Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Is Commercial Umbrella Insurance?

Learn what umbrella insurance covers and how to decide if you need it.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Most businesses carry different types of liability insurance. In particular, businesses typically need general liability insurance and workers’ compensation policies. When you have multiple policies and feel your business is at greater risk of a lawsuit, purchasing a commercial umbrella insurance policy can provide additional coverage for less money. An umbrella policy covers several underlying liability policies to ensure you have the protection you need.

Here’s a deeper look at commercial umbrella insurance, what it covers and how to decide if you need it.

What is commercial umbrella insurance?

Commercial umbrella insurance is an insurance policy designed to extend the liability limits of specific underlying policies. “With the increased size of jury verdicts and litigation financing, commercial umbrella insurance has gained significant popularity among businesses, especially those looking to protect themselves from large-scale liability claims,” explained Chris Peterie of Tower Street Insurance.

For example, if a general liability policy had a $1 million per-occurrence limit and the umbrella policy had a $5 million limit, the business would have a total of $6 million in liability coverage.

Dennis Shirshikov, an adjunct professor of economics at City University of New York, provided a real-life use case: “A retail chain with several delivery vans [could] use business umbrella coverage as a safety net against catastrophic auto-related claims.”

Did You Know?

A commercial umbrella insurance policy doesn't cover professional liability insurance claims, even if you have a professional liability insurance policy. To increase coverage in this area, you'd need to raise the coverage limits on the professional liability policy itself.

What does commercial umbrella insurance cover (and not cover)?

Commercial umbrella insurance adds a layer of additional liability coverage for specific policies a business owner may already have. It covers more than a claim’s settlement; it also pays for investigation and defense costs if the claim results in a lawsuit. Depending on the insurance carrier, some aggregate limits may exclude the cost of investigation and defense.

This aspect of commercial umbrella insurance is a significant plus for a business because lawsuits can quickly run into tens of thousands — if not hundreds of thousands — of dollars and would eat into the capped coverage.

“Commercial umbrella insurance typically applies on a per-occurrence and aggregate basis,” Peterie explained. In other words, the policy can cover multiple claims in a year up to the total or aggregate value.

Notably, your commercial umbrella insurance policy will not add coverage to your professional liability policy. This means that malpractice and errors and omissions policies cannot benefit from an added layer of liability coverage.

Let’s say a company has the following insurance coverage:

General liability policy: $500,000 per occurrence and $1 million aggregate limit

Commercial auto insurance: $250,000 per person and $500,000 per accident limits

Commercial umbrella policy: $10 million limit

Now, imagine the company experiences a challenging claims year:

Slip-and-fall injury: A customer slips on the floor, falls and hits their neck on a display, resulting in paralysis. This leads to a $5 million liability claim.

The general liability policy pays $500,000 (its per-occurrence limit).

The umbrella policy covers the remaining $4.5 million.

After this claim, the umbrella policy’s aggregate limit is reduced to $5.5 million.

Commercial auto accident: Later that year, the company is involved in an auto accident that results in a liability claim of $300,000.

The commercial auto insurance pays the first $250,000 (its per-person limit).

The umbrella policy covers the remaining $50,000.

This example illustrates how an umbrella policy provides additional coverage beyond the limits of the underlying policies, protecting the business from catastrophic financial loss.

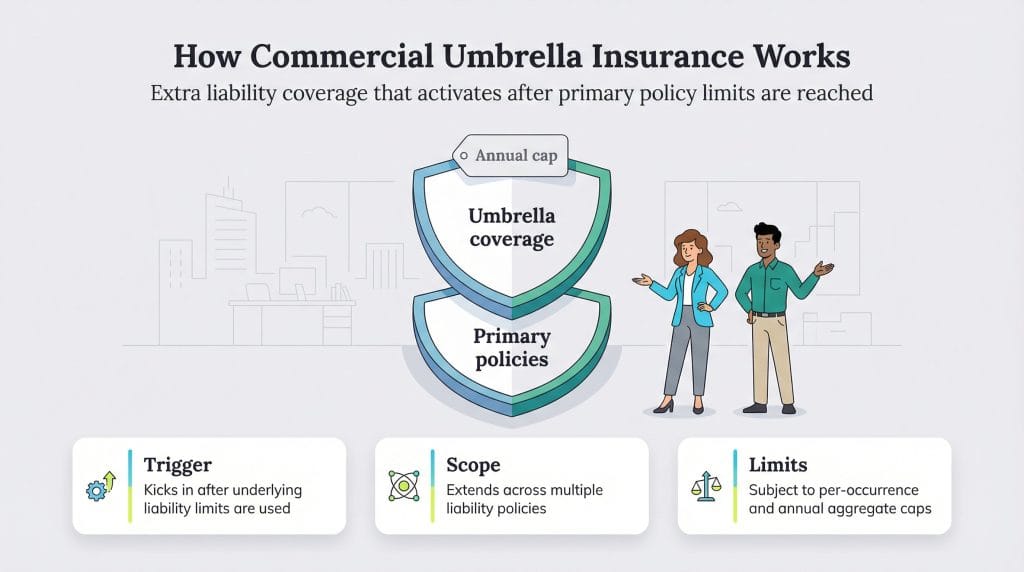

How does commercial umbrella insurance work?

Umbrella coverage is additional coverage for liability policies. The underlying policy’s limit will be utilized first. The umbrella policy will kick in once the underlying policy reaches its maximum limit or cap. The umbrella coverage is used until it hits its cap.

When it comes to umbrella insurance, both the per-occurrence limit and the annual aggregate limit apply. A company can have several claims, but the annual aggregate limit caps the total amount the insurance company will pay for all claims in a year.

Don’t confuse umbrella insurance with excess liability insurance. Both add coverage, but excess liability insurance applies to only one policy, usually general liability while umbrella insurance covers multiple policies. “Excess liability might be used to increase solely general liability coverage, while an umbrella could augment car and other liability lines,” Shirshikov explained.

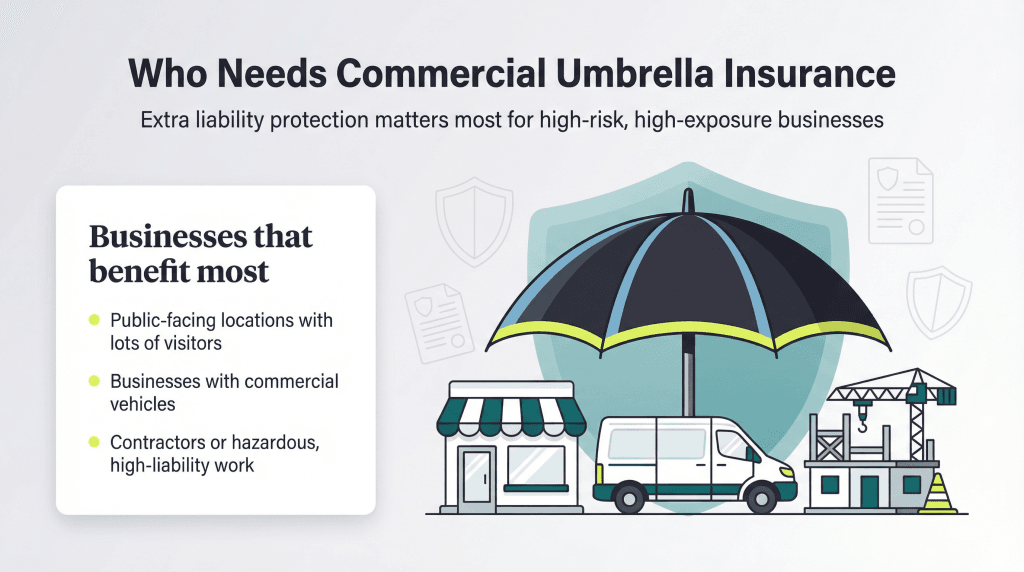

Who needs commercial umbrella insurance?

A business with significant liability risks and multiple types of business insurance policies should consider a commercial umbrella policy. Adding umbrella insurance is generally a more cost-effective way of adding overall liability coverage, as opposed to increasing each liability policy’s limits. It can reduce the price of higher coverage insurance, such as high-liability commercial auto insurance costs.

Liability claims can be unpredictable and costly, so all business owners should evaluate the potential benefits of umbrella insurance against the policy’s costs to determine its value.

Some businesses, such as construction contractors, may be asked for proof of insurance with specific limits when working with certain clients or on government contracts. In cases like this, the contractor would get an umbrella policy to extend coverage to its other policies without requiring direct modifications to their limits.

In general, the following parties need commercial umbrella insurance the most:

Businesses with significant public exposure, such as restaurants, retail stores and event venues

Businesses with commercial vehicle fleets

Contractors working on government or high-liability projects

Businesses in hazardous industries, such as construction or manufacturing

Did You Know?

Contractors' insurance needs are unique, with both mandatory and advisable policies to help cover the costs of repairs and replacements and deal with business lawsuits.

How much does commercial umbrella insurance cost?

The cost of your commercial umbrella liability insurance policy depends on the amount of coverage you need, your claims history and your business’s specific insurance risk profile. You can get a policy for as little as $30 per month for up to $1 million in additional umbrella coverage.

In most instances, getting an umbrella policy will be less expensive than adding additional liability coverage to your underlying policies. Ask your insurance representative to run a quote both ways to see what’s most cost-effective while getting your liability coverage set up.

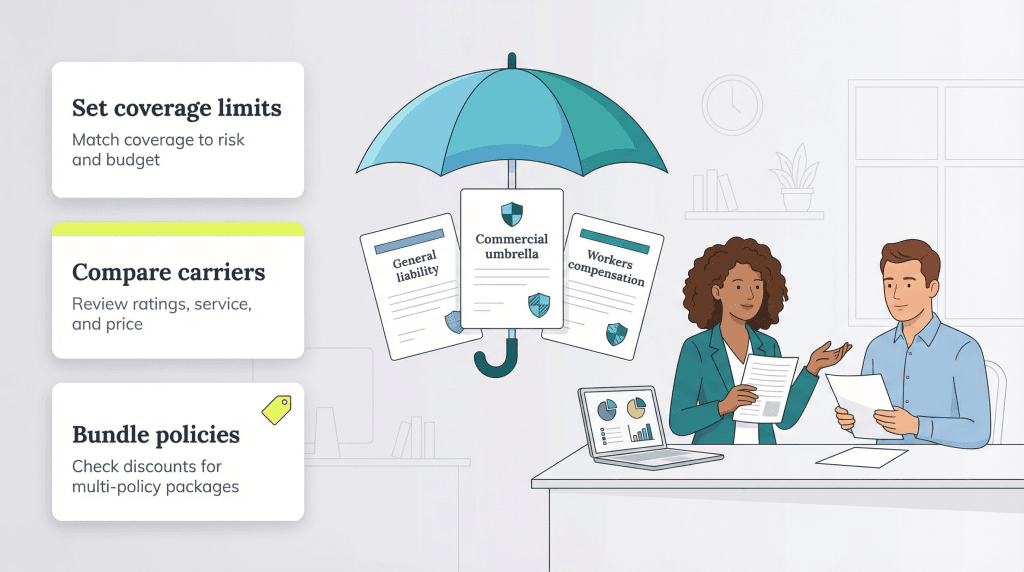

Your desired coverage level will depend on your company’s net worth, risk profile and budget. Once you decide the coverage level you need, start getting quotes from multiple insurance carriers to compare them.

2. Contact your current insurance carrier.

When shopping for commercial umbrella insurance, remember that you don’t have to purchase this policy from the carrier you used for other policies. However, your current insurance carrier may offer discounts or policy credits to existing customers. Getting a quote from your current carrier can give you a benchmark against which to evaluate quotes from other companies.

3. If you have an independent insurance broker, reach out.

If you already have a working relationship with an independent insurance broker, reaching out to them may provide faster service than seeking out a new broker. If you don’t currently work with an independent insurance broker (one who partners with multiple insurance carriers), find one and ask for at least three quotes. Independent agents can give you insight into which carriers have a better reputation for speedy claims processing and satisfactory claims resolution.

4. Consider consolidating insurance policies with one carrier.

It’s ideal to shop for umbrella insurance, general liability insurance and workers’ compensation insurance at the same time with new carriers to see what type of package deal you can get. If you are unhappy with one or more of your current carriers, this is a good opportunity to make a move. Conversely, if one of your carriers has given you particularly good service, you should explore moving other policies to that carrier.

In addition to the quote for commercial umbrella insurance, get a quote for all your insurance policies. Be sure to do this with every company you’re considering. Some might have a higher price on umbrella coverage but offer a much bigger discount if you bundle your policies.

5. Evaluate your quotes on price, rating and coverage.

When comparing quotes, price will be a crucial factor. However, you should also evaluate and compare the proposed coverages in detail. Some companies might exclude something you want or give you lower coverage amounts. For example, Farmers Insurance offers umbrella coverage of up to $10 million, while American Family goes up to only $2 million.

Five agencies rate insurance companies on their financial strength:

A.M. Best Company

Fitch Ratings

Kroll Bond Rating Agency

Moody’s Investor Services

Standard & Poor’s Insurance Ratings Services

Research the insurance carriers on your shortlist on multiple rating agencies to get an accurate picture of their financial strength. More stable insurance companies — those with higher ratings — typically cost more but are less at risk of going out of business and leaving you high and dry in the event of a claim.

Tip

Don't just get a quote for umbrella insurance. See how much you can save in insurance costs if you bundle policies with one carrier. Many of the best liability insurance providers offer discounts or credits for bundled policies.

Commercial umbrella insurance FAQs

Commercial umbrella insurance isn't required, and you'll never be asked to prove you have an umbrella policy. However, if you don't have a policy, you could be underinsured in a serious claim. Someone could make a claim that exceeds your policy limits, and you'd have no additional coverage or protection. Your business could then be liable for the difference between what your policy covers and the claim amount. Choosing not to get an umbrella insurance policy could expose your business to high-value claims. This could be financially devastating to small businesses.

Insurance will cover you only up to the policy's aggregate limits. If you exceed these limits, you're responsible for the value in excess of the insurance cap. For example, if the aggregate limit is $5 million and you have a claim for $6 million, you would be responsible for the extra $1 million. This is why increasing coverage where you can afford it is essential. You are not absolved of responsibility just because you have an insurance policy. Claimants can still sue you for damages and losses, potentially impacting the profits and assets of your business. While you can't insure your business for every scenario, you don't want to be underinsured based on industry standards. Talk to your insurance representative about the right amount of liability coverage.

You don't need to have all your insurance policies with the same insurance carrier to benefit from an umbrella policy. You can have your general liability policy with Company A, commercial auto with Company B and umbrella with Company C. As long as the underlying policies meet the minimum liability coverage requirements of the umbrella policy, they are covered.

However, having all your policies with the same carrier can help you save money on business insurance. You may qualify for discounts or credits by bundling policies with the same carrier. This is because the insurance company can better underwrite the combined risk compared to separate policies.

Umbrella policies, even in high coverage amounts, are relatively inexpensive. Since they significantly reduce a company's risk, they offer excellent value. Typically, a $5 million commercial umbrella policy costs between $375 and $525 per year. A $10 million policy costs around $2,200 to $2,500 per year. Costs vary with industry, claims history and location. For example, nonprofit organizations tend to have the lowest premiums, followed by retail businesses, while wholesale businesses and building design firms often face the highest premiums.

Jennifer Dublino is an experienced entrepreneur and astute marketing strategist. With over three decades of industry experience, she has been a guiding force for many businesses, offering invaluable expertise in market research, strategic planning, budget allocation, lead generation and beyond. Earlier in her career, Dublino established, nurtured and successfully sold her own marketing firm.

At business.com, Dublino covers customer retention and relationships, pricing strategies and business growth.

Dublino, who has a bachelor's degree in business administration and an MBA in marketing and finance, also served as the chief operating officer of the Scent Marketing Institute, showcasing her ability to navigate diverse sectors within the marketing landscape. Over the years, Dublino has amassed a comprehensive understanding of business operations across a wide array of areas, ranging from credit card processing to compensation management. Her insights and expertise have earned her recognition, with her contributions quoted in reputable publications such as Reuters, Adweek, AdAge and others.