Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Workers' compensation has tax implications that every employee and business owner should understand.

When an employee receives workers’ compensation benefits, they generally don’t have to pay state or federal taxes on the money. However, tax rules vary by state, and in some cases, employees may need to report the income on their tax return. Because the rules can be complex, it’s always best to consult a tax advisor when receiving workers’ compensation benefits.

For both employers and employees, there’s some basic information worth knowing. Here’s a look at workers’ compensation insurance and the tax implications of workers’ comp benefits.

Editor’s note: Looking for the right workers’ compensation insurance for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

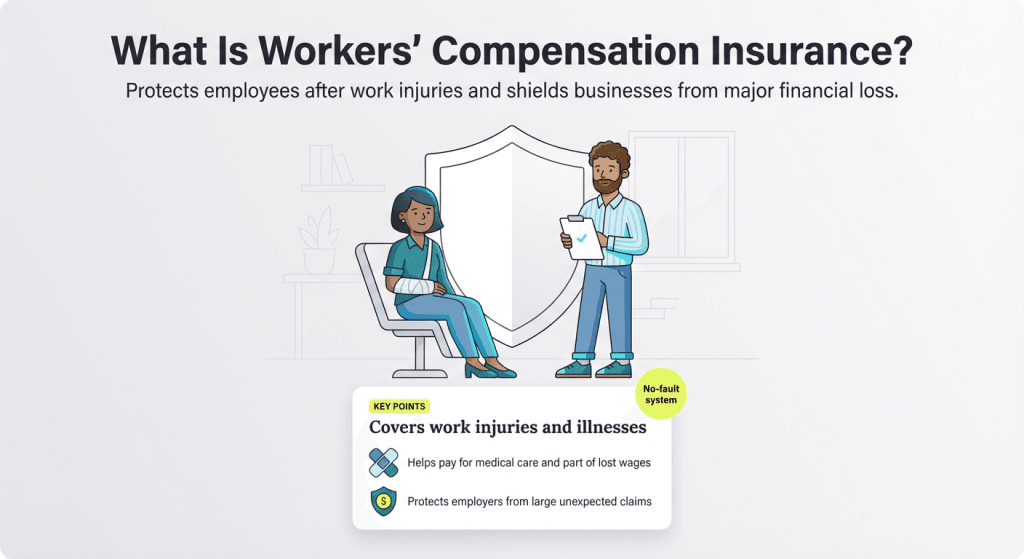

Workers’ compensation insurance is a business insurance policy that provides financial and medical benefits to employees who experience job-related injuries or illnesses. It is mandatory for employers in most U.S. states.

Chris Heerlein, CEO of REAP Financial, said that beyond legal requirements, workers’ comp insurance protects businesses from unexpected costs that could derail operations. “I’ve witnessed small employers face six-figure claims that, without coverage, would have put them out of business,” Heerlein noted. “[Workers’ comp insurance] also signals to employees that their safety and well-being are taken seriously, which impacts morale and retention.”

Each state where workers’ compensation insurance is required has its own laws and regulations, so coverage and program details vary. For example, in Alabama, employers must offer workers’ comp if they have five or more regular employees. In Idaho, the threshold is just one employee, even if that employee is occasional, seasonal, part-time or full-time.

The program is designed to ensure workers receive the care and financial support they need while recovering from a job-related injury or illness. During their time away from work, benefits cover a portion of lost wages as well as medical expenses.

While the process varies somewhat by state, workers’ comp generally follows these steps:

Here are some important things to remember about workers’ comp:

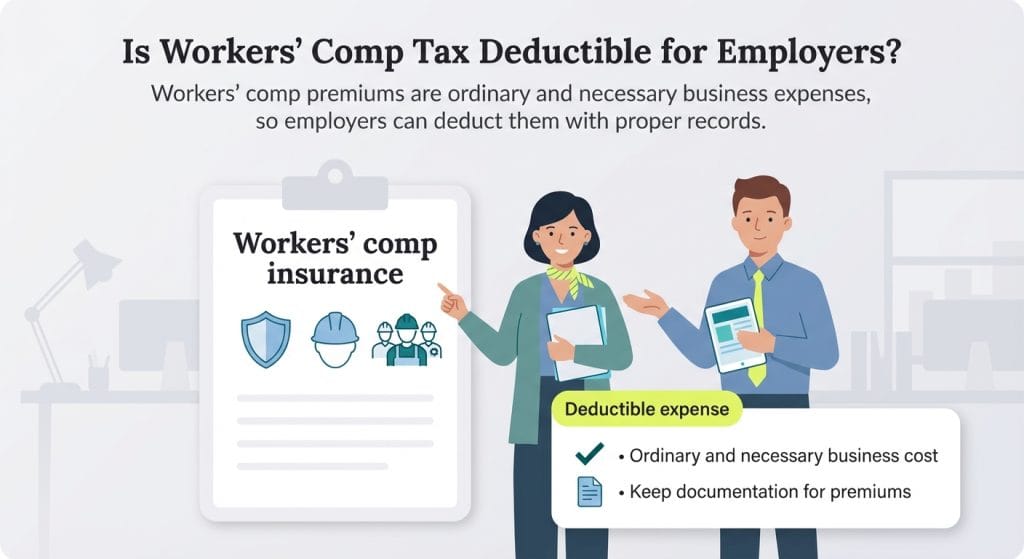

For employers, the premiums paid for workers’ compensation insurance are tax-deductible expenses. In general, when insurance is deemed ordinary and necessary, a business owner can deduct the cost.

The IRS guide on deducting business costs defines an ordinary expense as something “common and accepted in your trade or business.” Because workers’ comp policies are considered ordinary (and often necessary by law), businesses can treat premiums as deductible expenses.

Heerlein emphasized the importance of careful documentation when listing workers’ comp premiums as a tax deduction. “Keep records showing the coverage period, payment amounts, and which employee groups are covered,” Heerlein recommended. “I always advise clients to work closely with both their accountant and insurance broker during tax prep to avoid misclassifying premiums.”

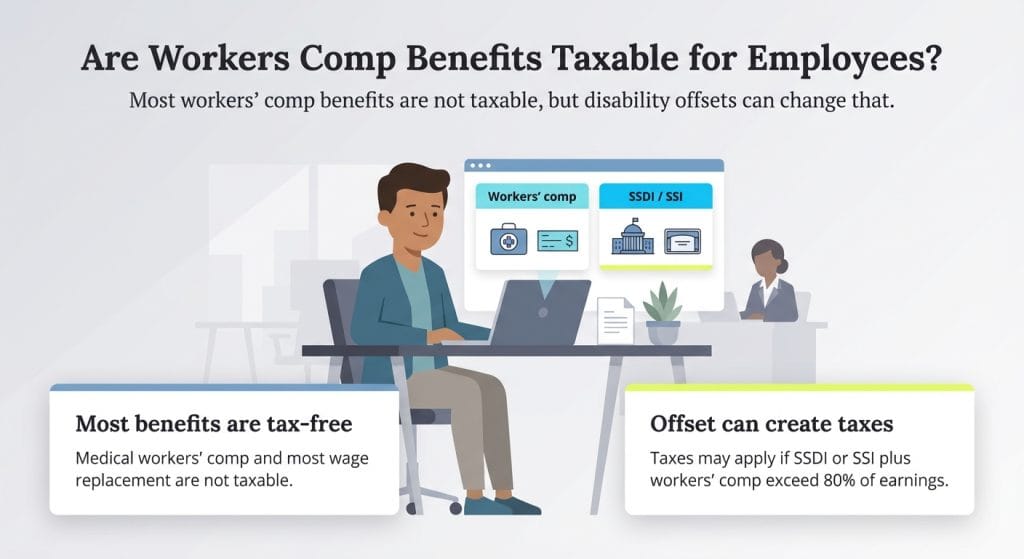

When employees can’t return to work due to job-related injuries, they receive medical benefits and lost-wages benefits through workers’ comp while on disability leave. Medical benefits are paid directly to providers and aren’t taxable.

Lost-wages benefits are usually not taxable either, but there are exceptions. For example, if the employee is also receiving federal Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI), a portion of the workers’ comp lost-wages benefits may become taxable to the extent that total benefits exceed 80 percent of the worker’s average current earnings — this is known as the “workers’ compensation offset.” (More on this below.)

Both SSDI and SSI are federal disability programs offered through the Social Security Administration (SSA). Although both programs provide cash benefits, they have different eligibility requirements. Because neither program covers temporary disabilities, most workers’ compensation cases will not lead an injured worker to file for them.

Both SSDI and SSI define disability in the SSA Code of Federal Regulations as “the inability to do any substantial gainful activity by reason of any medically determinable physical or mental impairment which can be expected to result in death or which has lasted or can be expected to last for a continuous period of not less than 12 months.”

In other words, to be eligible, the injury must prevent the worker from doing their job — or any other job — for at least 12 months.

If you qualify for SSDI or SSI while receiving workers’ comp, part of your workers’ comp benefits may become federally taxable under the “workers’ compensation offset” rule, which applies if your combined benefits exceed 80 percent of your average current earnings. State laws vary, so it’s best to consult a tax consultant about your specific situation.

Natalie Hamingson and Mark Fairlie contributed to this article.