Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

PayPal vs. Merchant Account: What’s the Difference?

PayPal and merchant accounts offer different ways to process customer payments — here’s how they compare.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Many businesses want to expand the payment methods they accept, so they obtain a merchant account from a payment processor or work with a payment facilitator like PayPal. Below, we’ll explain the differences between PayPal and merchant accounts to help you choose the right payment processing solution.

Searching for a credit card processor and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Did You Know?

PayPal credit card processing operates through a single company — PayPal. In contrast, merchant accounts are available from multiple providers.

What’s the difference between PayPal and a merchant account?

PayPal and merchant accounts both let businesses accept credit cards and digital payment methods, but they work differently and appeal to different types of businesses.

PayPal: PayPal acts as a payment aggregator, processing transactions without requiring a separate merchant account. However, fees can be higher, and you have limited control over how payments are handled. PayPal is a great option for newer businesses or those with lower transaction volumes. “PayPal is technically a payment aggregator, offering a secure and quick way for businesses to accept payments,” explained Michael Seaman, CEO of Swipesum.

Merchant accounts: A merchant account is a dedicated business account set up through a payment processor. The application process can be lengthy, but it offers lower transaction fees, greater customization, better scalability and more control over transactions. This makes it ideal for growing and high-volume businesses.

PayPal and merchant accounts also have different transaction rates and fees:

Merchant account

PayPal

Transaction Rate

Varies, but generally between 1.5% and 3.5%

Online via PayPal Checkout: 3.49% + 49 cents

In-person via PayPal Zettle: 2.29% + 9 cents

Alternative payment methods (e.g., Apple Pay): 2.89% + 29 cents

Note that PayPal’s fixed fee per transaction depends on the currency received. The amounts above reflect U.S. dollar transactions.

What to know about merchant accounts

The best credit card processors typically provide merchant accounts to their customers. Merchant accounts are the traditional way businesses accept credit cards.

What is a merchant account?

A merchant account temporarily holds customer payments before transferring them to your business bank account. The best merchant account services work with credit card processors to facilitate credit card and digital payment acceptance.

“A merchant account is your own. It’s like owning a home versus renting,” Seaman explained. “The underwriting process ensures stability, and you’re in control of your rates, integrations and cash flow. Plus, it can handle high volumes.”

Merchant account approval process: Unlike PayPal, merchant accounts require underwriting and approval. “A merchant account allows the business to control chargebacks and funding for risk management,” said Shane Hurley, CEO of RedFynn Technologies. “In contrast, PayPal can freeze and hold funds.”

If you meet the following criteria, you’ll have a good chance of obtaining a merchant account:

Merchant account transaction rates: All merchant accounts charge transaction rates, which include a percentage of the purchase amount plus a flat per transaction fee. These rates range from 1.5% to 3.5% of the transaction amount, plus 20 to 30 cents per transaction.

Additional fees: Some merchant account providers charge a monthly fee for account maintenance, customer service or statement processing along with additional processing fees. These can include PCI compliance fees (a required security feature), payment gateway fees for e-commerce transactions and incidental fees like chargeback fees, refund fees or account termination fees.

Merchant account dashboard and virtual terminal: The credit card processor provides a dashboard where you can see all transactions and create reports. Many include a virtual terminal at no extra cost, though some may charge a fee for access or per-transaction use. A virtual terminal lets you manually input card information for phone or mail orders or when a card’s chip or magnetic stripe isn’t working.

Tip

Retailers and restaurants will need the best POS systems with compatible card processing hardware, such as mobile card readers.

How does payment processing work with a merchant account?

“When a customer makes a payment, whether that’s by credit card, debit card or [another method] — it doesn’t magically land in your business bank account,” Seaman explained. “The money first flows into your merchant account. This is when processing happens.”

Here’s how it works:

A customer initiates a transaction.

The business accepts the customer’s credit card or digital payment method.

The payment processing system sends the transaction information to the processor.

The processor forwards the transaction data to the customer’s card-issuing bank, which approves or declines the transaction.

If approved, the card-issuing bank transfers the funds to the business’s merchant account, where they are temporarily held.

The payment processor batches approved transactions and transfers the funds to the business’s bank account, typically within one to three business days.

Merchant account pros and cons

Merchant accounts offer flexible features that can be tailored to a business’s unique needs.

“You control your funds, your rates and your flow of cash,” Seaman explained. “[Merchant accounts] offer features like recurring billing, multi-currency support and integration with your business management software, ERP or POS system.”

Additional pros include the following:

Lower transaction rates compared to PayPal and other payment facilitators

More cost-effective for businesses with high sales volumes

Lower chargeback fees (with tools to help manage disputes)

Fewer account holds and freezes

Faster payouts, typically within one to three business days

A branded merchant account experience that builds more customer trust

Advanced fraud prevention measures

Control over your customers’ online shopping cart data

The downsides of merchant accounts include:

Complex and lengthy application processes

Strict approval criteria, which make it harder for new businesses or those with low credit scores to qualify

Potential extra costs, such as monthly fees and gateway fees

Higher PCI compliance costs

FYI

PCI compliance fees vary by processor, but they usually cost between $75 and $120 per year.

What to know about PayPal

PayPal is a payment facilitator that allows businesses to accept credit cards without a dedicated merchant account. PayPal processes transactions under its master account and assigns businesses individual accounts within its system, instead of providing businesses with their own merchant account.

What is PayPal?

PayPal began as a peer-to-peer money transfer tool and grew into a comprehensive financial platform for consumers and businesses.

According to PayPal’s fourth-quarter 2024 earnings report, the platform processed $437.8 billion in total payment volume, handling approximately 70 million transactions per day.

PayPal has expanded its merchant services, offering a growing range of business solutions. As of 2024, PayPal has approximately 35 million active merchant accounts.

How does payment processing work with PayPal?

As a credit card facilitator (also called a payment aggregator), PayPal uses one master merchant account, and each business operates as a submerchant under that account. PayPal handles transaction processing through its Payflow Payment Gateway (Payflow Link or Payflow Pro), which connects to card networks, issuing banks and other payment providers.

Here’s how it works:

A customer initiates a transaction using PayPal, a credit card or another accepted payment method.

PayPal’s Payflow Payment Gateway processes the transaction and sends the details to the appropriate card network (Visa, Mastercard, etc.).

The card network communicates with the customer’s issuing bank, which either approves or declines the transaction.

If approved, funds are transferred to PayPal’s master merchant account.

PayPal credits the payment to your business’s PayPal account.

You can either keep funds in your PayPal account to pay business expenses or manually transfer them to your bank account (unlike a merchant account, this step is not automatic).

PayPal is sensitive to potential fraud and chargebacks since all businesses share PayPal’s master merchant account. PayPal may freeze your account if your business experiences multiple chargebacks in a short period. You can opt for PayPal’s chargeback and seller protection services (available for an additional cost) to reduce the risk of account holds and chargeback fees.

Did You Know?

PayPal credit card fees don't include some of the additional costs associated with traditional merchant accounts, such as monthly service fees. However, PayPal does charge for chargebacks and cross-border transactions.

What is PayPal Zettle?

PayPal Zettle is PayPal’s POS solution, which includes the Zettle mobile card reader, the Zettle terminal and a POS app. Businesses can use Zettle’s hardware and software to accept in-person and NFC mobile payments (credit and debit cards, PayPal, Venmo and more) while tracking sales and managing inventory.

PayPal pros and cons

Using PayPal for payment processing has some advantages, including the following:

Easy signup and approval process

Suitable for international businesses

Preferred by PayPal users, increasing conversion rates

Seamless integrations with GoDaddy, Wix, Shopify and more

Enables buy now, pay later options for customers

The downsides of PayPal include:

Restrictions on high-risk industries

Strict fraud detection may result in sudden account holds or frozen funds

Limited customer support with long wait times

High chargeback fees

Choosing between PayPal and a merchant account

Both PayPal and traditional merchant accounts allow you to accept multiple forms of payment and provide payment processing software and hardware.

“Small businesses, startups or low-volume sellers can use PayPal,” Hurley advised. “Traditional merchant accounts are essential for scaling businesses, high-volume sales, and industries with complex payment needs.”

Consider the following use cases and the best solution for each.

Best for businesses that

Merchant account

PayPal

Are startups or very small businesses

No

Yes

Are established businesses

Yes

No

Have low transaction volumes

No

Yes

Have high transaction volumes

Yes

No

Operate in high-risk industries

Yes

No

Sell internationally

No

Yes

Run e-commerce stores

No

Yes

Want control over shopping cart data

Yes

No

Consider a merchant account if:

Low costs are a priority: Hurley said, “Compared to PayPal’s flat fees, merchant account rates are lower and can be adjusted for high-volume sales.”

You want more control over your finances: Hurley noted that merchant accounts give business owners direct control over funding, chargebacks and dispute resolution — without relying on a third-party platform like PayPal.

You’re an established business in a stable industry: Merchant accounts have stricter approval criteria, so having an established business history and a good track record with credit card processing improves your chances of approval.

You have a high transaction volume: “For businesses with higher volumes, relying solely on PayPal is like trying to run a marathon in flip-flops,” Seaman cautioned. “It’ll get you started, but it’s not built for the long haul. That’s where a merchant account shines. Lower fees, no shared risk, and the ability to scale.”

Consider using PayPal if:

You’re a startup or low-transaction business: PayPal is an excellent option for startups, small businesses and those with low transaction volumes.

You have an online-only business: PayPal integrates with most e-commerce platforms, offers user-friendly payment tools and is easy to set up online payments.

You conduct business internationally: PayPal simplifies cross-border transactions and supports multiple currencies.

You’re in a high-risk industry: PayPal is more likely to approve businesses in high-risk industries. Still, be aware that your funds could be frozen or your account suspended if you have too many chargebacks.

Stripe doesn’t require a long-term contract and offers transaction rates similar to PayPal’s (2.9% + 30 cents per transaction for domestic payments, plus an additional 1% for international transactions.) You’ll pay a $15 chargeback fee if a customer disputes a charge and requests a reversal. Our review of Stripe explains if the dispute is resolved in your favor, Stripe may refund this fee.

Square

Read our Square review to see why it’s one of the best mobile credit card processors with free basic service charges at 2.9% + 30 cents per online transaction and 2.6% + 10 cents per in-person transaction. For businesses needing more features, industry-specific plans for retailers and restaurants start at $29 per month, with premium options exceeding $165 per month.

Shopify Payments

Shopify is a leading e-commerce platform with built-in payment processing through Shopify Payments. Pricing starts at $39 per month, with plans reaching $399 per month, plus processing fees ranging from 2.5% to 2.9% + 30 cents per transaction. Read our Shopify review to see how it’s an excellent choice for POS tools and inventory management.

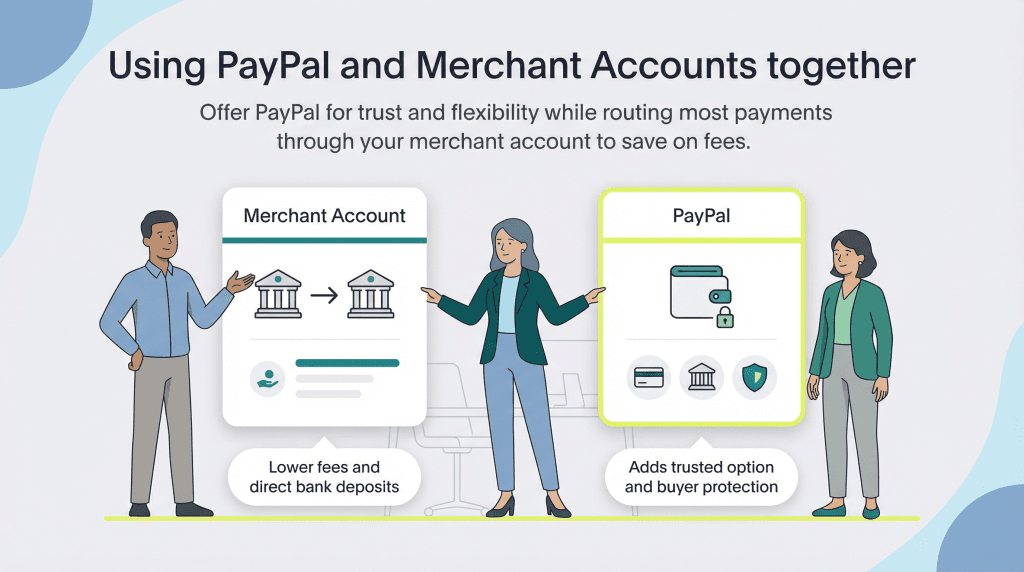

PayPal and merchant accounts: Can you use both?

While PayPal is convenient for buyers, businesses with high transaction volumes benefit from a merchant account’s lower processing fees and direct bank deposits. If you use both, you’ll likely route most payments through your merchant account, only keeping PayPal for customers who prefer it.

“Think of PayPal as adding another payment option that many customers trust, especially in industries like e-commerce and online services,” Seaman explained. “This is because PayPal lets customers pay with stored balances, linked cards, or even directly through their bank accounts without sharing card details. For customers, that’s peace of mind and buyer’s protection.”

Jennifer Dublino is an experienced entrepreneur and astute marketing strategist. With over three decades of industry experience, she has been a guiding force for many businesses, offering invaluable expertise in market research, strategic planning, budget allocation, lead generation and beyond. Earlier in her career, Dublino established, nurtured and successfully sold her own marketing firm.

At business.com, Dublino covers customer retention and relationships, pricing strategies and business growth.

Dublino, who has a bachelor's degree in business administration and an MBA in marketing and finance, also served as the chief operating officer of the Scent Marketing Institute, showcasing her ability to navigate diverse sectors within the marketing landscape. Over the years, Dublino has amassed a comprehensive understanding of business operations across a wide array of areas, ranging from credit card processing to compensation management. Her insights and expertise have earned her recognition, with her contributions quoted in reputable publications such as Reuters, Adweek, AdAge and others.