Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Business owners should understand payroll-related payments, taxes and more.

Payroll liabilities are commonplace in day-to-day business. Whether you’re paying employees, using a payroll service or facing IRS penalties, it’s easy to get overwhelmed by the complexities of running payroll.

We’ll walk you through the basics of payroll liabilities and provide tips for streamlining your payroll.

Searching for payroll software or services and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Payroll liabilities are payroll-related payments you must pay for your business. These liabilities include employee-earned wages your workers haven’t yet received, employee taxes and payroll service costs.

Payroll liabilities are present in every payroll you run. However, most companies pay their payroll responsibilities quickly and use the best online payroll services.

The terms “payroll liability” and “payroll expense” sound similar, but they have some key differences.

“The difference between a payroll liability and a payroll cost is whether it’s been paid yet,” Hayden Cohen, CEO of Near, said. “If you owe money to another party for payroll-related expenses, those are liabilities. Once those liabilities have been paid, they’re considered expenses.”

Payroll liabilities include tax withholdings, benefit deductions, retirement contributions and union dues. You must calculate each liability accurately and send it to the proper authority. After you take all payroll deductions from your employees’ gross pay, they receive their net pay. Net pay is the actual dollar amount your employees receive for their work. Net pay can be distributed via cash, check or direct deposit.

It is essential to know your specific payroll liabilities. Running payroll reports and analyzing them monthly will help you create an accurate budget, understand your labor costs and manage your small business’s cash flow.

Although liabilities vary from business to business, we’ll examine the most common payroll liabilities you’ll likely encounter.

Employees are an integral part of your business. To keep your employees and reduce turnover, you must pay them real wages on time. “Employee wages are payroll liabilities until they’ve been paid,” Cohen explained. “Generally, you only count money that your employees have earned or are contractually owed, rather than projected future wages.”

Wages compensate employees for work they’ve accomplished during a pay period. You’ll determine how often to run payroll: Daily, weekly, biweekly or bimonthly. Before you run payroll, all unpaid employee wages are liabilities because you still owe that money.

Payroll tax withholdings are another integral payroll obligation. All employers must file payroll taxes and contribute these taxes for every worker they hire.

Here is a breakdown of payroll taxes, including those required by the Federal Insurance Contributions Act (FICA), the Federal Unemployment Tax Act (FUTA) and the State Unemployment Tax Act (SUTA):

All employees must complete IRS Form W-4. When your employee fills out a W-4, it helps you determine their withholding allowances. The worker’s gross wages are also a factor in tax contributions.

Generally, payroll taxes are paid quarterly. However, because payroll taxes aren’t immediately sent to the IRS or state or local agencies, they are considered liabilities until deposited.

All businesses that invest in payroll software or a professional employer organization (PEO) have liabilities in payroll service costs.

When working with payroll software, you may pay your service costs at the end of every month or the beginning of the following month, similar to credit card or utility bills. PEO costs may have monthly or yearly contract fees.

“Payroll service costs include things like paying for payroll software, printing paper checks if that’s something you still do or hiring an outside company to handle your payroll,” Cohen said. “These are all liabilities until they’ve been paid.”

Payroll companies have various pricing structures. It’s important to compare payroll software costs before you sign up because one pricing structure may be less expensive than another.

Here are the six payroll software pricing structures:

Depending on the employee benefits you offer and your employees’ current financial liabilities, you may have to account for several other payroll liabilities, including the following:

All contributions and withholdings are payroll liabilities until you transfer money to the correct agencies.

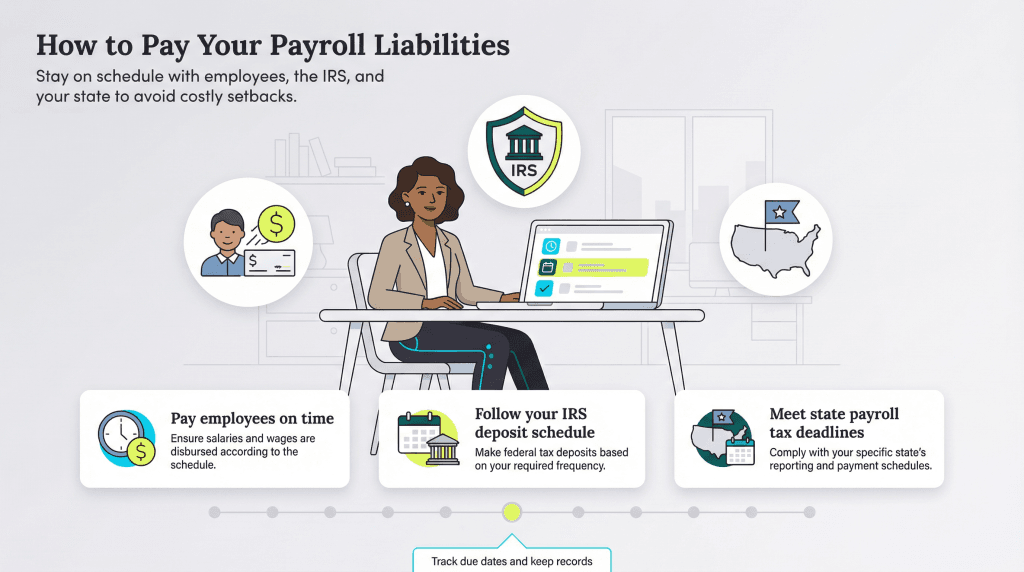

If you neglect your liabilities, your company could face serious setbacks. All payroll liabilities should be paid accurately and on time to the correct recipients. Here’s how to do it.

Pay employees’ wages using your employer-designated pay schedule. Employees depend on the money they receive to pay bills and purchase food and gas. Once you’ve completed onboarding successfully, analyze a new hire’s payroll for insurance premiums, tax contributions and garnishments.

Deposit all federal tax liabilities according to your specific depositing schedule. The IRS bases your depositing schedule — either monthly or semiweekly — on your previous fourth-quarter tax period.

Most companies use the electronic federal tax payment system to deposit tax liabilities. If you’ve invested in a payroll tax filing service, it will take care of your tax deadlines.

State tax liabilities are similar to federal taxes in that you pay your state payroll tax using the state-specific depositing schedule.

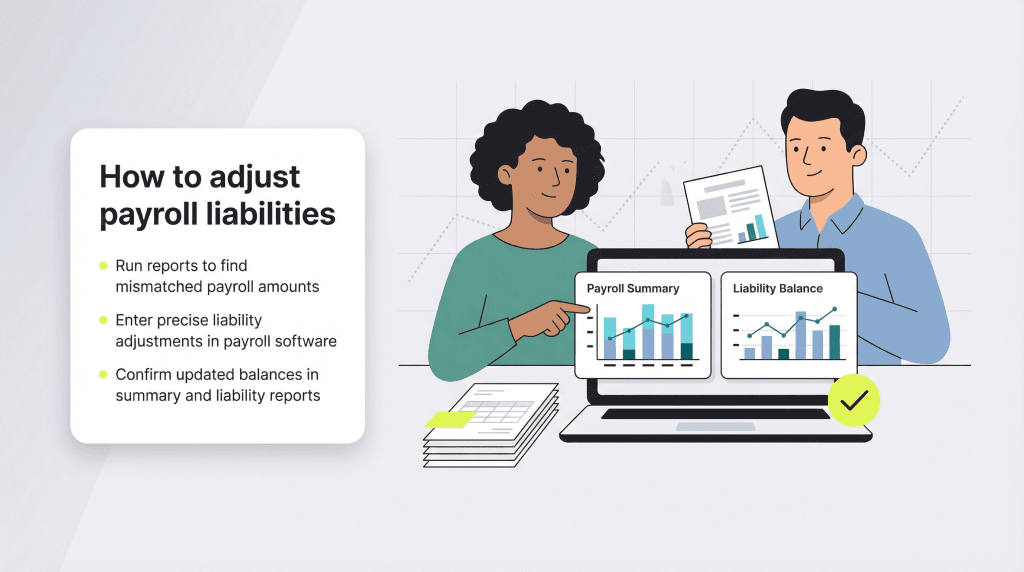

If your payroll liabilities don’t match up, you must make adjustments. Here are some common reasons for a payroll liability adjustment:

How you adjust payroll liabilities depends on whether you modify them manually or automatically through payroll software. For example, if you complete payroll manually, you can enter an adjustment for any liability. However, if you use a payroll service, you won’t adjust any payroll liabilities that the service oversees, such as federal and state tax liabilities. You may be able to modify local or other taxes that are not supported by your payroll service if the software or your subscription plan allows it.

Here are the basic steps for completing an employee payroll liability adjustment using QuickBooks:

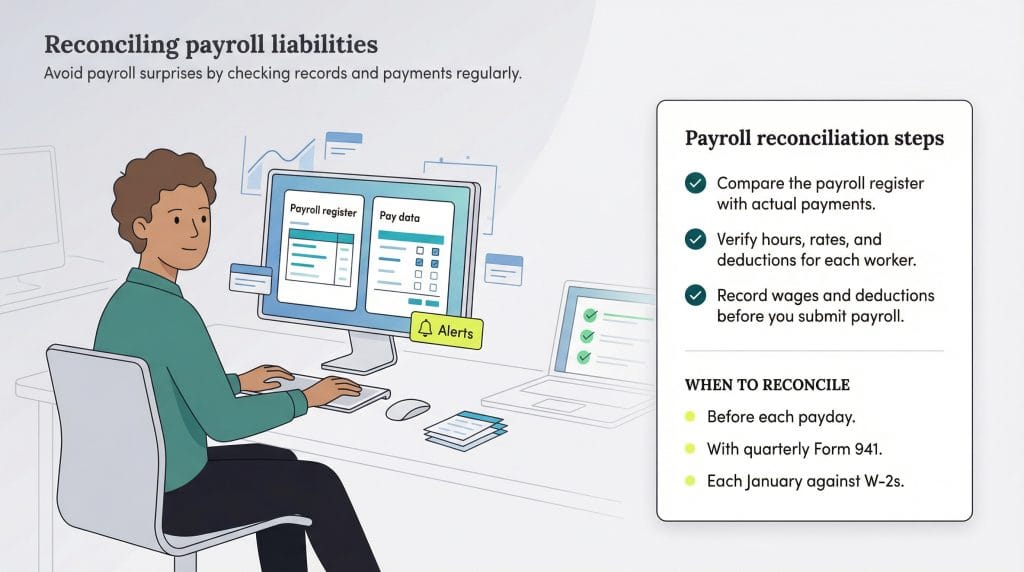

Payroll reconciliation double-checks your calculations to ensure your employees are paid accurately. To do this, compare your payroll register with the amount you pay the staff member by cash, check, direct deposit or a direct deposit alternative.

Here’s how to complete a payroll reconciliation:

Here is the schedule for payroll reconciliation:

Payroll reconciliation helps you prevent disgruntled employees, avoid financial penalties and fines from the IRS and keep your books current. Payroll is a significant portion of a business’s overhead costs, so it’s essential to get it right. Payroll software can streamline reconciliation and alert you to any errors.

Amanda Hoffman contributed to this article.