Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

The Insurance Claims Process and How to File

If your business suffers a loss that’s covered by insurance, you’ll need to file an insurance claim. Learn how an insurance claim works and how to file one.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

If you’re in an accident or your organization suffers a loss covered under a business insurance policy, filing an insurance claim should be one of your first steps. Filing a claim initiates the process of securing monetary compensation for any losses you incurred. The best commercial insurance providers strive to make the claims process as straightforward as possible. But, knowing how claims work — and how to file one — is essential.

How to File an Insurance Claim

Determine how to file your claim

Gather required information and documentation about the incident

Take quick action to protect your interests

Work with the assigned insurance adjuster

Consider talking to an attorney

What is an insurance claim?

An insurance claim is a request made by an insured party (the policyholder) to their insurance company for a loss covered under the policy agreement.

For example, say you operate a fleet of company vehicles and one of your drivers is involved in an accident. Fortunately, you have commercial auto liability insurance to help compensate you for costs. To start the process of having the insurance company pay for repairs to the vehicle, you will need to file a claim with your insurance carrier. The insurance company may then approve or reject the claim based on an assessment.

How to file an insurance claim

The claims process will vary based on the type of business insurance you’re dealing with (e.g., workers’ compensation, business property, professional liability, commercial auto liability or another coverage type). However, the basic steps will be similar to the following:

1. Determine how to file your claim.

First, determine your insurance provider’s specific preferred claims-filing method. For example, many providers let you file claims online or via an app, but some require you to speak with an agent over the phone. In many cases, your insurance broker can also guide you through the claims process and provide additional support if issues arise.

“For basic claims like a single-party car accident, roadside assistance [or] glass claims, we encourage our clients to directly report their claims to their insurance carrier and then reach out to their broker if they are running into any problems or if they have questions,” explained Katie Blackburn, head of property and casualty claims advocacy at World Insurance Associates. “You will need to know your insurance carrier’s name, [your] policy number and have some specific details about the incident. For all other claims, we would recommend that the client reach out to their insurance broker as soon as they know about a claim.”

The claims process may include downloading and mailing documents. It may also entail uploading documents to an online insurance portal, faxing documents, calling a toll-free hotline or using an app. Knowing how your insurance provider’s process works will make it easier and quicker to file a claim.

Blackburn emphasized the importance of understanding claims-made policies and their unique requirements. Such policies can include directors and officers (D&O) insurance, employment practices liability insurance (EPLI), and errors and omissions (E&O) insurance. Unlike occurrence-based policies, claims-made policies provide coverage only if the claim is filed during the active policy period or during a specified extended reporting period. This is the case regardless of when the incident occurred.

“For claims that may fall under a claims-made policy, such as D&O, EPLI, E&O or other management liability policies, we would recommend that the client reach out to their broker to discuss reporting the claim as a Potential Claim to their insurance carrier,” Blackburn advised. “[This ensures] they are complying with the strict reporting guidelines that claims-made policies carry.”

2. Gather the necessary information and documentation.

Next, you’ll gather the basic information your insurance provider will need, which will likely include the following:

Contact information for you and others involved

Your policy information (if available)

The type of loss (auto, property, general liability or workers’ compensation)

The date of the incident

A description of the loss or any injury

If you took photos immediately following the incident, you’ll submit those to your insurer. You should also provide an inventory of anything that was damaged or ruined.

“Document, document, document,” urged John McCormick, insurance editorial director at QuinStreet. “Make detailed notes of what happened, when and any relevant incident details. Take clear photos and videos of the damage from all angles. Keep receipts and invoices of your damaged property and any repairs you make. Collect serial numbers and receipts. If these can be salvaged, they will help with your claims.”

FYI

Check your insurance policy's declaration page for details on coverage and deductible amounts. These are key factors to consider when choosing business insurance to ensure it meets your needs.

3. Take quick action to protect your interests.

At this point, you’ve determined your carrier’s specific filing procedures, so follow through promptly. “File a claim as soon as possible,” McCormick advised. “Provide all the details and documents you’ve collected, and follow your insurer’s instructions closely.”

Immediate action is especially important in cases of building-related damage. Your insurer will likely require you to take steps to prevent further damage — even while the claim is being filed or processed. Document all observations related to the incident; this material includes permits and licenses, names and addresses of involved parties, and photographs of the damage.

4. Prepare for the adjuster.

You’ll be assigned an insurance adjuster within a few days of filing an insurance claim. The adjuster is responsible for evaluating the damage and determining what the insurance company is responsible for covering. You may be required to provide proof of loss within 60 days of the initial insurance claim.

“The carrier will intake the claim, set up a claim file and assign an adjuster,” Blackburn explained. “The client should receive a claim acknowledgment from the carrier with this information within 24 to 48 hours, if not sooner. The adjuster will then reach out to the client. They will usually need any supporting documentation that’s available, and they will likely have follow-up questions for the insured. Depending on the carrier and the claim, an independent adjuster may be sent out to inspect the property.”

5. Consider talking to an attorney.

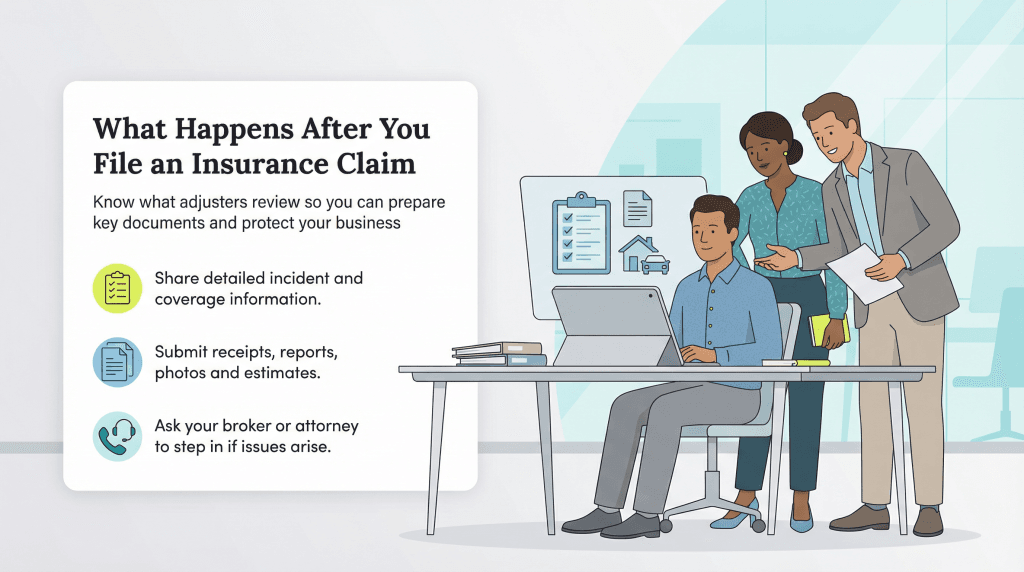

Is your case complex and do you need additional assistance? Then consider working with an insurance attorney to help gather the necessary documentation. Also, you should ensure you provide everything the insurance company has requested. This legal professional can also help you if you run into a dispute with your insurer. [Read related article: A Crash Course in the Business Legal Terms You Need to Know]

“Think about hiring outside experts,” McCormick recommended. “The U.S. Small Business Administration suggests calling in a legal expert to help you with your insurance documentation and/or a professional contractor to help you estimate your repair and replacement costs.”

Blackburn noted that the decision to hire an attorney depends largely on the unique needs and complexities of the business. “It depends on what kind of business and how large, complex, and regulated that business is,” Blackburn explained. “All businesses should have an attorney they can speak with who is experienced in the kind of work that business does and the jurisdictions that they do business in.”

After filing an insurance claim, a claims adjuster will gather information about the incident and your policy’s coverage to determine how much the insurance company should pay. Their goal is to settle your claim as quickly and cost-efficiently as possible.

Be prepared to provide the adjuster with all incident details and any applicable repair, service or replacement estimates. Relevant documentation includes:

Receipts

Accident reports

Injury information (in workers’ compensation cases)

Police reports

Photographs of the damage or incident (to substantiate the loss)

Medical records and bills

Estimates from contractors

Auto repair estimates

Invoices

In certain instances, the insurance company may suggest a lawyer and may cover the cost of the attorney as well as any settlement or judgment. “If the business owner is being sued, defense counsel should be appointed,” Blackburn explained.

In some cases, you may feel your claim isn’t being handled appropriately. “If the adjuster is not being responsive, if they don’t seem to understand the insured’s business or don’t have enough experience to handle a complex claim, then I would recommend that the client reach out to their broker to advocate on their behalf with the carrier,” Blackburn advised.

How are claims paid?

After the adjuster receives and investigates the claim’s validity and determines the amount of coverage according to your policy, they may request additional information.

Once that review is complete, the claim will be either approved or denied. Any payment you receive for a loss will be subject to the policy’s limits and deductible — the out-of-pocket amount for which you’re responsible.

Blackburn explained that payment specifics depend on the claim type. For example:

Liability claims: Liability claims are typically paid after a settlement or verdict is reached and approved by the courts.

Property claims: Property claims require carriers to review applicable quotes or invoices incurred due to the damage; they must approve the scope of work and labor and material costs. For large property claims, the insured may receive an advance payment followed by additional payments as more work is done.

“For a smaller claim, the payment would likely be made once the quotes for work are agreed upon, and then any supplemental payments, or recovery for depreciation, would be issued once the work is complete,” Blackburn noted. “Payments are typically made via check, ACH or wire depending on the size of the payment, who the insurer is and the type of claim.”

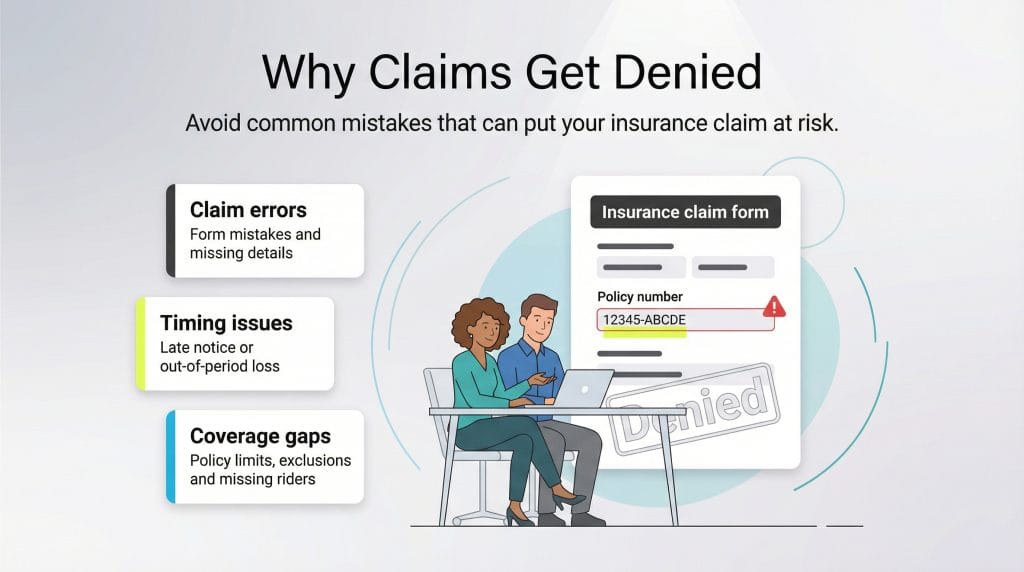

Why would a claim be denied?

Your claim could be denied for several reasons, including the following:

Errors in the claim form: Your claim form contained an error, such as incorrect or insufficient information (e.g., a typo in the policy number).

Timing issues: The incident or loss occurred outside the policy’s effective period (i.e., before the policy’s start date or after its expiration). Timely notice of a loss is also required for many business insurance policies; delays in reporting can lead to a denied claim. Notify your insurer immediately following the incident or loss to avoid this issue.

Policy exclusions or limitations: The incident or loss occurred outside the scope of the policy. For example:

A general liability policy will not cover loss or damage to your own property (it only covers third-party property).

An auto accident that happened while you were driving for personal reasons would fall outside the scope of a business auto policy.

FYI

Obtaining an insurance rider (also called an insurance endorsement) can simplify the claims process. It reduces the likelihood of denials due to coverage gaps — making them particularly valuable for high-risk businesses or industries.

What are the costliest insurance claims?

These are the most expensive insurance claims for small businesses on average (broken down by average claim cost):

Reputational harm

$50,000

Vehicle accidents

$45,000

Fire

$35,000

Product liability

$35,000

Customer injury or damage

$30,000

Wind and hail damage

$26,000

Customer slip and fall

$20,000

Water and freezing damage

$17,000

Struck by object

$10,000

Theft and burglary

$8,000

Natural disasters are among the most expensive insurance claims. Of course, it depends on the nature and severity of the disaster. For example, Hurricane Katrina resulted in over 1.7 million claims totaling $41.1 billion. If divided equally, which is unlikely, that would average approximately $24,176 per claim.

“Claims can be expensive for a variety of reasons,” Blackburn explained. “It depends on the kind of claim, the extent and kind of damages, the jurisdiction that the claimant is in, the severity of the loss, cost of medical treatment, cost of ongoing care for an injured party, legal fees, type of defense counsel that needs to be retained and jurisdiction that counsel is practicing in, cost of materials and labor, and if there are any supply chain disruptions.”

Is it worth making an insurance claim?

Based on the numbers revealed above, is it worth filing an insurance claim? Often, yes, but not always. It depends on these factors:

The incident

Your claims history

Whether you are the at-fault party

Your policy coverage

The amount of the loss

Claims history

Your claims history can significantly affect your business insurance costs. If you have a history of filing claims, adding another claim may increase your risk profile and, as a result, your insurance premiums. Insurers maintain databases of claims records to assess business insurance risk. Filing a claim near your deductible amount could also appear on your report without yielding much financial benefit.

If you have concerns about your insurability due to a history of accidents or losses, consult your insurance company. If your provider drops you as a policyholder, a new insurance carrier may adjust your premiums to reflect the higher risk. Even if you remain with your current insurer, you risk increasing your premiums.

Tip

To save money on business insurance, shop your coverage with several providers. You should also bundle your coverage with a business owner's policy and inquire about a claims-free discount.

At-fault party

If you are determined not to be at fault for the incident, a third party may pay. For example, let’s say you were involved in an auto accident that was not your fault but resulted in damage to your business vehicle. The at-fault driver’s insurer might pay the repair costs via the subrogation process. If you sign a waiver of subrogation, it waives future legal action and claims on the incident.

To protect your interests, report accidents immediately to your insurer and notify them if you agree to any settlements. Consult an attorney before signing subrogation waivers — especially if you live in a no-fault auto accident state — to fully understand your rights and potential outcomes.

“If there is an at-fault party, we would recommend that our client file a claim with that at-fault party’s carrier,” Blackburn said. “Sometimes, a client may want to file the claim under their own insurance and then have their carrier subrogate against the at-fault carrier’s carrier down the road. If a claim is under the client’s deductible, we would recommend not to file it.”

Policy details

Consider the details of your policy, especially in the case of general liability. Many policies prohibit the insured from making a payment without consent, and some don’t allow direct payments to third parties.

This could ultimately cause a notice of policy cancellation or nonrenewal for the violation. There is also the risk that your case will be sent to litigation. So, you should not take these actions without speaking to your insurance representative or attorney.

Cost of the loss

You may want to eschew filing a claim if the loss:

Is less than your deductible

Doesn’t affect another party

Carries no risk of legal action, further damage or associated medical costs

Can be paid out of pocket

If you choose not to file a claim, you may be able to deduct the loss on your tax returns. The appropriate method depends on your business’s legal structure. Consult a tax accountant to ensure compliance and carefully weigh your options before proceeding.

Making informed decisions for a smooth insurance claims process

Understanding the insurance claims process is essential for ensuring a smooth recovery from accidents or losses covered under your business insurance policies. Filing a claim promptly, providing accurate documentation and staying informed about your policy’s coverage can significantly impact the outcome.

It may not always be cost-effective to file a claim. But, carefully evaluating the incident, your claims history and potential financial implications can help you make the best decision for your business. Being proactive and informed can help protect your business’s financial health and maintain a favorable relationship with your insurer.

Nicole Urbanowicz is a small business owner who studied management and finance at Harvard, where she received her master's degree. Before becoming an entrepreneur herself, she started her career writing about business and investing for Dow Jones and The Wall Street Journal, after which she became a research analyst for Allured Business Media, using business intelligence data to develop strategic guidance.

At business.com, Urbanowicz covers a range of insurance topics, including workers' compensation, endorsements, coinsurance and more.

Today, in addition to running her e-commerce business, Urbanowicz continues to provide financial analysis and advice and uses her certification from the New York State Department of Financial Services to consult on insurance matters.