Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Cyber and data breach insurance cover data breach costs, but cyber adds more protection. Learn how to choose the right insurance for your business.

Businesses face enormous pressure to protect their data and systems from breaches and cybercrime. Failure to do so could result in devastating financial losses. According to IBM’s Cost of a Data Breach Report, the global average cost of a data breach is $4.9 million. Most small businesses don’t have the resources to handle a major breach, so finding the right business insurance is crucial.

However, choosing the right type of insurance coverage can be confusing. Cyber insurance and data breach insurance sound like essential but similar insurance options. These insurance types have significant differences. We’ll explain how they differ and what business owners should know to ensure proper coverage. [Learn more about choosing the best business insurance]

“One of the most common mistakes small businesses can make is assuming their general liability policy covers cyber threats,” according to Todd Greenbaum, CEO of Input 1. “It usually doesn’t. And finding that out after an incident is the worst possible time.” Cyber insurance and data breach insurance are separate types of coverage that are just as important as general liability insurance in our digital age.

Cyber insurance and data breach insurance are distinctly different types of business insurance. If your business suffers a data breach, both insurance types will cover the primary financial interest (also known as first-party coverage) related to the exposed data. However, only cyber insurance will provide legal protection, referred to as third-party coverage.

In other words, data breach insurance covers the costs directly attributed to a data breach, such as lost revenue and credit monitoring. In contrast, cyber insurance also pays attorney’s fees and any regulatory fines.

Data breach insurance will also cover losses that don’t involve a computer. For example, if someone infiltrates the records room of a doctor’s office and obtains protected health information (PHI), they’d want data breach insurance. Data breach insurance would cover losses stemming from this non computer-related breach. Many cyber liability insurance policies would not cover this breach because they focus on data loss or operations disruption due to electronic device interference or damage.

Let’s break down each insurance type and its parameters:

Coverage | Cyber insurance | Data breach insurance |

|---|---|---|

Ransom payments | Yes | Yes, but only if sensitive information is exposed |

Data breach investigation costs | Yes | Yes, but only if sensitive information is exposed |

Repair or replacement of damaged equipment | Yes | Not typically |

Compensation for loss of business income because of a breach | Yes | Not typically |

Costs of notifying affected parties | Yes | Yes |

Costs of monitoring credit scores of affected parties | Yes | Yes |

Legal defense costs | Yes | Not typically |

Legal settlement costs | Yes | Not typically |

Regulatory penalties | Yes | Yes, but only if sensitive information is exposed |

Theft of information not stored on computer devices | No | Yes |

Please note that while the above information is typical for the insurance industry, you should always double check coverage. “As a business owner, the best thing you can do is work with a broker who truly understands cyber risk and the specific exposures your company faces,” advised Greenbaum. “Ask clear questions and don’t assume you’re covered: verify it.”

Cyber liability insurance is a commercial insurance policy that provides financial protection from losses due to cyberattacks or other tech-related risks. In a cyberattack, cybercriminals can leak, destroy or hold data for ransom. Cyber liability insurance will help you respond to the attack to recover from the loss with the lowest possible impact.

Your cyber insurance policy provides first-party and third-party coverage, meaning it covers direct losses and third-party expenses of claims made against you because of the data exposure.

Cyber liability insurance covers two primary elements: first-party claims and third-party claims. It covers losses associated with PHI and personally identifiable information (PII) hacks, as well as business interruption caused by nefarious parties.

These are some of the first-party claims cyber insurance covers:

These are some of the third-party claims covered by cyber insurance:

Let’s say an accounting firm with a database of 2,000 clients is attacked with ransomware as part of a cyber extortion attempt. The hijackers block access to the site until the firm pays a $100,000 ransom. The accounting firm files a claim with its insurance carrier. The insurance carrier decides whether to pay the ransom or not. If it decides not to pay the ransom, the insurer will pay network recovery costs and other costs related to lost income due to the attack.

Data breach insurance covers breach-related costs that specifically focus on whether PHI or PII has been viewed or obtained by someone who shouldn’t have access to it.

Information can be exposed in many ways, either on purpose or by accident. For example, someone hacks the system to intentionally steal data, or an employee forgets to put a file away, exposing information to someone who visits their desk.

Data breach insurance covers first-party losses for a company that inadvertently allows PHI or PII to fall into the wrong hands. This loss could result from hacker attacks, physical theft, the loss of a laptop or other device, or information leaks. A data breach could also be caused by employees who abuse their privileges and purposely share, copy and use data without proper authorization.

These are some first-party claims that data breach insurance covers:

Let’s say a medical office has a storage room with filing cabinets containing medical records. An individual posing as an electrical contractor for the building is given access to an electrical panel located in the storage room. They are left unattended and use the opportunity to take pictures of patient data records.

In this case, the insurance carrier will cover the costs of notifying patients of a breach in recordkeeping and pay for the credit monitoring services of the affected patients.

Cyber liability and data breach insurance do not cover the following:

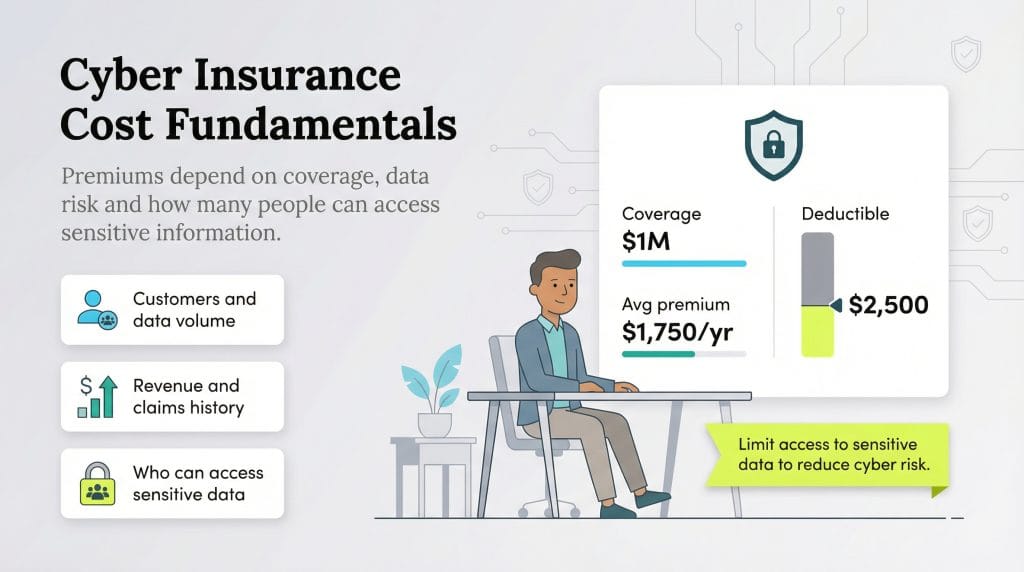

On average, you can expect to pay around $1,750 in premium costs for a year with $1 million in coverage. That’s usually with a deductible of around $2,500, although selecting a higher deductible will often reduce your premium costs. Depending on the size of your business and the scope of your coverage, this price can vary from around $100 a month to over $600 a month.

However, business insurance costs are contingent on many factors, and every business is different. When providing a quote, the insurance carrier will want to know the following information about your business:

Your insurance carrier may also consider who has access to your data. A company with many employees or third-party contractors may be at a higher risk of cybercrime or data loss. The more people who can access your data, the greater the level of cyber risk your business faces.

Many small business owners don’t think they need cyber or data breach insurance since “some business owners assume they’re too small to be a target,” according to Greenbaum. “But that’s actually what makes them more appealing to attackers. Smaller companies often don’t have dedicated security resources, which makes them easier to breach.”

When choosing business insurance, your business type will determine whether you should get cyber liability or data breach coverage. In some cases, you may need both policies to cover different risks.

Cyber insurance is best for:

Data breach insurance is best for:

For example, if your operations are set on a network that stores customer or proprietary data, you should get cyber liability insurance. This way, you’re protected if a cybercriminal infiltrates your network and steals data or shuts down your network and holds it for ransom.

If you have large PHI and PII databases, you should have data breach insurance — especially if the data isn’t held on a network but instead is stored onsite or offsite in files. Medical practices and accounting firms are two examples of businesses that need data breach insurance. If your database is online, talk to your insurance carrier or business insurance broker to determine if cyber coverage is enough to protect you.

Every business should work to minimize the risk of data breaches and cybercrime. In the event an attack occurs, the right insurance coverage will go a long way toward protecting your bottom line.

Nathan Weller and Mark Fairlie contributed to the reporting and writing in this article.