Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Direct deposit may not be suitable for every worker. Learn about alternative payment methods for your team.

To boost employee retention and satisfaction, you must provide your workers with accurate and timely payments. Automating your payroll via a reputable service can ensure prompt, accurate payments and help you comply with local, state and federal tax laws.

The best online payroll services support direct deposit, a payment method many workers prefer. However, direct deposit doesn’t work for everyone and may not suit your team members. Fortunately, viable direct deposit alternatives may work well for your business and provide stability to a growing workforce.

Searching for payroll software or services and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

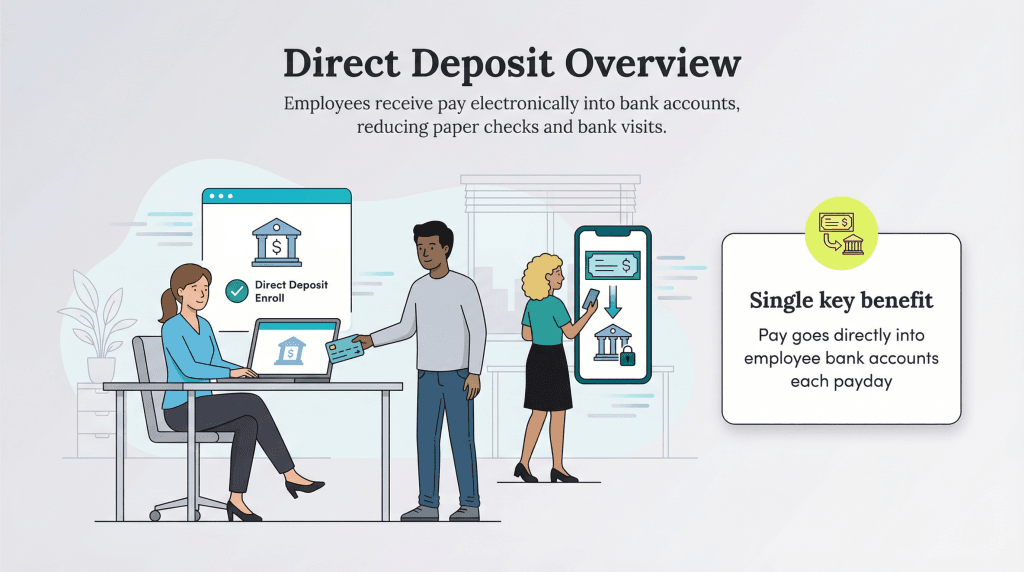

Direct deposit is a payment method that delivers paychecks to employees electronically. Employees provide their checking or savings account information to human resources during the onboarding process. The employer transfers workers’ paychecks into their bank accounts every payday, thus eliminating paper checks and trips to the bank.

Most employers offer direct deposit and it’s a popular, convenient and practical option. However, direct deposit is not suitable for all workers, particularly those without a bank account.

According to the most recent Federal Deposit Insurance Corporation survey of unbanked and underbanked households, more than 5.6 million United States adults, or around 4.2 percent of U.S. households, are unbanked. An income of less than $30,000 is the strongest indicator of a higher-than-average unbanked community.

“Employers need alternatives to direct deposit to ensure all employees, including the unbanked and those who prefer different payment methods, receive their wages efficiently,” said Kevin Shahnazari, the founder and CEO of FinlyWealth. “Relying solely on direct deposit can alienate workers without traditional bank accounts, creating unnecessary barriers to financial access. Multiple payment options ensure inclusivity, enhance employee satisfaction and prevent payroll disruptions.”

When employees lack banking options, they may turn to alternative finance methods with unreasonably high interest rates and fees, often leading them to live from paycheck to paycheck. Employers have payroll options to help unbanked employees or those who prefer other payment forms.

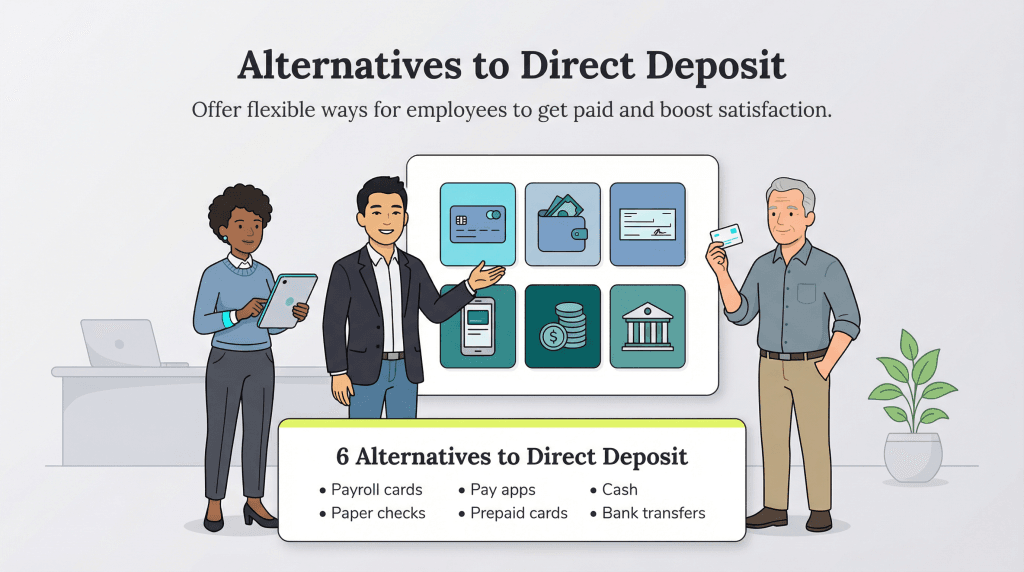

If direct deposit isn’t the best fit for your business or employees, there are several other payment methods to consider. “In my experience, organizations offering multiple payment methods have higher employee satisfaction and retention,” said Luca Dal Zotto, founder of Convert Bank Statement. “For example, one of my clients switched to a hybrid model (payroll cards + direct deposit) and saw a 20 percent increase in employee satisfaction after six months.”

Here’s a look at six popular direct-deposit alternatives that may benefit your staff and business.

The automated clearing house (ACH) network began in the 1970s. As the growing number of paper checks became overwhelming, U.S. banks wanted to improve how money was transferred. Nacha (formerly the National Automated Clearing House Association) manages and governs the ACH network.

ACH provides a bank-level encrypted electronic transfer of money between banks. ACH manages the system behind direct deposit and direct payments. Your business, the government or an individual can make payments using this network.

“ACH transfers are a strong alternative to direct deposit, offering a secure and cost-effective way to move funds between bank accounts,” said Shahnazari. “They provide flexibility for employers handling payroll and enable employees to receive payments without traditional direct deposit arrangements.”

ACH is different from a wire transfer or credit card network. It is a direct payment between two bank accounts. ACH transfers are grouped by the two banks that completed the transaction. The bank checks and holds the transactions before they are sent in bulk.

“ACH transfers are a safe method, allowing businesses to transfer payments directly into accounts without the use of paper checks,” said Dal Zotto. “ACH payments are also cheap, ranging from 25 cents to 50 cents per transaction and are, therefore, a favorite among businesses.”

While ACH transfers are often associated with direct deposits, ACH direct payments are another option. ACH direct payments can be made via ACH credit payments and ACH debit payments:

ACH pros

ACH cons

Setting up ACH payments

To set up ACH payments, follow these steps:

Some employees may prefer to receive their paychecks via a payroll card. Payroll cards work like debit cards. Every payday, the card is loaded with the employee’s earned wages. The employee can use the money to take out cash from an ATM, make purchases, pay bills online and transfer money to friends and family.

“Prepaid debit cards or payroll cards are ideal options for unbanked employees,” said Dal Zotto. “These cards allow workers to be remunerated in real time without a bank account. As estimated by the National Payroll Reporting Consortium study, 6.5 million Americans used payroll cards.”

Payroll card pros

Payroll card cons

Setting up payroll cards

Here’s how to set up payroll cards:

Paying contractors or irregular part-time employees can be a hassle if you use paper checks or pay cards. PayPal is a great option for paying freelancers or one-time invoices.

When sending these payments, be sure to check the box for “service.” Sending a service payment may incur a fee for the contractor, but this fee gives the recipient an instant payment option. You must determine a different payment option if the freelancer doesn’t agree to this fee. It’s a good idea to clarify from the outset that you’re paying via PayPal.

“Electronic payment mechanisms like PayPal and mobile wallets [like Apple Pay or Google Pay] are rising,” said Dal Zotto. “PayPal alone, for example, has 435 million active accounts worldwide, making it possible for employees to get instant, easy pay. Mobile wallets are particularly appealing to young, technology-savvy employees.”

PayPal pros

PayPal cons

Paying contractors with PayPal

Either way, you can pay the contractor via a bank account or credit card; additional fees may apply.

According to Statista, 96 percent of Americans own a smartphone. Because employees can access social media accounts, email, banks and more on their smartphones, receiving their paychecks through a mobile wallet like Venmo for Business or Apple Pay is likely quick and convenient.

“Mobile wallets, including Apple Pay, Google Pay and Venmo, have gained popularity as payroll alternatives, particularly among younger workers,” said Shahnazari. “Employers can issue payments directly to employees’ mobile wallets, allowing instant access and seamless digital spending without requiring a traditional bank account.”

Mobile wallet pros

Mobile wallet cons

Paying employees with a mobile wallet

To offer a mobile wallet as a payment method, it’s best to partner with payroll software that supports this feature. Payroll software platforms such as QuickBooks Payroll, Paychex and Gusto offer mobile app solutions to complete payroll on the go.

Paying by paper check may seem old-fashioned, but it still brings benefits. For instance, paper checks can help you track payroll quickly if you’re not ready for automated payroll software. “Paper checks remain a widely used alternative, particularly for businesses transitioning from traditional payroll systems or for employees who prefer physical checks,” said Shahnazari. “While slower and more prone to loss or fraud, they provide a tangible payment method for those who resist digital banking.”

Plus, smaller companies may benefit from the personal touch a paper check can provide. For example, you can touch base with your employees when handing out checks directly, automate the process by having your bank fill out and mail the checks or write a check on the fly if there’s an accounting mistake.

Paper check pros

Paper check cons

Paying employees with paper checks

You can order paper checks through your bank and personalize them with your business information. However, it’s advisable to open a dedicated payroll account so no other debited business expenses cause the account balance to fall below zero.

Fill out paper checks each pay period or have your bank’s bill-pay service mail them to your employees. If there are any discrepancies, you’ll have to void the checks and rewrite them.

Paying employees cash may save you fees, but it doesn’t always make sense. For example, even though you save money on payroll software and bank fees, tracking cash is challenging. If you have more than a few employees, electronic paycheck records make bookkeeping easier and help your small business avoid an audit. “Cash payments, while uncommon, can be an alternative for small businesses or gig workers,” said Shahnazari. “However, they come with security risks and potential compliance challenges, making them a less desirable option for large-scale payroll operations.”

Cash pros

Cash cons

Setting up a cash payment system

You’ll need a sound bookkeeping system in place to set up cash payments. Plus, you’ll need to withdraw ample cash from the bank to pay all of your employees in full on payday. Finally, you must keep impeccable records to avoid an IRS audit.

Amanda Hoffman contributed to this article.