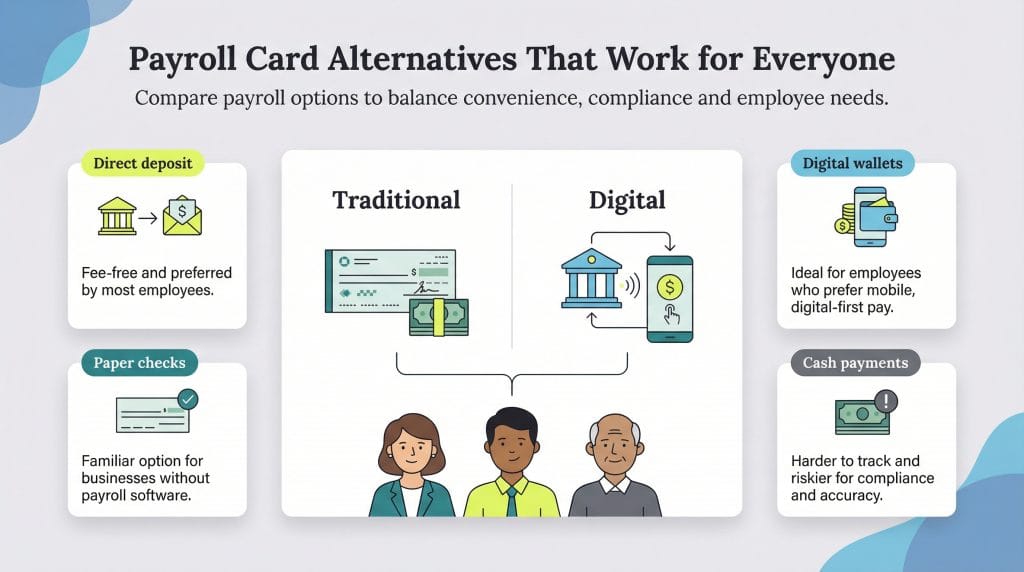

Payroll card alternatives

Under federal law and many state wage-payment laws, employers generally cannot require employees to receive wages through a payroll card as their only payment option. Businesses that offer payroll cards must also provide at least one alternative payment method — typically direct deposit or paper checks — and may need to obtain an employee’s voluntary written consent before enrolling them in a pay card program.

“Direct deposit is a popular, fee-free alternative and digital wallets are growing in use as well, providing flexibility without the extra costs,” explained Taryn Pumphrey, president of Ledger Lift. “If your workforce lacks traditional banking access, payroll cards can be a great option, but direct deposit or mobile payments might be more cost-effective for others.”

Here are some options to consider.

Direct deposit

Direct deposit is one of the most common ways businesses pay employees. It uses the Automated Clearing House (ACH) network, which securely moves funds between bank accounts and supports both ACH payments and direct deposits.

To get started, employees provide their checking or savings account information during the onboarding process, allowing your payroll provider or payroll team to deposit wages directly into their bank account each pay period.

While employees need a bank account to use direct deposit, the method offers several advantages: It eliminates paper checks, reduces the risk of lost payments and gives workers fast, convenient access to their wages without an extra trip to the bank.

Did You Know?

According to PayrollOrg's 2025 Getting Paid in America survey, nearly 93 percent of respondents said they receive their wages via direct deposit, making it by far the most common way Americans get paid.

PayPal

PayPal is a popular payment option for businesses that hire freelancers, independent contractors or other nonemployee workers. Whether you work with one-time, seasonal or part-time help, PayPal can eliminate the need for paper checks or payroll cards.

Contractors can create and send invoices through PayPal, which makes it easier to keep track of who was paid, how much and when — something that comes in handy at year-end. When you send a payment, make sure it’s marked as a business transaction for goods or services so everything is documented correctly and the contractor gets access to PayPal’s business payment features.

Mobile wallets

Mobile wallets aren’t just an emerging payment trend anymore. With an estimated 4.5 billion users worldwide in 2025, they’re already part of how a lot of people pay bills, move money and manage day-to-day spending from their phones. For small businesses, that’s an opportunity to meet employees where they’re already handling their finances.

As more banks let customers add debit cards and direct deposit accounts to digital wallets, employees can connect their pay to apps like Google Pay, Apple Pay, Samsung Pay and others. For workers who already use their phones to pay bills, send money or keep an eye on balances, that can make payday feel a little more immediate, especially when faster payment options are in the mix.

Paper checks

Despite the popularity of digital payment options, paper checks are still very much in use for business payroll. Some employers prefer to run payroll manually or stick with familiar payment processes instead of moving to a fully digital payroll system.

Cash

Paying employees in cash is legal as long as you properly withhold taxes and keep accurate payroll records. That said, it’s not how most businesses want to handle payroll for long. You might save on processing fees, but someone still has to track every payment by hand, document it correctly and make sure nothing slips through the cracks, and this is the kind of extra work that can lead to payroll discrepancies, IRS headaches or employee disputes if something gets missed.

Cash payroll also means more trips to the bank to manage cash flow and ensure the correct amount is available on payday. Once you’ve calculated payroll, each payment must be counted, documented and delivered to employees by hand.

FYI

Some businesses are exploring digital payment methods like Zelle, Venmo and Cash App to pay freelancers, independent contractors and gig workers. These options can be fast and convenient, but they may lack the payroll reporting tools, protections and payroll tracking features that traditional payroll systems offer.

Payroll card FAQs

Not exactly. Payroll cards are prepaid debit cards, but they work differently from traditional bank-issued debit cards. A payroll card is issued by an employer and isn't tied to a personal bank account. Because payroll cards are preloaded with wages, cardholders typically can spend only the funds available on the card.

Traditional debit cards, by contrast, are issued by banks and linked directly to a checking account. Depending on the account and bank settings, debit card purchases may allow overdrafts or trigger overdraft fees.

No. Under federal law, employers generally must offer workers at least one alternative way to receive their wages in addition to payroll cards. In many cases, that alternative is direct deposit or paper checks, although state wage-payment laws may impose additional requirements.

Payroll cards can cost businesses anywhere from $2 to $10 per employee each month, depending on the provider and features included, while paper checks can cost $4 or more per check when you factor in printing, postage and processing.

Employers can offer more than two payment options, and states may have their own rules around employee consent and acceptable wage-payment methods, so it's important to check your state's labor laws.

With nearly two decades of experience under her belt, Julie Thompson is a seasoned B2B professional dedicated to enhancing business performance through strategic sales, marketing and operational initiatives. Her extensive portfolio boasts achievements in crafting brand standards, devising innovative marketing strategies, driving successful email campaigns and orchestrating impactful media outreach.

At business.com, Thompson covers branding, marketing, e-commerce and more.

Thompson's expertise extends to Salesforce administration, database management and lead generation, reflecting her versatile skill set and hands-on approach to business enhancement. Through easily digestible guides, she demystifies complex topics such as SaaS technology, finance trends, HR practices and effective marketing and branding strategies. Moreover, Thompson's commitment to fostering global entrepreneurship is evident through her contributions to Kiva, an organization dedicated to supporting small businesses in underserved communities worldwide.