Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Employer Health Insurance: Average Employee Health Insurance Cost in 2026

Discover how employer-sponsored health insurance works, including current rates and what prices in 2025 mean for employers.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Employee health insurance benefits are a must-have for many workers. While health benefits are available through health insurance marketplaces or federal programs, the cost of private health insurance has gone up, leaving many Americans without viable options outside of employer-sponsored coverage. This means the insurance benefits an employer offers as part of a compensation management program — as well as how the costs of that insurance are shared — can directly impact a business’s ability to hire and retain the right people.

Below, we break down the current state of employer health insurance costs in the U.S., strategies to keep expenditures down, and what health insurance prices in 2025 mean for employers.

Current costs of employer-sponsored coverage (2025)

According to the Kaiser Family Foundation (KFF) 26th Employer Health Benefits Survey, the average annual premium for an employee in 2024 for employer-sponsored health coverage increased by 6 percent to $8,951 for single coverage, and $25,572 for family coverage, up another 7 percent from the previous year. On average, employees covered $1,368 (16 percent) of the premium for single coverage and $6,296 (25 percent) for family coverage, slightly less than in 2023.

Employers typically cover the bulk of these premiums. Aon projected the average employer health insurance cost to surpass $17,000 per employee in 2026, a 9.5 percent jump from 2025. These costs vary widely depending on the plan type, business size, and location.

Some employers are seeking to decrease their employees’ healthcare expenses by covering treatments or expanding what they offer. These services could be considered fringe benefits, such as:

Telehealth behavioral mental health services

Specialty drug access, including GLP-1 drugs for weight loss

IVF and other family planning services

Concierge services

Health and wellness promotions within the workplace

Access to centers of excellence

Working spouse surcharges

Cost trends and what’s ahead

Healthcare insurance costs continue to rise each year, outpacing general inflation. In 2025, employer health insurance costs are projected to increase by up to 9%. This annual increase is even greater than the 6.4% increase seen between 2023 and 2024.

Small-to-midsize businesses can expect to see the largest jumps in year-over-year insurance costs, with some projections suggesting a 9% rise for companies with 50–499 employees. Driving these increases are not just inflation, but also changes in medical service utilization and prescription drug spending.

Who pays what? Employer vs. employee cost share

Coverage Type

Employee Monthly Contribution

Employer Monthly Contribution

Employee Share (%)

Employer Share (%)

2024 Annual Premium

2025 Projected Premium*

Single Coverage

$132

$668

16

84

$8,951

~$9,525

Family Coverage

$625

$1,650

25

75

$25,572

~$27,000

*Projections based on anticipated 6 to 7% increases.

Employees benefit from lower-cost premiums through employer health insurance. On average:

Employers shoulder about 84 percent of premiums for single coverage and roughly 75 percent for family coverage, according to the KFF Employer Health Benefits Survey.

Employees pay the remainder: about $132 a month for single coverage and $625 a month for family coverage.

For the year, the average employee’s share comes out to $1,368 (single) or $6,296 (family).

Premiums are just one piece of the picture. Shared financial responsibility also includes:

Health savings accounts (HSAs): Tax-free savings for medical expenses, with both employers and employees able to contribute, and funds that can be rolled over year-to-year.

Flexible spending accounts (FSAs): Pretax accounts set aside for healthcare costs; these typically must be used by year-end.

Deductibles and copays: Employees must pay out of pocket for medical care up to the deductible before insurance covers additional costs. The average deductible for single coverage is about $1,787.

Coinsurance: Employees are often responsible for 20% or more of costs after meeting the deductible.

Shared employer and employee health insurance costs help keep coverage accessible, but shifting more costs to workers can impact recruitment and retention, especially as premiums and out-of-pocket costs continue to rise.

FYI

While healthcare costs for employers continue to increase across the board, the amount still varies by industry. For example, according to Aon data, the communications and technology industries experienced the highest percent increase (7.4 percent), while the retail and wholesale trade industry saw just 2.4 percent.

What’s driving health insurance cost increases?

Several factors fuel the rising price of employer-sponsored coverage each year:

Medical and prescription inflation: Rising medical service costs and the increased use of specialty drugs—especially weight-loss and diabetes medications like GLP-1s—are major contributors.

Healthcare worker shortages and provider consolidation: Labor shortages have driven up wages in the health sector, while hospital and provider group consolidations reduce competition and drive up prices.

Coverage expansion and plan design: Employer demand for enhanced benefits, such as expanded mental health and family-building coverage, adds to plan costs.

Return to pre-pandemic healthcare usage: Increased demand for medical services after deferred care periods means higher costs for insurers.

Regulatory effects: Transparency in health plan pricing and shifting government requirements contribute to cost volatility.

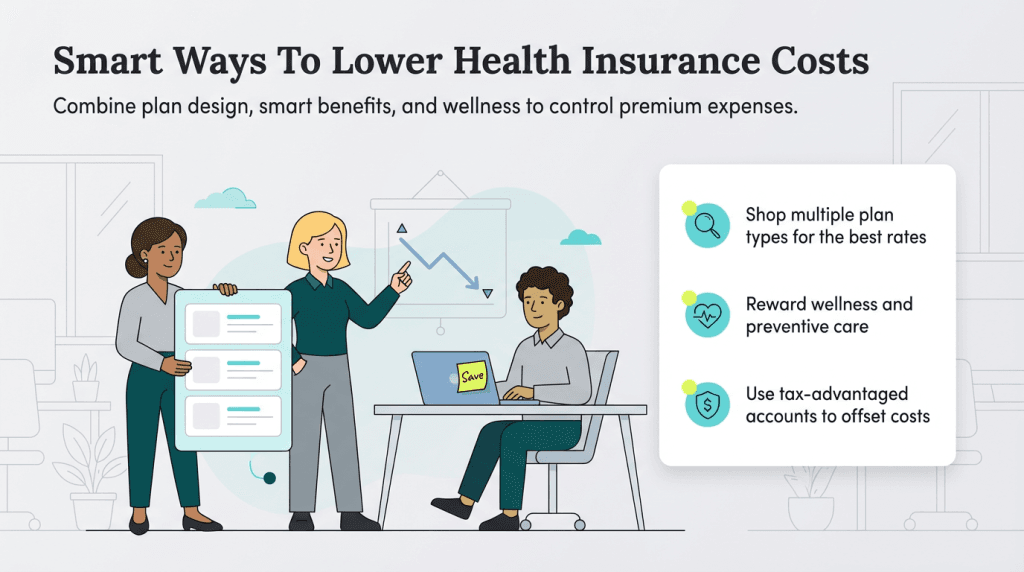

Strategies to manage premium costs

Business owners can use proactive tactics to minimize health insurance costs for themselves and their employees:

Shop around with an insurance agent or broker: Options like group health-sharing, traditional group plans, ACA marketplace plans, or level-funded plans may help lower costs. “By having the opportunity to learn and compare from multiple carriers, you can be sure you are getting the best benefits structure with the best rates available,” said Michael Stahl, former chief marketing officer at UnitedHealthcare.

Encourage proactive healthcare habits: Employees who take part in exercise programs or see primary care doctors regularly may qualify for premium discounts or rebates through some insurers.

Shift cost-sharing to employees: Choosing plans with higher deductibles or out-of-pocket expenses can reduce business owner costs, but may affect employee satisfaction and retention. [Related article: How Much Workers’ Comp Insurance Do You Need?]

Encourage prescription drug discounts: Employees can save significantly by choosing generic medications and seeking direct discounts or coupons from pharmaceutical companies.

Consider HRAs, HSAs, and FSAs: Exploring benefit account options may help defray costs while reducing tax burdens for both businesses and employees.

Implement workplace wellness programs: Incentives for preventive care and healthy habits can lead to lower overall claims, keeping premium costs in check.

FAQs: Employer and employee health insurance costs

In 2025, average annual employer health insurance cost per employee is expected to surpass $16,000, with most businesses covering over 75% of premium costs.

Employees typically pay $1,368 (16%) for single coverage or $6,296 (25%) for family coverage per year; higher for plans with lower employer contributions.

Yes. Most projections suggest a 5.8% to 9% increase in premiums for 2025, depending on employer cost-control efforts.

Employers may increase their share of premium costs, offer reimbursement arrangements (HRAs), promote wellness and prevention, and regularly review plan options with a broker.

Through employer health insurance, employees can receive substantial discounts on their health insurance premiums. Employers often subsidize the cost of the insurance plans they offer, making them significantly more affordable to their employees, who can usually sign up for the insurance plan through the company’s HR department.

Most employees have a limited selection of employer health insurance plans, with companies often providing either health maintenance organization (HMO) plans, preferred provider organization (PPO) plans, or both.

“Employer health benefits are such a crucial part of attracting and retaining talent,” Stahl said. “It is essential to get it right.”

Sean Peek contributed to this article. Source interviews were conducted for a previous version of this article.

For almost a decade, Max Freedman has been a trusted advisor for entrepreneurs and business owners, providing practical insights to kickstart and elevate their ventures. With hands-on experience in small business management, he offers authentic perspectives on crucial business areas that run the gamut from marketing strategies to employee health insurance.

At business.com, Freedman primarily covers financial topics, including debt financing, equity compensation, stock purchase agreements, SIMPLE IRAs, differential pay, workers' compensation payments and business loans.

Freedman's guidance is grounded in the real world and based on his years working in and leading operations for small business workplaces. Whether advising on financial statements, retirement plans or e-commerce tactics, his expertise and genuine passion for empowering business owners make him an invaluable resource in the entrepreneurial landscape.