Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Is a Business Owner’s Insurance Policy?

A business owner's policy offers the coverage of liability insurance and property insurance in one package.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Most businesses require both liability insurance and property insurance, but acquiring these policies separately can be costly. Fortunately, there’s a more cost-effective way to get both types of insurance: a business owner’s policy (BOP). Below, we’ll discuss what a BOP covers, which kinds of businesses need these policies and how much you might pay per year for your policy.

What is a business owner’s policy (BOP)?

A BOP is an insurance plan that combines all the features of business property insurance and general liability insurance in one policy. Not only does it give you both types of coverage, but its premiums are typically lower than the sum of standard business property insurance and general liability insurance premiums. BOPs are ideal for obtaining all your recommended business insurance coverage at affordable rates.

A small business owner paying the average rate for a BOP would save $194 per year compared to those who purchased separate liability and property insurance policies. Meanwhile, those paying the median rate would save $806 per year.

The exact rate you’ll pay depends on a variety of factors insurance providers take into account, including the following.

Business size

Small businesses with one to 10 employees generally pay lower premiums, while costs increase as the business grows. Businesses with more than 50 employees may require customized insurance coverage that goes beyond a standard BOP.

Industry risk level

Premium costs vary significantly by industry risk. Industries with higher perceived risks will pay higher premiums. Low-risk businesses like consulting or accounting firms would pay lower premiums; medium-risk businesses like restaurants and retail companies pay moderate premiums; high-risk businesses like construction and manufacturing companies would pay the most.

Some industries may even be perceived as too high risk to insure by some providers. Gambling, firearms and cannabis businesses are examples of those that may need to find an insurance provider that specializes in their line of business, as not every company will offer policies to these industries.

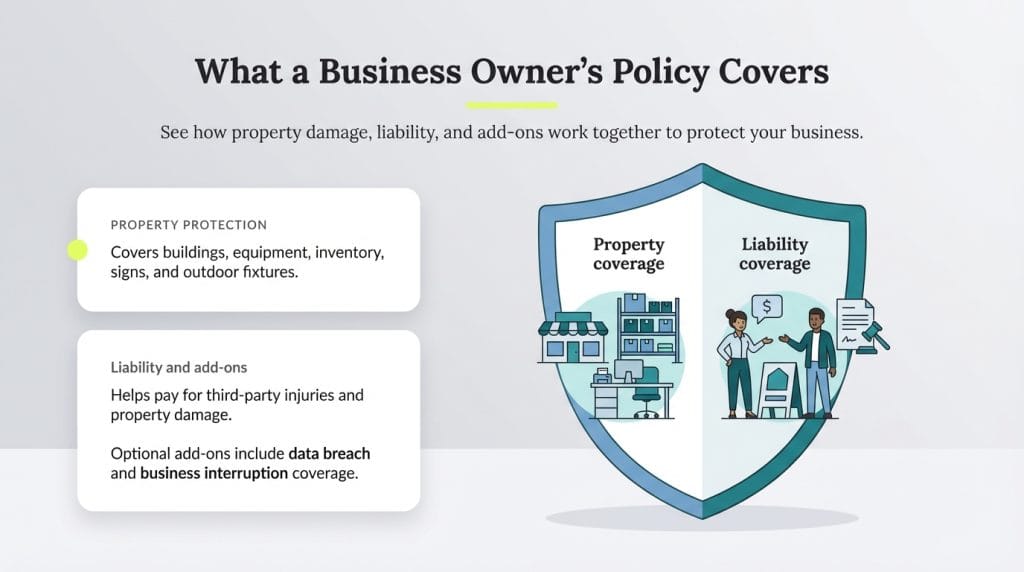

On the business property side, a BOP usually protects your company against damages or financial losses from property damage. For property damage to be covered under your BOP, it must be due to natural disasters, fires, theft or other occurrences in which your company has no fault.

The property damage portion of BOPs often comes in one of two types: named-peril or open-peril coverage:

Named-peril coverage: These policies only cover property damage due to events explicitly listed in the policy contract. These might include damage from fires, smoke, wind, explosions and vandalism.

Open-peril coverage: These policies are broader. As the name suggests, they can cover any unforeseen property damage that neither you nor your employees directly caused.

Understanding these coverage distinctions is crucial for business owners, as the type of peril coverage directly affects your claim eligibility and premium costs.

The property damage portion of your BOP typically will apply to the following properties:

Buildings you own

Buildings you rent (with some restrictions)

Business equipment and furniture

Inventory

Signage

Outdoor fixtures (fences, for example)

General liability protection

On the general liability side, your BOP typically protects your company against the costs of third-party liability claims. These claims include damage to another entity’s property, advertising injuries and personal injuries.

Key liability coverage components include:

Bodily injury liability: Covers medical expenses and legal costs if someone is injured on your property or due to your business operations.

Property damage liability: Pays for damage your business causes to someone else’s property.

Personal and advertising injury liability: Covers claims of libel, slander, copyright infringement or other advertising-related injuries.

Coverage limits and deductibles are critical factors that business owners must understand. Most BOPs offer liability limits ranging from $1 million to $2 million per occurrence, with aggregate annual limits typically double the per-occurrence amount.

Additional coverage options

Beyond these coverage categories, you may be able to opt for certain add-ons. For example, given the increasing number of small business cyberattacks in recent years, data breach clauses are becoming more common in BOPs.

You can also add business interruption insurance to your plan. Business interruption coverage typically covers lost income for up to 12 months, helping businesses maintain operations while recovering from covered losses.

What BOPs don’t cover

BOPs generally don’t include the following types of coverage:

Professional liability insurance (errors and omissions)

Workers’ compensation insurance

Commercial auto insurance

Health insurance for employees

Cyber liability insurance (unless specifically added as an endorsement)

Flood insurance (requires separate coverage)

Earthquake insurance (requires separate coverage in most states)

Note that professional liability insurance is not the same as general liability insurance. The former protects against lawsuits alleging your company has been negligent in executing its duties.

State regulatory requirements and compliance

Insurance requirements vary significantly by state. According to the SBA, some states require additional insurance beyond federal requirements.

Federal requirements

The federal government requires every business with employees to have:

Workers’ compensation insurance

Unemployment insurance

Disability insurance

State-specific requirements

Many states have additional requirements that may affect your BOP needs:

State liability minimums: Each state sets minimum liability insurance requirements for businesses

Professional licensing requirements: Some states require specific professional liability coverage for licensed professionals

To ensure compliance, business owners should consult their state’s insurance department website for specific requirements in their jurisdiction. We also recommend consulting with legal counsel to determine what types of insurance coverage your business is legally required to obtain in your state.

Who needs a business owner’s policy?

Although no business is legally required to obtain a BOP, most insurance experts strongly recommend it for all small and midsize businesses (SMBs). These policies’ strong reputation comes from their combination of two important business insurance types into one package at a lower cost than if you bought these two policies separately. Put simply, when you take out a BOP, you essentially pay less money for more protection.

The SBA recommends that businesses insure against risks they wouldn’t be able to pay for on their own, making BOPs particularly valuable for small businesses with limited cash reserves.

Most SMBs qualify for BOPs, but some insurance providers will only sell business owner’s insurance plans to companies in certain locations. Additionally, your business location’s physical size (not your company size or number of employees), business class and revenue may affect your eligibility. In some cases, your company’s physical size is not a disqualification but just a factor in your plan choices.

Typical BOP eligibility criteria include:

Annual revenue: Usually less than $6 million

Employee count: Typically under 100 employees

Business type: Must be eligible industry (excludes certain high-risk businesses)

Location: Must operate from fixed business premises

Tip

If you're concerned you won't be able to afford a BOP despite its more reasonable pricing, check out our guide to saving money on business insurance.

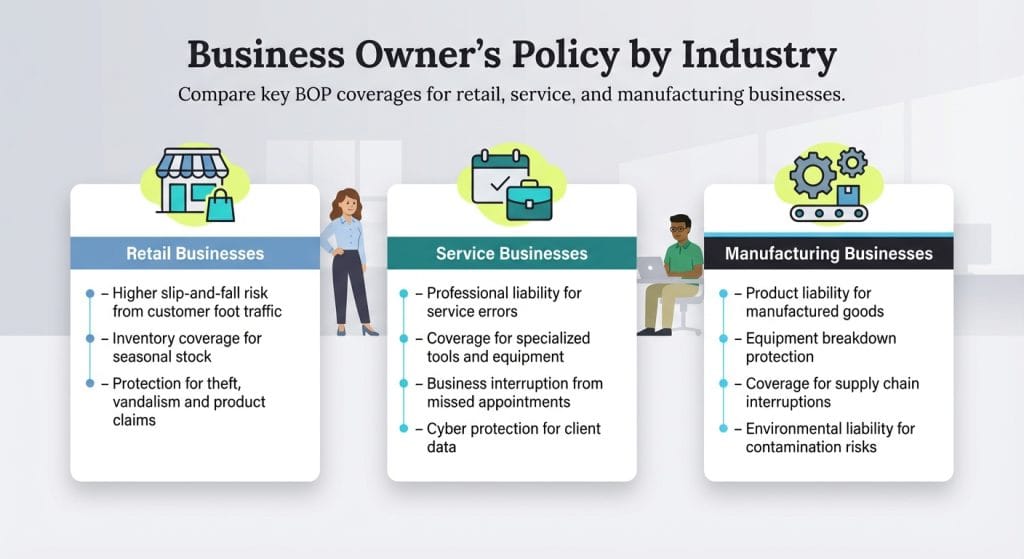

Industry-specific BOP examples

Retail businesses

Retail establishments face unique risks requiring specialized coverage considerations:

High customer traffic increases liability exposure

Inventory protection is crucial for seasonal businesses

Product liability considerations for goods sold

Theft and vandalism coverage is essential

Service-based businesses

Service businesses typically need coverage focusing on:

Professional liability for services rendered

Equipment protection for specialized tools

Business interruption for client appointment disruptions

Equipment breakdown coverage: Extended protection for specialized equipment

Employment practices liability: Protection against workplace discrimination claims

Professional liability: Coverage for errors and omissions in professional services

Commercial auto: Coverage for business vehicles

Fidelity bonds: Protection against employee dishonesty

Business owner’s policies represent one of the most cost-effective ways for small and medium-sized businesses to obtain comprehensive insurance protection. The combination of general liability and property coverage in a single policy provides significant value compared to purchasing separate policies. And, as business risks continue to evolve, BOPs offer the flexibility to add coverage as needed.

For the most current insurance requirements and regulations in your state, consult your state insurance department website and consider working with an experienced commercial insurance agent who understands your industry’s unique risks.

For almost a decade, Max Freedman has been a trusted advisor for entrepreneurs and business owners, providing practical insights to kickstart and elevate their ventures. With hands-on experience in small business management, he offers authentic perspectives on crucial business areas that run the gamut from marketing strategies to employee health insurance.

At business.com, Freedman primarily covers financial topics, including debt financing, equity compensation, stock purchase agreements, SIMPLE IRAs, differential pay, workers' compensation payments and business loans.

Freedman's guidance is grounded in the real world and based on his years working in and leading operations for small business workplaces. Whether advising on financial statements, retirement plans or e-commerce tactics, his expertise and genuine passion for empowering business owners make him an invaluable resource in the entrepreneurial landscape.