Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

EPLI protects your business from lawsuits brought by past or current employees. Learn how EPLI works and why your business needs it.

With employee lawsuits on the rise, small businesses should consider purchasing employment practices liability insurance (EPLI). EPLI protects your company if current, past or prospective employees sue for alleged wrongful treatment. This type of liability insurance is increasingly important, especially since employee litigation claims cost companies in the U.S. over $40 million in 2024 alone. Industry analysts expect these types of losses to continue to impact businesses across various industries in the coming years.

Learn more about EPLI, whether it’s the right fit for your company, and how shopping for EPLI compares to choosing business insurance for other types of policies.

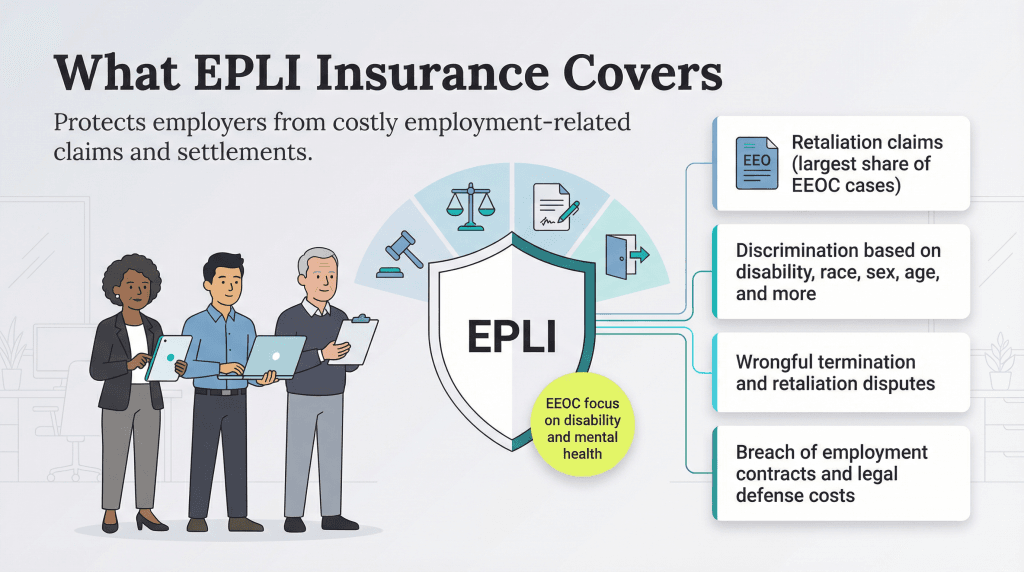

EPLI is a business insurance policy that protects organizations from employee mistreatment claims. It provides coverage for various lawsuits, including sexual harassment, discrimination and mismanagement of employee benefits. If an employee files a lawsuit against your company, EPLI may help pay for legal costs and damages, regardless of the suit’s outcome.

Some businesses choose to opt out of EPLI coverage. However, according to Corrie Hurm, head of claims at Embroker, that’s a big mistake.

“Many business leaders believe their general liability policy covers these risks or feel confident in their HR practices,” Hurm explained. “However, this is a dangerous oversight, as from the moment a business hires its first employee, it becomes exposed to potential employment-related claims. This exposure exists regardless of the company’s size, industry or the quality of its HR operations.”

No one wants to believe a current or former employee would sue them, but these kinds of business lawsuits are on the rise. Unprotected organizations can face devastating financial repercussions.

“What is particularly troubling is that many organizations don’t recognize the need for EPLI until they are already facing a claim,” Hurm noted. “At that point, it’s too late to secure coverage for that incident, and if they were to try, the cost would likely be much higher.”

At the very least, a lawsuit can hurt your brand’s reputation and ability to make money in the future — and it can happen to anyone. Even businesses with the best intentions and solid HR practices can be caught off guard, according to Hayden Cohn, CEO of Hire with Near.

“The simple fact is that even if businesses take the time to carefully review employment law and invest in proper training and procedures to avoid legal issues, accidents can happen,” Cohn cautioned. “It only takes one irresponsible manager, one disgruntled employee, or one unforeseen situation to expose the company to liability, and investing in EPLI should be one of the ways businesses protect themselves.”

EPLI policies typically cover the following claims against employers:

According to the Equal Employment Opportunity Commission (EEOC)’s 2024 enforcement and litigation statistics (the most recent data available), retaliation remains the most frequently cited claim in charges filed with the agency. It accounts for more than 47.8 percent of all charges filed, followed by claims of discrimination based on disability, race and sex.

The following claims categories are noted in descending order of frequency:*

*These percentages add up to more than 100 percent because some charges allege multiple bases.

The EEOC said it recovered $700 million for workers claiming discrimination in 2024, including over $40 million in litigation claim awards. This was the largest recovery in the agency’s recent history.

Disability claims, in particular, have increased in recent years as workplace cultures shift toward greater openness around mental health-related disabilities.

“More employees are now comfortable disclosing mental health concerns to their employers, recognizing these issues as disabilities that may require accommodations,” Hurm explained. “However, these situations can become contentious if an employee requests accommodation and then faces adverse actions, such as termination.”

Hurm noted that the EEOC has made disability discrimination, especially related to mental health claims, a significant focus in recent years. “They have launched initiatives aimed at addressing this issue,” Hurm said. “However, the approach may shift depending on the current administration, which could alter the priorities of the EEOC moving forward.”

There are many common exclusions to EPLI. Although these vary from state to state, coverage typically excludes these areas:

The cost of your EPLI policy will be determined by various factors, including your industry, your business location and whether you’ve had similar claims filed in the past. On average, a standard $1 million EPLI policy costs between $1,500 and over $2,500 per year for five to 20 employees.

Underwriters typically examine the following risk assessment factors to determine the price of the policy:

Another determining factor in the cost of EPLI is the amount of coverage your business needs. Most EPLI policy limits range from $500,000 to $1 million, although businesses that pay higher salaries may opt for as much as $2 million in coverage. Also note that many EPLI policies have a deductible, which means you can lower the cost if you raise the deductible. You may want to consult an attorney to ensure you have adequate coverage.

Employee lawsuits are rising, and many business owners are unsure how to curb this trend. These lawsuits are costly and can hurt morale and productivity, especially if a current employee files the suit.

One reason for the rise in employee lawsuits is that people are more aware of their legal rights in the workplace. Legal protections and anti-discrimination laws have expanded to provide employees with more safeguards, and the EEOC is enforcing compliance more strictly than ever.

The bottom line is that small business owners must take steps to protect their companies from the threat of lawsuits. EPLI coverage can protect your business if the worst occurs.

Natalie Hamingson contributed to this article.