Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Workers' compensation insurance is a key policy most businesses are required to have.

Workers’ compensation insurance can help protect your business and employees when an employee is accidentally injured or falls ill on the job. Each state has its own workers’ compensation laws for both employers and employees, so it’s important to know how the regulations affect your business. Furthermore, nearly every state requires workers’ compensation insurance for companies with at least one employee, with the exception of Texas, where workers’ compensation isn’t required by law. We’re breaking down what you need to know.

>> Read Next: Workplace Accidents — How to Avoid Them and What to Do When They Happen

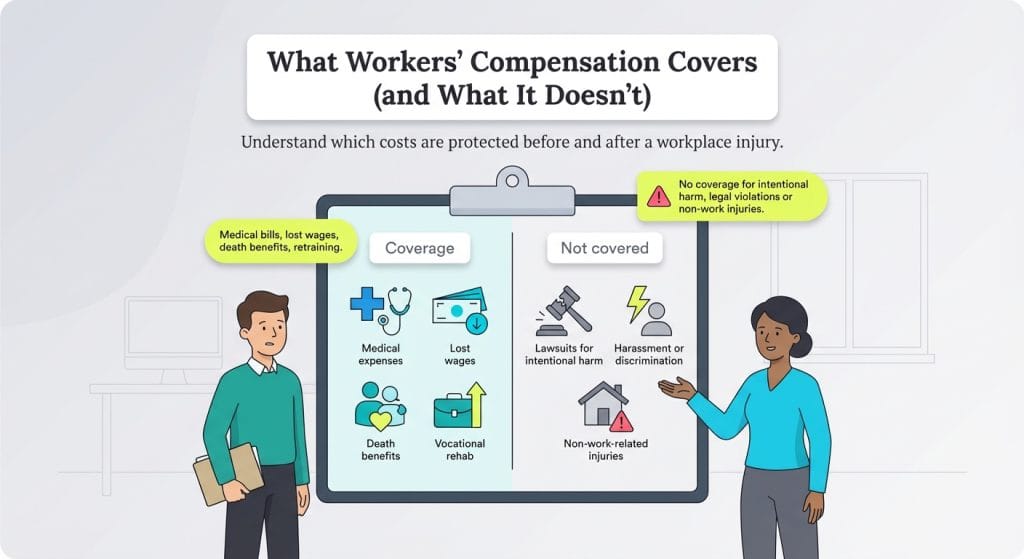

Workers’ compensation is a type of business insurance that provides benefits to employees who become injured or ill while doing their jobs. The insurance covers the employee’s medical costs, a portion of their lost wages while they’re out of work and their rehabilitation costs so they can return to work or find a new job.

Workers’ compensation insurance also protects the employer by limiting its liability for legal claims in the event an employee sues the business over an illness or injury caused by work-related incidents.

Workers’ compensation covers the following expenses.

Some insurance policies don’t provide workers’ compensation coverage across multiple states or when employees travel to different states. Under these circumstances, you would need workers’ compensation insurance in each state where your employees work or travel.

Workers’ compensation is a no-fault system. When an employee receives workers’ compensation for their injury or illness, they give up the right to sue their employer. However, workers’ compensation will not cover your business if you purposefully harm an employee, such as committing assault, battery, fraud, defamation or emotional distress or protect your business if your employee sues you for the following acts:

Workers’ compensation covers medical costs or death benefits that result from employee injuries that occurred while the employee was doing their job or acting on your behalf. Examples include injuries or illnesses related to the following:

Different states exclude certain situations from workers’ compensation coverage. Here are some examples of employee actions that would not qualify for workers’ compensation:

As with any commercial liability insurance policy, workers’ compensation has a limit or cap on the amount a policy will pay out for a claim. However, workers’ compensation limits are structured differently than other types of insurance policies. These policies place limits on employer liability and employee benefits:

State governments determine which types of employers must carry workers’ compensation insurance as well as the fines for not being covered, guidelines for reporting work-related injuries and medical care requirements. [Related article: How Much Workers’ Comp Insurance Do You Need?]

State laws determine the details involving workers’ compensation, including how much it costs. In all applicable states, employers pay for workers’ compensation insurance largely based on a percentage of their total payroll costs. On average, it works out to $1 per $100 of payroll. There are no employee payroll deductions for workers’ compensation insurance.

Below are some other factors besides payroll that affect the cost of workers’ compensation insurance:

Implementing strategic cost-reduction measures can significantly impact your workers’ compensation expenses while maintaining compliance and employee safety.

Develop comprehensive safety programs. Safety programs that can effectively prevent accidents and injuries will reduce the total number of workers’ compensation claims that are filed. Key safety program elements include:

Implement return-to-work programs. Delayed injury reporting can significantly increase workers’ compensation claim costs, with research showing costs can increase substantially when reporting is delayed beyond two weeks. Establishing effective return-to-work (RTW) programs can dramatically reduce claim costs. Successful return-to-work programs should include:

Focus on early injury reporting. Immediate reporting and care can reduce harm, reduce total settlement amounts and let your team know that their safety is your top priority. Establish clear procedures for immediate injury reporting and response. Best practices for injury reporting include:

Improve experience modification rates. Your experience modification rate (EMR) directly affects your premium costs. A strong safety program that reduces the frequency and severity of claims can reduce your EMR factor, which goes into the calculation for your annual workers’ comp insurance premiums. Strategies to improve EMR include:

Most businesses with one or more employees require some form of workers’ compensation insurance, except those in Texas, where workers’ compensation is optional. Whether your specific business and employees require this insurance will depend on the type of business and the status of your employees.

The following types of employees are likely to be exempt from a workers’ compensation insurance requirement.

Understanding workers’ compensation implementation timelines and deadlines is crucial for maintaining compliance and ensuring proper coverage. New businesses typically need one to three business days to secure workers’ compensation insurance after submitting a complete application. However, it’s important to plan ahead, as several factors can extend the timeline.

Coverage must be in place before your first employee begins work, and some insurers may require a workplace inspection before issuing a policy. High-risk businesses may face additional underwriting reviews, which can delay approval. Additionally, state-specific requirements may add processing time, making early preparation essential.

Employers must meet several critical deadlines when implementing workers’ compensation coverage.

Before hiring your first employee:

Within the first month of operation:

Ongoing compliance requirements:

State laws often impose shorter deadlines for reporting injuries to employers than for filing formal claims. For example, some states require injured workers to notify their employer immediately or within 24 to 48 hours, while others allow 30 to 90 days. In contrast, the deadline to file a formal workers’ compensation claim is usually one to three years from the date of injury, depending on the state.

Employers should be familiar with both sets of deadlines, as delays in reporting can lead to benefit denials or disputes. In cases involving occupational illnesses or repetitive stress injuries, the timeline may be based on when the symptoms were first recognized, rather than the actual date of exposure.

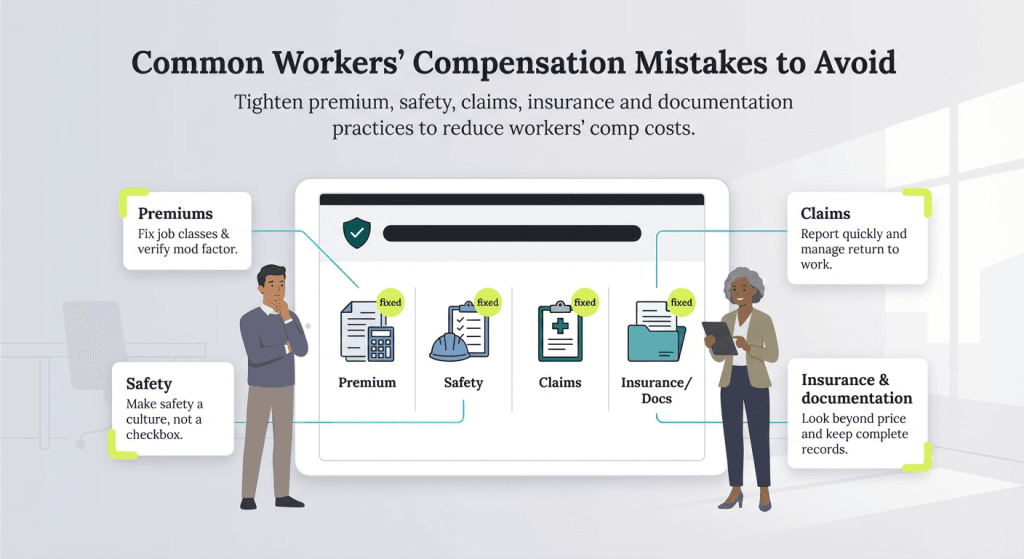

Avoiding common pitfalls can save businesses significant costs and compliance issues. These mistakes often result from lack of experience with workers’ compensation systems.

Most employers are unfamiliar with the complicated calculations that make up their total workers compensation cost. Small oversights can lead to significant overpayments. Common premium mistakes include:

To prevent this from happening, have an independent expert review all premium calculations annually and challenge any discrepancies.

A strong safety program is essential to reducing workplace injuries and lowering insurance costs. However, many employers make avoidable mistakes that weaken their safety efforts. Common safety program mistakes include:

How you handle workers’ compensation claims directly affects your overall costs. Poor processes can result in longer recovery times and higher premiums. Common claims management mistakes include:

When purchasing workers’ compensation insurance, it’s important that you look at the whole picture, not just how much it costs. Choosing a policy based only on price can leave your business exposed.

Mistakes in insurance selection include:

Thorough documentation supports the legitimacy of claims and helps protect your business during disputes or audits. Poor documentation practices can lead to claim disputes and increased costs:

Businesses can purchase workers’ compensation insurance from state-funded programs or private insurance companies. Each state determines its workers’ compensation policy requirements. When you purchase a policy, you’ll need to provide the following information so the insurer can determine your coverage and costs.

Each state has its own rules on what’s covered, how it evaluates different issues, how injured employees receive medical care and which benefits an employee can receive.

When an employee becomes injured or ill on the job, the first task is not to file a workers’ compensation claim — it’s to make sure the employee receives proper medical treatment. This may include calling an ambulance to take the injured or ill employee to the hospital.

Following that, the employer and employee have a limited amount of time — usually between 10 and 90 days — to submit the paperwork that’s required for the employee to receive workers’ compensation benefits. The process for filing varies from state to state. However, if the claim isn’t filed within the required time, coverage can be denied.

When an employee is injured or falls ill due to work, the employer must do the following:

The employer must also provide the employee with information on their rights and workers’ compensation benefits, as well as the procedure for returning to work.

After the illness or injury occurs, the employee must take the following steps:

A workers’ compensation claim should include the following information:

The time required to complete a workers’ compensation claim depends on state requirements, the time needed to investigate the claim and other factors. Once the employer files the claim, the insurance provider must determine whether to approve or reject the claim.

If the insurance provider approves the claim, the company will provide the affected employee with payment details. The insurer can deny the claim if it doesn’t qualify for workers’ compensation benefits:

Note that you may want to talk to a tax advisor about how a workers’ comp claim can affect taxes.

Kimberlee Leonard contributed to this article.