Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

How Do Workers’ Compensation Rates Work?

Workers' compensation rates stem from various factors, including industry risk, claims history and payroll costs. Here's what you need to know about workers' compensation, and how to keep costs down.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Workers’ compensation insurance isn’t just a legal requirement, it’s a necessary business insurance policy that could save you a lot of money if someone gets hurt on the job. Unfortunately, it’s often expensive. Workers’ compensation rates are affected by industry risk, your claims history and payroll costs. When you understand the factors affecting your workers’ compensation rates, though, it can help you keep costs down.

What workers’ compensation covers

Workers’ compensation covers medical expenses and lost wages for employees injured in the workplace. It also covers rehabilitation costs, permanent disability benefits and death benefits for family members of workers who are killed on the job.

Did You Know?

Private industry employers reported 2.6 million non-fatal workplace injuries and illnesses in 2023, according to the U.S. Bureau of Labor Statistics. That represented a decline of 8.4 percent from year-over-year, and the lowest rate since 2003.

How workers’ compensation rates are calculated

Insurance providers commonly use the following equation to determine workers’ compensation rates:

Class Code Rate x Payroll ÷ $100 x Experience Modifier = Premium

Let’s break down each variable in the formula:

Class code rate: The class code rate is a variable that demonstrates a particular job’s risk. The riskier the job in the eyes of an insurance provider, the higher the class code rate. It is generally expressed as a dollar figure per $100 of payroll.

Payroll: This figure is typically the total labor costs of your business divided by 100. The higher your payroll, the higher your perceived risk, which means your annual premium will be higher.

Experience modifier: The experience modifier reflects how your claims history affects your premium and is expressed by a number ranging from 0.75 to 1.25. New businesses start with a 1.0. If your business has filed a lot of claims, your experience modifier will likely be higher than one, increasing your annual premiums. If your track record shows you seldom file claims, your experience modifier will likely be lower than one, reducing your annual premium.

Now that you understand each variable, let’s look at practical examples of how this formula works.

Example 1: Small Office Business

Class Code Rate: $0.50 per $100 of payroll (low-risk office work)

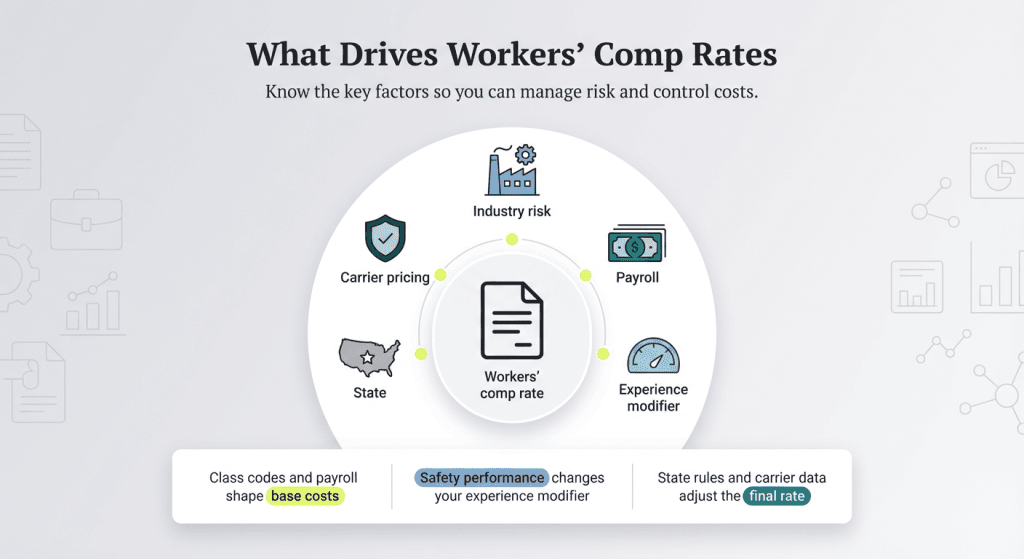

Here’s a closer look at the five primary factors that affect your workers’ comp rates, including the variables in the equation. Examining these factors in more detail will help you understand your rate and how you might be able to mitigate risks to reduce the cost of your annual premium.

1. Industry Work Classification

Every job has risks, but some jobs carry higher risks than others. The class code rate is a variable that demonstrates a particular job’s insurance risk according to its industry work classification.

For example, an electrician working on remote towers is at higher risk than a customer service representative in a call center. Additionally, a roof installer is at greater risk of injury than a call software developer.

The industry work classification reflects a job’s risk factor via a class code rate. Most states use the National Council on Compensation Insurance (NCCI) codes to establish industry work classifications.

3. Payroll

Insurance companies consider your payroll when determining your company’s risk. The more payroll you process, the higher your rate because your loss exposure is greater. In other words, the more payroll you have, the more risk there is to the insurance company.

Insurance companies divide the total payroll by 100 to determine the variable used in the workers’ comp equation shown above. For example, if you have $100,000 in payroll, you would divide that number by 100 to get 1,000.

3. Experience Modifier

An experience modifier, also known as the experience modification rate (EMR), reflects how your claims history affects your premium. The higher the EMR, the higher your premium will be.

All new businesses start with an experience modifier of 1.0 and will see fluctuations based on the ratio of their claims to overall industry claims. These numbers often vary from 0.75 to 1.25. However, it’s possible to see an EMR go much higher if your company has excessive claims.

Rates for various work classes will fluctuate from state to state based on the state’s history and experience with claims and risk classifications. States that see many high-cost claims will generally see higher job class rates among employees. Regulators review rates annually and adjust them based on current data within the state.

5. Insurance Carrier

The insurance carrier’s schedule of rates also affects your workers’ comp rate. When an insurance carrier is familiar with an industry, the rates are usually more competitive because the carrier wants to work with those types of businesses.

Even though many factors affect rates, the insurance carrier ultimately sets workers’ compensation rates. The same carrier will often have different rates in different states for the same type of business.

Carriers will use the NCCI data, state information and their own data to determine rates. This is why rates differ from carrier to carrier, and some are more competitive than others.

Workers’ compensation rates by state

Even though rates vary by industry, every state has an average of workers’ compensation costs per $100 of payroll. This data gives you an idea of what you can expect when shopping for insurance rates. The National Academy of Social Insurance (NASI) maintains an annual report that lists the state averages.

Here’s a glance at the most and least expensive states by rate per $100 of payroll, according to NASI’s most recent data.

Highest Cost States

State

Rate per month

Wyoming

$1.83

Hawaii

$1.62

Montana

$1.48

Idaho

$1.42

South Dakota

$1.41

Lowest Cost States

State

Rates per month

Texas

$0.41

Virginia

$0.56

Indiana

$0.60

Massachusetts

$0.61

Arkansas

$0.63

Utah

$0.63

Official State Workers’ Compensation Resources

For detailed information specific to your state, contact your state workers’ compensation board directly:

Safety compliance and OSHA standards impact on rates

Workplace safety compliance directly affects workers’ compensation rates. Companies with strong safety programs typically experience lower claim frequencies and reduced premiums.

OSHA’s Role in Workers’ Compensation Costs

The Occupational Safety and Health Administration (OSHA) sets and enforces workplace safety standards that significantly impact workers’ compensation costs. Key OSHA standards affecting workers’ comp rates include:

OSHA Recordkeeping Requirements: Employers must maintain accurate records of work-related injuries and illnesses, which directly impact experience modifiers.

Industry-Specific Standards: OSHA has specific standards for construction, manufacturing, maritime, and other high-risk industries.

Tip

According to OSHA's Safety Pays program, which uses data from the National Council on Compensation Insurance (NCCI), effective safety programs can result in reduced workers' compensation premiums, lower experience modification rates, decreased claim frequencies, and improved employee morale and productivity.

Tips for lowering workers’ comp costs

Like many business insurance costs, workers’ comp rates can be lowered with specific strategies and tips. Consider the following best practices to help keep workers’ compensation premiums down:

Implement a comprehensive safety program: Regular safety training and hazard identification can reduce workplace incidents.

Maintain accurate payroll records: Ensure your payroll classifications are correct and up to date.

Review your experience modifier: Work with your insurance carrier to understand how your claims history affects your rates.

Consider a return-to-work program: Getting injured employees back to work quickly can reduce claim costs.

Shop around for carriers: Different insurance companies may offer more competitive rates for your industry.

Implement safety incentives: Reward employees for maintaining safe work practices.

Frequently Asked Questions

Workers' compensation rates are typically reviewed and updated annually by state regulatory agencies. NCCI files rate recommendations on behalf of insurers in participating states, with changes usually taking effect on January 1 of each year.

Yes, if you believe your experience modifier is incorrect, you can request a review through NCCI or your state's workers' compensation board. You have the right to review the data used to calculate your EMR and request corrections for any errors.

Safety improvements typically take three to four years to fully reflect in your experience modifier, as EMR calculations use a three-year experience period with a one-year lag for claims development.

Generally, independent contractors are not covered by workers' compensation, but this varies by state. Some states require coverage for certain types of contractors or in specific industries.

Penalties for not carrying required workers' compensation insurance vary by state but can include fines, criminal charges, and personal liability for employee injuries. Texas is the only state that doesn't require most employers to carry workers' compensation insurance.

Without workers’ compensation insurance, your business may be subject to costly claims, lawsuits, state penalties and fines. Some states even have criminal penalties for companies without workers’ comp insurance. Take the time to understand how you’re being charged and look for ways to reduce the costs of this necessary expense.

Kimberlee Leonard is an insurance expert who guides business owners through the complicated world of business insurance. A former State Farm agency owner herself, Leonard started her decades-long career as a financial consultant advising on investment strategies before switching her focus to insurance and risk mitigation for businesses.

At business.com, Leonard covers topics related to business insurance, such as workers' compensation rates, professional negligence, insurance riders, hold harmless agreements and more.

Leonard has developed insurance primers on everything from small business insurance costs to specific policies, such as excess liability insurance. She has also reviewed business software tools, analyzed employee retirement plan providers and continues to share insights on financial topics as they relate to business. Leonard's work has been published in Forbes, U.S. News and World Report, Fortune, Newsweek and other respected outlets.