Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Determining the right level of workers' compensation coverage is a balancing act. Too much coverage can strain your budget, while too little leaves your business exposed to serious liability.

As a business owner, part of the job is managing risk, including following best practices, complying with applicable laws and carrying the right business insurance. If you have employees, that includes workers’ compensation (also called workman’s comp or workers’ comp) coverage.

But figuring out how much coverage to carry isn’t always straightforward. Carrying more insurance than you need can tie up capital, while not having enough leaves your company dealing with expensive claims and potential legal headaches if something goes wrong. Here’s a closer look at the factors that influence your coverage needs and how to choose a policy that makes sense for your business.

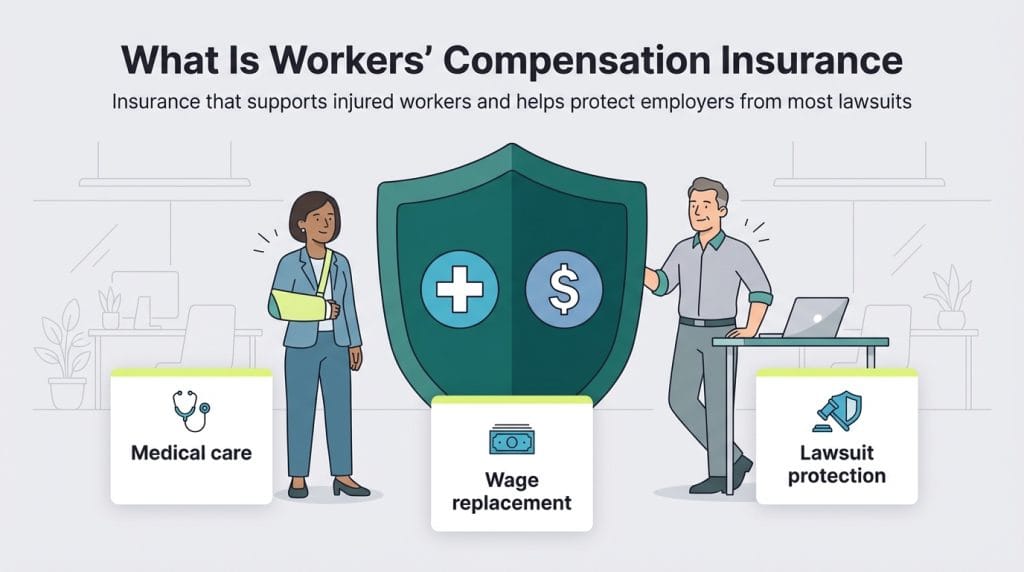

Workers’ compensation insurance is coverage that provides benefits and protection for employees who are injured in a workplace accident or become ill on the job. It helps ensure workers receive medical care and wage replacement and, in most cases, protects employers from direct legal action after a work-related injury or illness. Workers’ comp works much like other types of business insurance: Employers pay into a policy or state-managed system, and benefits are paid out if a covered incident occurs.

“When employees are injured on the job, workers’ compensation provides financial coverage for their medical bills, lost wages and other expenses,” said Jeff Somers, a startup founder and product leader with experience building and scaling early-stage companies. “In addition to protecting employees, workers’ compensation limits employers’ exposure to lawsuits after work-related injuries.”

Figuring out how much workers’ compensation coverage you need isn’t a one-size-fits-all process. The right amount depends on several factors, including state requirements, payroll size and the level of risk tied to your industry. While insurance brokers or agents can help guide the process, understanding what affects your rate makes it easier to spot gaps or unnecessary costs.

To estimate your total workers’ compensation insurance cost, start by asking the following questions.

Workers’ compensation requirements are set at the state level. Texas is the most notable outlier and allows most private employers to opt out of workers’ compensation coverage, though “nonsubscribers” there face different liability risks. In many other states, coverage is required as soon as you hire your first worker, whether they are full-time or part-time employees.

“Since workers’ compensation laws are regulated at the state level, business owners should first determine when workers’ compensation insurance is required for their business,” Somers advised. “Usually, it’s as soon as they hire an employee.”

Some states allow workers’ comp exemptions if you are the sole employee of your business. Somers suggests weighing the potential cost of a workplace injury against the price of coverage before relying on that exemption.

“Since most health insurance plans exclude coverage for work-related injuries, sole proprietors may be putting their livelihood on the line if they opt to skip workers’ comp coverage for themselves,” Somers cautioned.

The average age of your workforce can influence workers’ compensation risk because injury patterns, experience levels and recovery timelines tend to shift as teams skew younger or older. Insurers don’t price policies strictly by age, but changes in workforce demographics can affect the types of claims a business may see over time.

Quinten Lovejoy, founder of The 300 Group, noted that both younger and older teams bring different risks. “As employees age, the propensity for injury increases,” Lovejoy said. “At the same time, a younger workforce brings about less experience and an increased chance of on-the-job injury.”

An aging workforce is becoming more common across many industries. Bureau of Labor Statistics projections show participation among older workers is expected to continue rising through the early 2030s, changing the risk profiles employers need to consider.

The level of risk tied to your employees’ daily work plays a major role in how much workers’ compensation coverage is needed. Insurers look closely at job duties because higher-hazard roles tend to produce more frequent or more severe claims.

“With higher levels of risk comes the need for high levels of coverage,” Lovejoy said. “A roofing contractor obviously has a higher risk than someone working in a jewelry store.”

Occupational hazards are often the biggest driver of cost differences because insurers assign classification codes — standardized job categories developed by the National Council on Compensation Insurance (NCCI)— to estimate injury risk. Each code carries a base rate per $100 of payroll that can vary widely by industry. For example, clerical office roles may fall below about $0.20 per $100 of payroll in some markets, while higher-risk work such as framing or roofing can reach $8 to $14 or more per $100 of payroll, depending on the state and carrier.

Following strong safety practices can help reduce claims over time. Maintaining OSHA compliance (standards set by the Occupational Safety and Health Administration) may also help lower risk, although higher-hazard industries will typically have to pay higher premiums regardless of prevention efforts. According to OSHA, falls remain the leading cause of death in construction, followed by struck-by incidents, electrocutions and caught-in/between hazards — collectively known as the “Fatal Four.”

Understanding the financial exposure your business faces can help you decide how much workers’ compensation coverage makes sense. Medical costs, wage replacement rules and state benefit requirements vary widely, which means the real cost of a claim and its impact on your premiums can look very different depending on where you operate.

When reviewing your coverage, consider the types of financial risk your business could face, such as:

Additionally, you’ll face even more financial risks if you don’t carry required workers’ comp coverage. Penalties vary by state, but employers may face fines, stop-work orders or retroactive premium charges if an audit finds coverage should have been in place.

The size of your workforce can influence workers’ compensation costs, but not always in the way business owners expect. Premiums aren’t based on headcount alone. Payroll totals and the type of work employees actually do tend to matter more. As teams grow, though, there’s simply more opportunity for injuries to happen, and that can influence claims patterns over time.

In practical terms, adding employees often means higher total payroll and a broader mix of job duties, two factors that insurers use when calculating workers’ comp premiums.

Workers’ compensation pricing can look confusing at first because there isn’t a single national rate. Costs vary widely depending on where your business operates, the type of work employees perform and how insurers evaluate risk. Instead of focusing on one average price, it helps to understand the factors that shape premiums and why quotes can differ so much from one company to another.

Insurers typically look at a few core factors when calculating workers’ compensation premiums: payroll totals, job classification rates and a company’s experience modification rate (EMR). The exact formula can vary by state and carrier, but these elements form the foundation of most pricing models.

While pricing models differ slightly between insurers, premiums are often illustrated using a simplified formula:

Classification rate × EMR × (Payroll ÷ 100) = Estimated premium

Workers’ comp premiums aren’t entirely within a business owner’s control. The type of work your team performs and your claims history both play a role in pricing, and those factors can feel frustrating when you’re trying to manage costs. Still, many companies find there are practical ways to reduce risk over time and keep premiums from climbing faster than expected. Consider the following:

Managing workers’ compensation coverage isn’t just about choosing the right policy; it also comes down to how consistently a business reviews risks, communicates with employees and responds when incidents occur. The practices below can help companies stay organized, support injured workers and avoid unnecessary premium increases over time.

Kimberlee Leonard and Jennifer Dublino contributed to this article. Source interviews were conducted for a previous version of this article.