Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Malpractice insurance is a critical policy that all those working in the medical industry should have.

Professionals are expected to perform their services properly and with sufficient expertise. Clients and patients assume someone with a professional designation has the knowledge and resources to do the job right. Sometimes, however, a professional, such as a doctor or lawyer, makes an egregious mistake that causes significant harm to a patient or client. That is called malpractice.

When a professional commits malpractice, the patient or client may sue to recover financial compensation to ameliorate some of the harm that has been done. It’s then up to a court to decide if a mistake was made, if it rises to the level of malpractice and, if so, what the penalty should be. Malpractice awards are often hundreds of thousands of dollars, and they can even climb into the millions. Because the stakes are high, malpractice insurance is a necessity.

Malpractice insurance is a liability insurance policy for healthcare or legal professionals. When errors happen while executing professional services and the professional is deemed at fault, malpractice insurance pays the penalty so the professional doesn’t have to pay for claims out of their pocket.

Malpractice insurance is for legal and healthcare professionals.

Malpractice insurance for legal professionals

In the legal profession, malpractice insurance covers mistakes an attorney might have made in handling a client’s case. Typically, only attorneys are covered by malpractice insurance. Law firms, however, may have an umbrella insurance policy that covers all its employees, including paralegals and administrative staff.

Solo lawyers, however, need their own malpractice insurance policies. “When it comes to legal malpractice insurance, many people don’t realize just how vulnerable attorneys can be to claims of negligence, errors or ethical breaches,” said Stephen Wagner, managing partner and co-founder at Wagner Reese LLP. “For instance, a malpractice lawsuit could spawn if a lawyer misses a critical filing deadline, such as a statute of limitations, causing a client to lose out on their right to pursue financial compensation for their case. Other malpractice issues arise when an attorney provides incorrect legal advice that results in a client suffering financial harm, if the attorney fails to respond to court deadlines which harms a client’s case or if the attorney fails to keep the client advised of the status of a matter.”

Malpractice insurance for healthcare professionals

In healthcare, doctors, surgeons, nurses, physical therapists and specialists can obtain malpractice insurance. Medical malpractice insurance pays claims when patients assert that a healthcare professional hurt them in some way due to negligence or harmful treatment. An example of medical malpractice is if a surgeon operated on a patient while drunk and caused severe harm.

“If a medical practice is hit with a malpractice claim and they have insurance, the first step is to notify their insurer,” Wagner said. “The insurance company will typically assign an attorney to handle the defense, cover legal fees and, if necessary, negotiate a settlement. If the case goes to trial, the insurer will provide legal representation and pay damages up to the policy limits.”

When a medical practice doesn’t have malpractice coverage, the financial implications can be catastrophic. “Without malpractice insurance, however, the situation becomes far more dire,” Wagner said. “The practice has to pay for its own defense, which can quickly add up to hundreds of thousands of dollars. If they lose the case, they must also pay any settlements or judgments out of pocket. For smaller practices, that financial burden can be enough to force them out of business.”

Malpractice policies are specific to the industry they cover and have crucial exclusions and terms. It’s critical to read policy documents carefully before buying a policy.

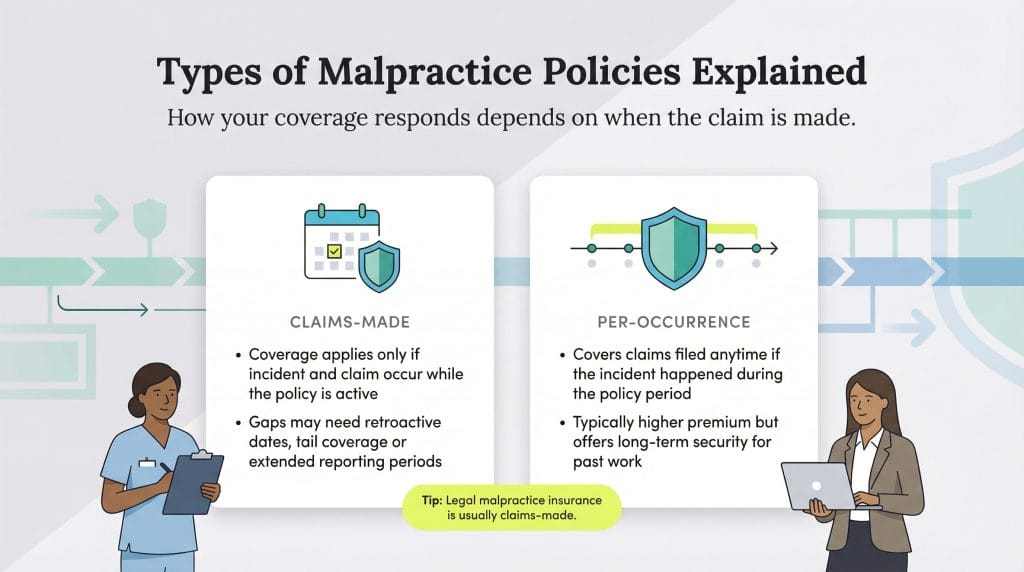

There are two types of malpractice policies. Both cover the same things when your business gets sued; the difference is how that coverage is applied in relation to when the claim is made.

Claims-made coverage requires the policy to be active when the claim is made. A healthcare provider or attorney who had a lapse in coverage could still add a retroactive date of coverage.

“A claims-made malpractice policy covers claims only if both the alleged incident and the claim occur while the policy is active,” said Loren Schwartz, a partner at Rouda Feder Tietjen and McGuinn. “If coverage lapses, past incidents won’t be covered unless the attorney purchases ‘tail coverage.’”

Suppose a doctor accidentally had a policy lapse and didn’t have coverage from Oct. 1 through Dec. 31. In that case, they could get a policy starting Jan. 1 with a retroactive coverage date beginning Oct. 1. That would provide the needed coverage for the period when they were uninsured. Retroactive dates require an added premium, but ensuring coverage is in place is often worth it.

A claims-made policy may also have an extended reporting period, such as six months after the policy’s lapse date. The extended reporting period would cover claims made during the policy’s effective period but reported after the policy lapses.

A per-occurrence policy is more expensive because it allows claims to be made anytime, whether or not the policy is active at the time of the claim, as long as the date that the claim-related activity occurred was during the coverage period.

If a policy has coverage from Jan. 1, 2025, to Dec. 31, 2025, for example, a claim could be made on April 1, 2027, as long as the incident regarding the claim happened in 2025 during the coverage period.

Patients or clients sometimes do not make claims immediately after an incident because they are unaware of the problem. They may only be informed of an error in practice in a follow-up with another provider, thus creating a malpractice claim. As a result, Schwartz said, it can be worth the extra expense upfront for more extensive coverage. “In legal and medical fields, claims-made policies are more common, but per-occurrence coverage offers long-term security, making it more desirable for professionals wanting broader protection,” he said.

Malpractice insurance covers the mistakes a medical or legal professional may make during regular business operations. Medical claims may have to do with misdiagnosis, surgical errors, medication errors, childbirth-related injuries and other mistakes made by medical professionals. Some Health Insurance Portability and Accountability Act (HIPAA) violations are also covered.

For lawyers, malpractice insurance usually covers mistakes made while representing a client in a case. Policies may have different definitions of “legal services,” so it is important to read the policy documents carefully to understand your coverage. One policy may include only legal services a client paid for, for example, while another policy may also cover pro bono services.

What malpractice insurance covers | What malpractice insurance doesn’t cover |

|---|---|

Defense, expert witness, legal, arbitration and settlement costs | Intentional wrongdoing |

Punitive and medical damages | Illegal acts |

Malpractice insurance won’t cover claims arising from sexual misconduct or physical abuse. If the claims are determined to be unfounded, however, the insurance will pay for the defense of the claim.

Since medical or legal mistakes often lead to settlements in the hundreds of thousands ― if not millions ― of dollars, malpractice insurance tends to be expensive. Malpractice costs vary widely depending on the profession and the type of practice involved. Schwartz said specialties such as neurosurgery, obstetrics and gynecology, orthopedic, and cardiothoracic surgery tend to come with the highest premium price tag.

“Medical disciplines with the highest malpractice insurance premiums tend to be those with high-risk, high-stakes procedures,” he said. “These fields have higher claim rates and larger settlement amounts due to the potential for life-altering outcomes. On the other hand, lower-risk specialties, such as psychiatry, pathology and family medicine, typically see lower premiums since they involve fewer invasive procedures and lower malpractice claim frequencies.”

Across medical specialties, annual malpractice insurance premiums average between $4,000 and $12,000, but that varies widely from state to state and across specialties. The range of costs reflects the risk each profession represents. Nurses, for example, are less likely to be sued than the doctor who oversees the nurse. Thus, there is less risk. Nurses could still be named in a lawsuit, however, and they aren’t covered by a doctor’s malpractice policy.

Here are a few examples of medical malpractice premiums:

Costs for attorneys vary depending on the type of law they practice and whether they’ve had previous claims. On average, legal malpractice insurance costs between $1,200 and $3,500 per year. Attorneys in riskier practice areas pay between $3,000 and $10,000 per year. Risky practice areas include securities, intellectual property, personal injury, and trusts and estates.

Paralegals may also carry malpractice insurance, although they are less likely to be sued than attorneys.

Basic malpractice insurance may not be enough. Remember that claims could result in settlements of millions of dollars. How does a professional determine the right amount of insurance to get? [Read related: Best Business Insurance]

First, understand that policies come in various coverage amounts.

To ensure adequate coverage, research the prevailing limits in your area for your profession or specialty. You should have those limits at a minimum. Some professionals will buy even more coverage, but remember that if you have more coverage than anyone else, you become a deep-pocketed target in a lawsuit that names multiple defendants. Some states also cap awards, so you may not need to extend coverage beyond the award limits.

Still, it can be extremely beneficial to invest in supplemental malpractice coverage, depending on the nature of your practice’s work. Schwartz noted that add-ons, such as cyber liability protection, defense cost and reputation management coverage can serve as vital safeguards for your practice. “These enhanced policies provide a layer of financial and professional security that can mean the difference between a temporary setback and permanent damage to a practice,” Schwartz said.

Both legal and medical professionals can benefit from investing beyond the most basic malpractice policy, Wagner advised. “Having higher coverage limits in an umbrella policy can be vital in cases where settlements or jury awards exceed minimum policy limits,” he said. “Many policies also include defense cost coverage, which helps pay for legal representation.”

You can purchase individual or group policies from a private insurance carrier. For medical professionals, medical risk retention groups can also provide coverage at a discounted rate to those in the group.

Some employers have a policy that covers an entire entity, such as a hospital or law firm. That type of policy may cover some individual risk, but check with human resources to ensure that you have the coverage you need. Most doctors and specialists will have their own policies to protect their interests as a separate entity from the hospital or medical group they work with. Some lawyers may also have an individual policy covering legal work outside the firm.

When shopping for insurance, compare prices among various providers to ensure that you get the best coverage for the best price. Remember to compare policies apples to apples for each quote you get, and ensure that each one has the same coverage limits. See if a deductible applies and, if so, how much it is.

A patient or client can file an insurance claim anytime. Sometimes claims are made out of frustration and vindictiveness. Some are outright fraudulent. To get a settlement or a judgment from the professional or their insurance carrier, the plaintiff must prove malpractice occurred.

Natalie Hamingson contributed to the reporting and writing in this article.