Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Cutting corners on business insurance is inadvisable; however, there are methods to lower insurance premiums without compromising coverage.

Balancing small business operations and costs is challenging, especially when considering essential expenses like business insurance. According to a survey by Next Insurance, 90 percent of small business owners are unsure if they have the right amount of coverage, with 96 percent of them unable to show that they comprehend the basics of small business insurance.

Understanding the average costs of insurance — and determining if you’re overpaying — can help you best meet your financial goals, based on your specific business needs. These 14 cost-saving tips will empower you to make informed decisions on reducing your insurance premiums.

Paying for business insurance can add up — reaching over $4,000 annually on average for small businesses. Here are several ways you can save:

Commercial insurance providers evaluate risk using algorithms that can spit out very different quotes from the same information. That means you could find substantially lower rates without changing your coverage simply by shopping around. However, don’t always just look at the price. “A great agent will focus on loss prevention and secure the best coverage at competitive rates,” explained Chris Peterie, CEO and co-founder of Tower Street Insurance.

How often should you get quotes for your business insurance policy? Most financial experts recommend you do it annually. [Learn more about the best business insurance providers]

A business owner’s policy (BOP) combines several common types of protection (property, business interruption and some liability) into a single plan. “Bundling often leads to more cost-effective premiums than purchasing each policy separately,” according to Dennis Shirshikov, adjunct professor of economics at City University of New York.

However, read the policy carefully before you sign. Many BOPs don’t include auto insurance or professional liability insurance, and most don’t cover workers’ compensation. You could need separate policies for these.

Some commercial insurance providers also sell home and auto insurance. Why does that matter? Carriers often provide discounts when you buy multiple lines of coverage. If yours does, you could save big without touching your coverage.

Take a thorough look at your policy and ensure you don’t have coverage you don’t need. If you don’t use a vehicle for your business, for example, you likely don’t need commercial auto insurance. If you don’t have employees, you don’t need employment practices liability coverage. Make sure you’re not insuring yourself against a risk you don’t face.

Many policyholders of all types don’t realize the relationship between their deductible and their premium. In a nutshell, all other factors being equal, the lower your deductible is, the higher your premium will be.

So, a good way to lower your premium is to raise your deductible. However, you’ll have to pay that deductible before you receive any help on a claim, so make sure you set it at an amount that you can come up with in a hurry.

Another benefit of this is that the higher deductible will discourage you from filing smaller claims. “The decision to raise a deductible should be based on a cost-benefit analysis. If the premium savings divided by the increased out-of-pocket exposure makes financial sense, it may be worthwhile,” according to Peterie.

Providers love policyholders who don’t file claims. If your business has been claims-free for years, you could be eligible for a discount. This is why it’s a good idea to avoid filing smaller claims. Be sure to ask about this as you’re evaluating carriers.

Talk with your provider about ways you can reduce risk in your business. These include starting a workplace safety program, instituting disaster preparations and initiating a theft-prevention plan. All of these will reduce the risk of a claim, which is why you might get a price break.

“Insurers reward businesses that take tangible steps toward mitigating risk,” noted Shirshikov. Each insurer is different, so review the loss-prevention programs with your agent.

Many providers offer group rates for businesses that fill the same niche. Ask if your provider does; if not, explore purchasing commercial insurance through a professional organization. You might have to pay a fee to join the organization, but you can recoup that quickly through reduced premiums. Plus, membership in the professional group could give your business a higher profile and may lead to important contacts with peers.

This varies by provider, but you can reap substantial savings by paying your premium in full upfront. Commercial auto insurance providers, for example, may discount a year’s premium by up to 15 percent if they get paid in a lump sum. You could also authorize an electronic funds transfer.

Another great method of saving money on business insurance is being proactive. This means you need to go above and beyond to protect all elements of your business. This will eliminate risks, which can prevent accidents and reduce your insurance costs.

Although it may seem counterintuitive, the cost of the policy is not always the most important part of an insurance policy. Rather, you should make sure that you have all the coverage you need. If you don’t, you may save some money on your monthly premium. But, if and when you have some sort of accident, you could end up paying much more in the long run.

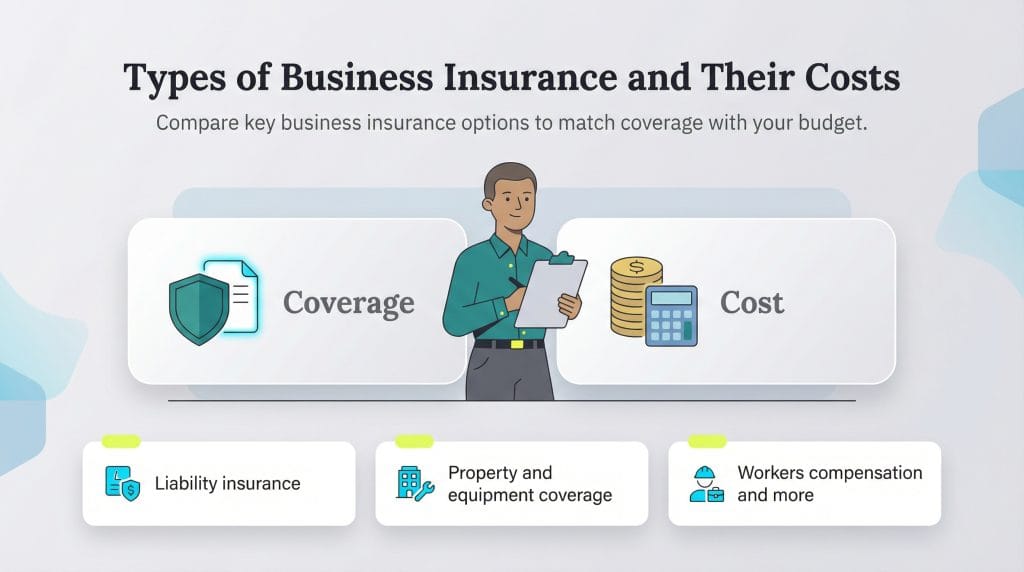

It can get overwhelming and expensive when choosing business insurance. If your risk of a certain type of loss isn’t great, you may not need some types of insurance. Take a look at the common policies and what they cover to help you decide.

A credit score is not always factored into a commercial insurance policy. However, some states allow insurers to use your credit history when rating a commercial auto policy, so good credit will help you get a lower rate. While a lower credit score won’t disqualify you from getting insurance, a higher one can help you get certain discounts.

Do a risk assessment of your business to see what your biggest risks are, and design insurance coverage to cover those risks. You may want to enlist the expertise of an insurance agent or risk assessment expert. They can determine your biggest risks and offer advice on how to reduce them as well as the best ways to protect yourself from losses. For example, a small business may not need as much coverage as a bigger company. Get the appropriate amount and right type of insurance.

By treating your commercial insurance as a planned expense instead of an afterthought, you might be able to reduce the amount you spend while maintaining full coverage. It takes a strategic approach to accomplish this mission, but it could well be worth it to your bottom line.

One of the best ways to safeguard your business from the unexpected is to know what types of business insurance are available. In some cases, certain businesses are required to have specific insurance to ensure compliance with legal requirements.

This guide explains the different types of business insurance, what’s covered and how much you can expect them to cost:

Insurance policy type | What it covers | Cost per month |

|---|---|---|

General liability | Third-party claims of property damage, bodily injury, and libel and slander | $30-$42 ($360-$504/year) |

Professional liability | Claims that an employee did not do their job to professional standards, leading to a loss | $60 ($720/year) |

Business property, such as furniture, electronics, materials, supplies and inventory | $83 ($996/year) | |

Business owners | Combination of general liability, commercial property and often business interruption insurance | $57 ($684/year) |

Business interruption | Lost revenue and expenses when a business is shut down because of a claim | $50-$150 ($600-$1,800/year) |

Internet-based risks that could lead to hacking or data breaches | $145 ($1,740/year) | |

Vehicles used for commercial purposes | $50-$208 ($600-$2,496/year) | |

Claims for employees injured on the job | $45-$70 ($540-$840/year) |

Selecting the right business insurance policy involves a careful assessment of your specific needs, balancing comprehensive coverage with cost considerations to protect your business’s future effectively.

Sean Peek contributed to this article.