Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

If a customer is hurt on your premises, they can sue you. But general liability insurance can protect your business.

As a business owner, you’re responsible for the work you and your employees do, as well as for your customers’ health and safety while they’re at your workplace. As a result, a client can sue your company if they’re injured or their property is damaged in the course of doing business. General liability insurance provides financial protection from legal claims brought against your business.

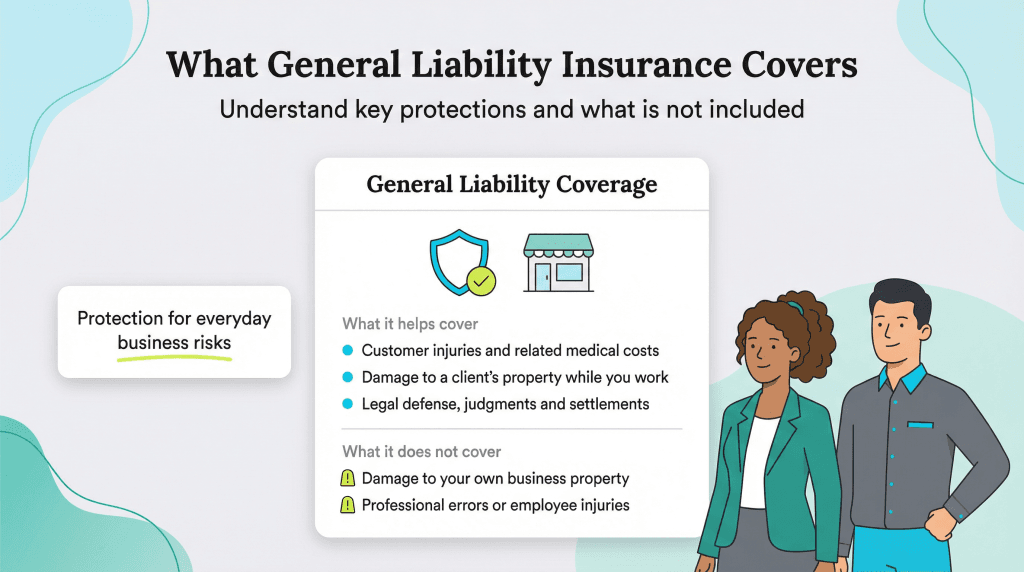

General liability insurance, also known as commercial general liability insurance, provides coverage against claims that may arise when a third party is injured on your premises — for example, if a customer trips on the carpet in your store and hurts their arm — or an employee accidentally damages a customer’s property. General liability insurance doesn’t protect against claims that relate to professional errors or business practices.

Business owners who sell products or provide services to customers need general liability insurance. “Every business should consider having a general liability insurance policy, as it’s often a prerequisite for establishing important business relationships,” advised Chris Peterie of Tower Street Insurance.

A significant number of small businesses will face property or general liability claims due to unexpected incidents and accidents. General liability insurance can protect a business against the costs associated with property or general liability claims.

Here are some types of businesses that need general liability insurance:

Businesses that engage in the following activities or business situations could also benefit from general liability insurance:

Most states do not require a business to maintain general liability insurance legally. However, each state has its own insurance laws that affect what a business needs in its general liability insurance policy to ensure adequate coverage of costs related to legal claims.

Dennis Shirshikov, adjunct professor of economics at City College of New York, noted that only a few businesses can get away without getting general liability insurance. “Some single owners with no public-facing business may be able to avoid general liability, although this is becoming less popular and [is] not recommended,” Shirshikov explained.

General liability insurance provides coverage for the following types of claims:

General liability insurance helps to cover the following costs resulting from claims against your business:

General liability insurance does not cover the following:

Reputational harm and advertising injury aren’t as self-explanatory as other claim types, such as property damage and bodily injury. Here’s a breakdown of these potential risks:

Your business can be sued by a competitor if you or an employee makes false or unfounded claims about them. “Reputational injury refers to charges of slander, libel or defamation that hurt a person’s or organization’s reputation,” Shirshikov explained. These claims could result in a loss of customers, revenue and trust for that competitor.

General liability insurance can cover the legal costs involved in defending your business against the following types of reputational harm claims:

A third party can sue your business for perceived or actual offenses that arise in advertising your company, products or services. General liability insurance covers the legal costs associated with defending these claims. Advertising injury can occur through the following means:

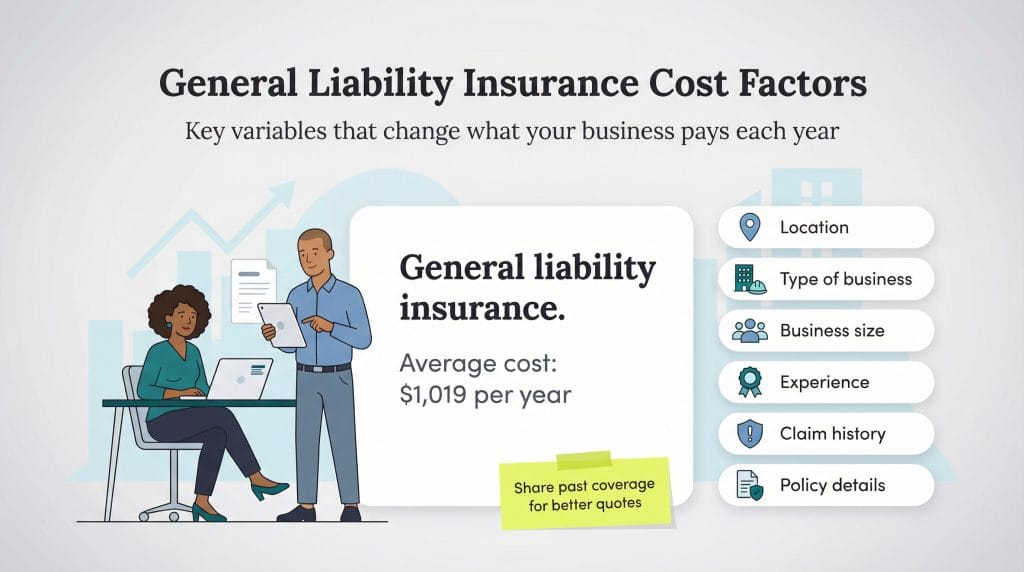

On average, general liability insurance costs $1,019 annually, according to The Hartford. However, the exact costs vary depending on the following factors:

Your policy provides coverage up to a certain limit. For most businesses, this falls into one of two categories:

Here are the steps you’ll take to select and purchase general liability insurance:

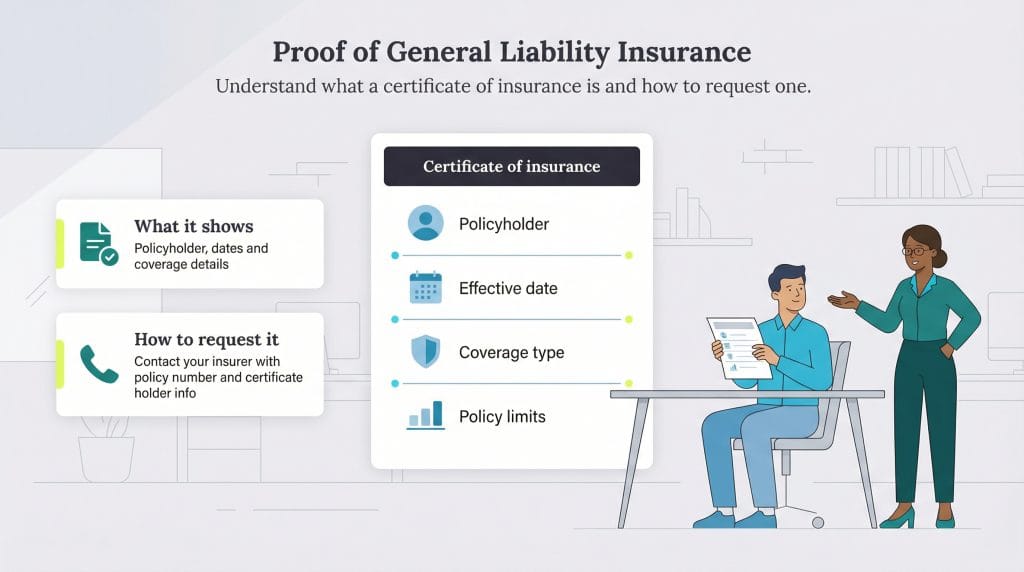

You might be required to show proof of general liability insurance when working with another business. In these instances, you typically need to show a certificate of insurance (COI).

A COI is a document that summarizes the key details found within an insurance policy. It also acts as verification of insurance and proof of specific insurance coverage.

A COI should include the following information:

To request a COI, contact your insurance company or broker and provide the following information:

Kimberlee Leonard contributed to this article.