Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Car Insurance for Business: A Complete Guide to Commercial Auto Insurance

If your business operates vehicles or has employees driving for business reasons, commercial auto insurance is a must.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

If your business operates a vehicle or a fleet of cars or trucks, proper auto insurance is a critical necessity that can save your company from devastating financial consequences. Commercial auto insurance can cover your losses, including bills and expenses, when a company-owned vehicle is involved in an accident. We’ll explain what commercial auto policies entail; we’ll also share how to gauge suitable coverage to protect your organization from potentially severe legal and financial repercussions.

What is commercial auto insurance?

Commercial auto insurance is a car insurance policy designed to protect businesses and their vehicles used for work-related purposes. Unlike personal auto insurance, which covers vehicles used for personal activities like commuting and errands, commercial car insurance provides coverage specifically for vehicles owned by a business or used to conduct business operations.

The policy covers business owners, employees and other authorized drivers who operate company vehicles, unlike personal policies that primarily cover household members. It addresses unique business exposures like loading/unloading operations, carrying tools and equipment, and liability arising from business activities. These policies cover many automobiles, including cars, sports utility vehicles, pickup trucks — any vehicle used exclusively for business.

Insurers typically offer coverage through standalone policies, insurance endorsements or riders to existing policies.

1. Commercial auto

Commercial auto insurance applies to vehicles, such as trucks and cars, that you or your employees use exclusively for your business. It helps pay the costs (up to coverage limits) if you or an employee damages someone else’s property or injures a pedestrian while driving.

This policy covers three types of drivers:

The business owner

Employees operating company vehicles

Anyone permitted to drive company vehicles

2. Hired auto

Hired auto applies to cars or trucks that your business leases, rents or borrows. This policy covers medical bills and third-party damage. You can also add a physical damage endorsement to cover your company vehicle.

3. Non-owned auto

Non-owned auto covers damage to another person’s vehicle, bodily injury claims that your business caused to someone else in an accident and expenses if your company gets sued for negligence. This coverage is for vehicles that your business doesn’t own but are used by employees for business tasks.

Similar to a business owner’s policy, this insurance only provides coverage for the third party, not the policy owner. As such, this insurance doesn’t cover your company’s hired or non-owned vehicles. It also doesn’t cover medical bills if an employee was injured in an accident while driving their own car or a rented vehicle, or provide liability coverage when you or an employee is driving for reasons unrelated to the business.

Who needs commercial auto insurance?

Any business that owns vehicles or has employees drive for work-related tasks needs commercial auto insurance. Additionally, if your business rents vehicles to conduct business or if employees use personal vehicles for work tasks, you need commercial auto insurance.

The following enterprises, in particular, should obtain commercial car insurance:

Businesses that own vehicles registered under the company name

Companies whose employees drive for work purposes

Businesses that transport goods, materials or passengers for compensation

Companies using vehicles over certain weight limits (typically 10,001+ pounds)

Businesses required to provide certificates of insurance to clients

Organizations subject to Department of Transportation (DOT) regulations and interstate commerce requirements

Commercial auto insurance can be critical to your business’s survival. An often-cited study by The Hartford found that vehicle accidents are the second-costliest insurance claims for small businesses, with an average claim of $45,000. Without adequate commercial auto insurance, such incidents can devastate a business.

Bottom Line

Many types of business insurance are advisable and even required. However, commercial auto insurance is among the most critical for any company that operates vehicles in any capacity.

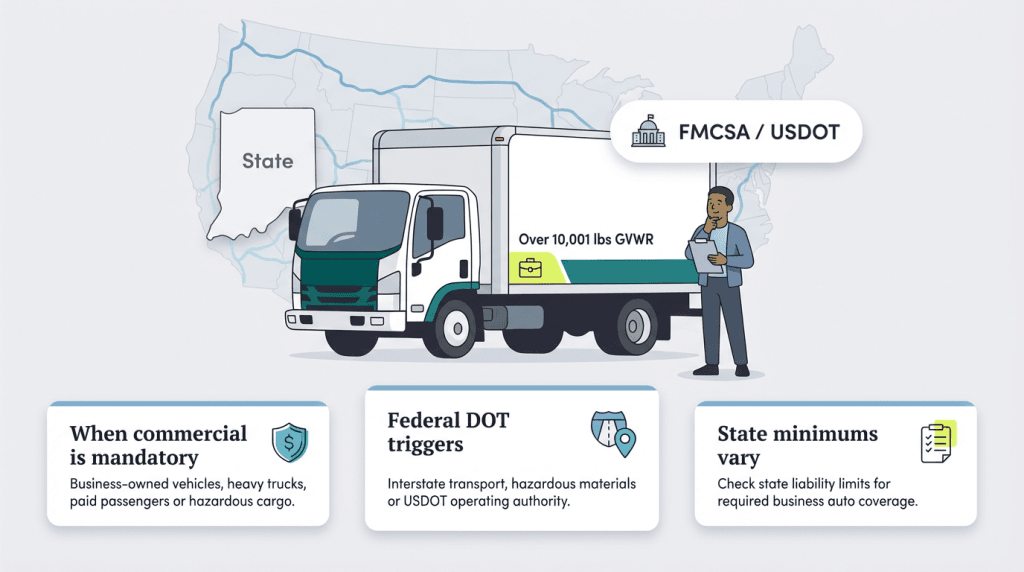

State minimum requirements and federal regulatory compliance

Understanding when your business legally requires commercial auto insurance versus when personal coverage might suffice is crucial.

Commercial coverage is legally required when:

The vehicle is registered under a business name.

The vehicle exceeds 10,001 pounds gross vehicle weight rating (GVWR) or gross combination weight rating (GCWR).

Employee drivers regularly operate company vehicles.

The business provides transportation services.

State requirements

Commercial car insurance laws vary by state, and state minimum requirements vary significantly across jurisdictions. That’s why it’s vital to consult your state’s requirements for how much commercial liability auto insurance is required; this information dictates specific bodily injury and property coverage parameters.

USDOT number requirements: Companies operating commercial vehicles transporting passengers or hauling cargo in interstate commerce must be registered with the FMCSA and have a USDOT number. Additionally, commercial intrastate hazardous materials carriers transporting types and quantities requiring a safety permit must register for a USDOT number.

Thirty-seven states require a DOT number for intrastate commercial motor vehicle registrants beyond federal requirements. These states have expanded the federal requirements to include intrastate operations that meet certain criteria.

Federal minimum insurance requirements: Minimum insurance limits that you must purchase include:

$750,000 minimum coverage for vehicles with a gross vehicle weight rating over 10,001 pounds

$1,000,000 for motor vehicles or large equipment/machinery transport

$5,000,000 for hazardous materials transport

For passenger transport:

Vehicles accommodating 16 or more passengers (including the driver) require $5,000,000 minimum coverage.

Vehicles accommodating 15 or fewer passengers (including the driver) require $1,500,000 minimum coverage.

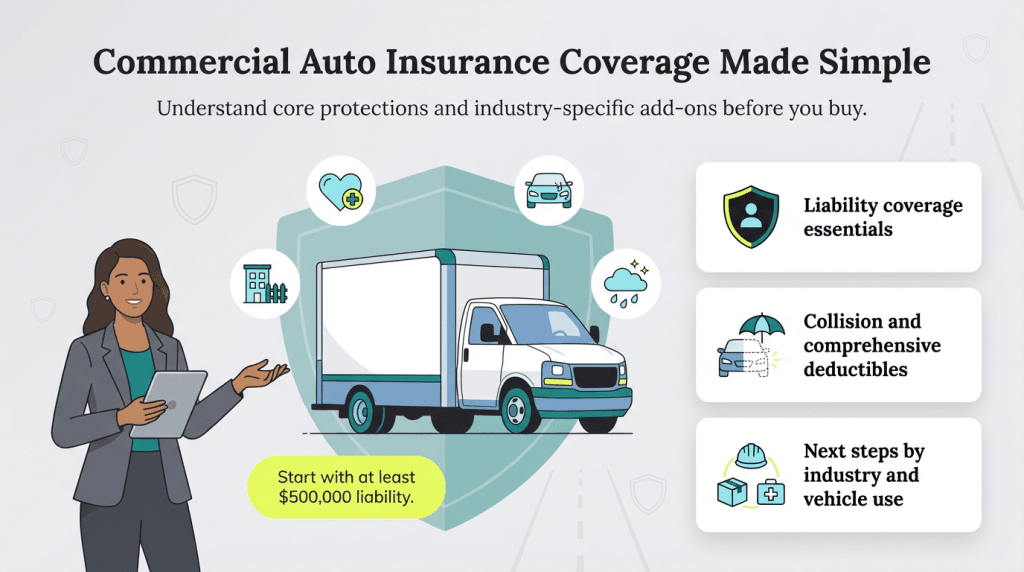

What commercial auto insurance coverage do I need?

While your exact needs may vary, Nationwide recommends at least $500,000 in liability coverage per vehicle. However, industry-specific requirements often demand higher coverage levels.

If you’re leasing a company car or truck, your lending institution may require you to carry collision and comprehensive coverage; this is to pay for damages to your vehicle if you’re at fault in an accident or the victim of non-collision events (like weather events or vandalism).

When shopping for commercial auto insurance, make sure you understand the different parts of car insurance coverage.

Liability coverage components

Bodily injury liability: Covers medical expenses, lost wages, and pain and suffering for injured parties

Property damage liability: Covers repair or replacement costs for damaged property

Combined single limit (CSL): Single coverage limit applying to both bodily injury and property damage combined

Physical damage coverage

Collision: Covers vehicle damage from collisions with other vehicles or objects

Comprehensive: Covers damage from theft, vandalism, weather, fire and other non-collision causes

Specified perils: Named perils coverage offering protection against specifically listed risks

Industry-specific considerations and specialized coverage

Different industries face unique risks requiring specialized commercial auto coverage considerations. Keep these coverages and factors in mind, depending on your sector.

Construction and contracting

Tool and equipment coverage

Increased liability for job site operations

Specialized vehicle modifications

Higher weight ratings requiring DOT compliance

Transportation and logistics

Cargo coverage and shipper liability

Interstate commerce regulatory compliance

Higher mileage and exposure

Specialized equipment and trailers

Service industries

Professional liability considerations

Customer property exposure

Service vehicle modifications

Territory and route considerations

Healthcare and medical services

Patient transport liability

Medical equipment coverage

HIPAA compliance considerations

Emergency response requirements

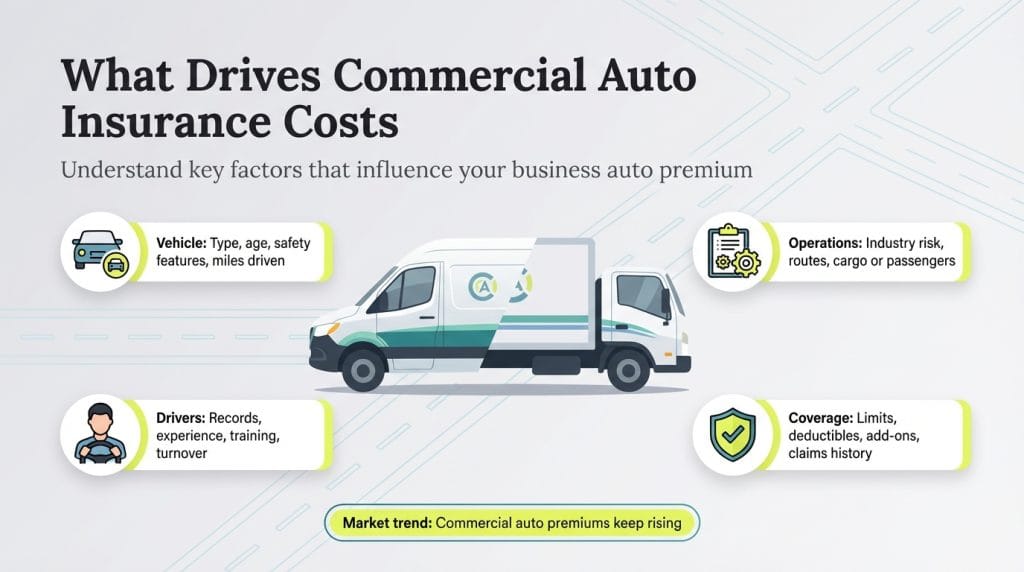

How much do commercial auto policies cost?

Commercial car insurance costs depend on several factors, including deductibles and out-of-pocket expenses. Generally, all other factors being equal, the higher the deductible, the lower the premium.

Insurer Progressive says its national average monthly cost for commercial truck insurance ranges from $767 for specialty truckers to $1,041 for transport truckers. Amistad Insurance Services estimates that its commercial car insurance ranges from $600 to $2,500 for each vehicle.

Factors affecting commercial auto insurance premiums

Some factors that can affect your business auto insurance costs include the following:

In early 2025, commercial insurance consumers of all sizes saw premium increases for the 30th consecutive quarter, with commercial auto costs experiencing a 10.4 percent increase, up from 8.9 percent in the previous quarter, according to The Council of Insurance Agents & Brokers’ “Commercial Property/Casualty Market Index Q1 2025” report.

The commercial auto insurance market has faced worsening conditions in the last decade, with profitability falling as rates continue to increase. Contributing factors to market conditions include:

High lawsuit costs: The Insurance Information Institute reported that court settlements are becoming so large that many businesses don’t have enough insurance to cover them.

Marijuana legalization: New drug laws across the country may increase the likelihood of commercial drivers operating vehicles under the influence.

How do I choose and purchase commercial auto insurance?

When choosing business insurance, including commercial auto insurance, you can shop online or contact insurers by phone. Independent insurance brokers and agents can also help match your needs to coverage limits and ensure you comply with all legal requirements.

Evaluation criteria for commercial auto policies

Before choosing your policy, compare several insurance providers’ offerings using these criteria:

Coverage details

Policy limits and coverage scope

Exclusions and limitations

Additional coverage options

Industry-specific endorsements

Financial strength

Insurance company financial ratings from agencies like A.M. Best and S&P Global Market Intelligence

Claims paying ability and history

Market share and stability

Customer service ratings

Compliance capabilities

DOT filing services

Certificate of insurance provision

Regulatory compliance support

Multi-state operation coverage

Cost considerations

Premium costs and payment options

Deductible options and impact

Discount opportunities

Total cost of ownership

Check online reviews to gauge how happy an insurer’s customers are with the company’s service, support and how promptly they pay claims. This data will provide valuable insights into the provider and ensure you opt for comprehensive commercial auto insurance coverage that fits your company’s risk management plan.

Progressive claims a 15.18 percent share of the commercial auto insurance market based on direct premiums written totaling more than $10 billion, making it the largest commercial auto insurer in the United States, according to the National Association of Insurance Commissioners’ 2024 market share report. However, you should always shop the market and compare quotes across providers to find the right fit for your unique business needs, not simply go with the most popular company.

How is car insurance for business different from personal car insurance?

There are two primary differences between commercial and personal auto insurance:

Higher coverage limits: Commercial policies typically offer substantially higher liability limits to protect business assets.

Broader coverage scope: Commercial insurance covers business-specific risks that personal policies exclude.

Nicole Urbanowicz is a small business owner who studied management and finance at Harvard, where she received her master's degree. Before becoming an entrepreneur herself, she started her career writing about business and investing for Dow Jones and The Wall Street Journal, after which she became a research analyst for Allured Business Media, using business intelligence data to develop strategic guidance.

At business.com, Urbanowicz covers a range of insurance topics, including workers' compensation, endorsements, coinsurance and more.

Today, in addition to running her e-commerce business, Urbanowicz continues to provide financial analysis and advice and uses her certification from the New York State Department of Financial Services to consult on insurance matters.