Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Adding a rider to business insurance helps you reduce costs and better protect against losses.

An insurance rider adds or modifies an insurance company’s original coverage details. You can add riders to many policies, including business and life insurance to further mitigate risk and loss exposure.

Here’s everything you need to know about business insurance riders, including key benefits, choosing the right option for your company and making a claim on your rider.

Most insurance policies come with standard coverage detailed in the contract, but there may be times when you want to add or change coverage. An insurance rider can accomplish this. You’ll usually pay extra to add a rider when you need to fill a gap in the stand-alone policy and customize your business insurance.

An easy way to remember what a rider does is in its name: additional coverage “rides along” with the existing policy.

Riders can be added to many business insurance policies, including the following:

How the rider affects the policy’s coverage depends on what’s missing in the stand-alone policy and what the rider says it will cover. The carrier will standardize each policy as the monoline policy, which is insurance coverage focused on a single type of risk. Then, business owners can add a rider to modify these policies and better protect themselves from losses.

Ask your insurance carrier about the riders available for policies you’re purchasing. Not every carrier offers the same selection of riders, which may lead you to choose another insurance company.

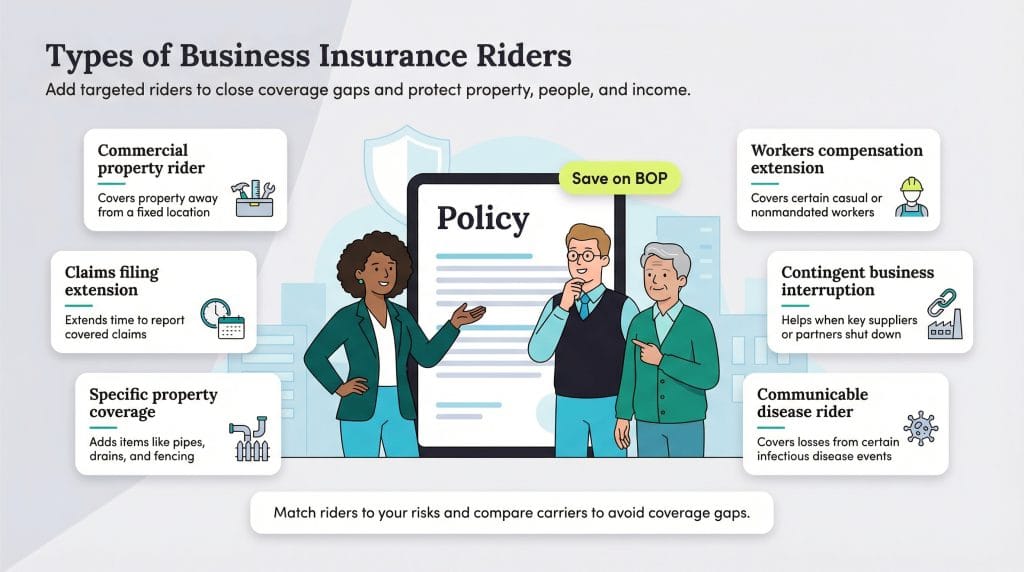

Some examples of typical business insurance riders include the following:

Neokissha Penix, an underwriting auditor who focuses on commercial insurance has noticed the most common commercial business insurance riders are commercial property riders. They are purchased to help fill gaps in coverage to protect the insured’s property.

Penix said the most common riders she funds into are for “covering property not at a fixed location. Having worked with a lot of contractors they constantly have tools/equipment at different job sites. This [rider] helps if the tools are damaged or stolen while not at the primary property location.”

Insurance riders offer many benefits to businesses, including the following.

A primary business insurance contract provides standard coverage and is generally static. The insurance carrier won’t go line by line to individualize the terms. However, your business may need more or different coverage than the standard provisions.

This is where riders come in. Riders let customers make changes to provide more comprehensive coverage — whether they need specific benefits not otherwise available or their needs have changed since their original contract was instated.

Getting riders can help business owners ultimately save money on business insurance while getting the coverage they need.

Although you must pay extra for an insurance rider, the additional cost is worth it to make sure your business is properly covered. A little extra for the right insurance is better than finding out after a loss that you were underinsured or not covered at all.

Additionally, riders usually have lower deductibles than standard insurance policies. Thus, adding a rider could increase your overall insurance payout.

Running a business can be unpredictable, even in the best of times. Modifying your insurance coverage to mitigate risk and meet your business’s present (and future) needs can bring much-needed peace of mind.

Even if you don’t purchase an insurance rider now, knowing your options can empower you to plan ahead if you need additional coverage down the line.

Buying an insurance rider is as straightforward as letting your insurance carrier know you want to add specific coverage. Riders usually cost pennies on the dollar compared to a whole new policy, making them an affordable and efficient way to add coverage.

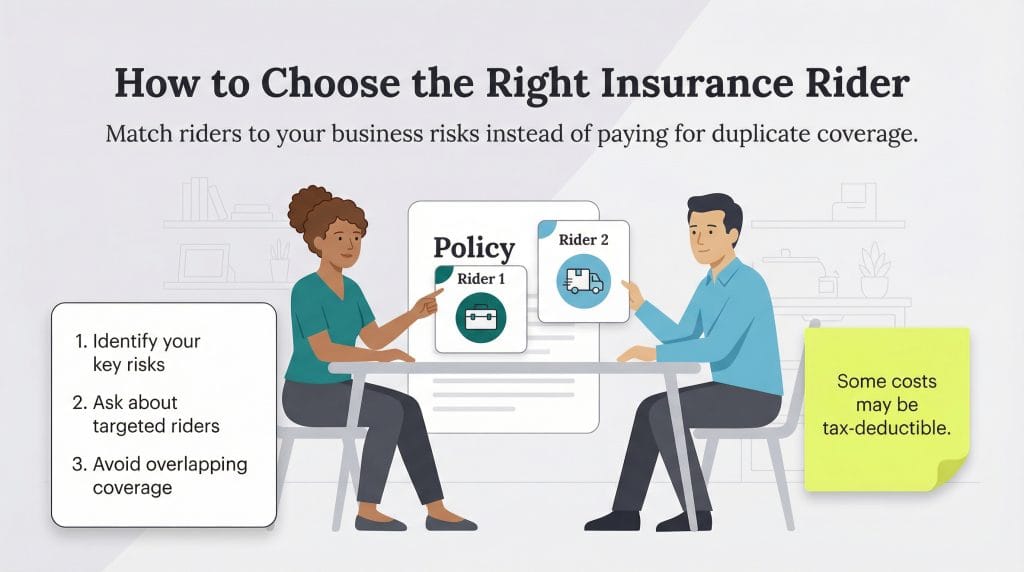

However, choosing a rider takes some consideration. When choosing business insurance, many business owners don’t think to ask about additional coverage, assuming the policy they’re purchasing covers everything they’ll need. This isn’t the case. Be sure to ask your carrier about its options to see if any riders fit your needs.

Depending on your business activities, some riders make more sense than others. Here are some examples:

Often, a specific rider will make sense for you and your business, while others won’t seem as essential. Business owners should talk to their insurance agent about their company’s needs and ask if specific riders would better protect their interests.

While a rider is an important component in having proper coverage, both insurers and insureds need to make sure the rider is right for their business. This can only come about through honest conversations about business needs, risks and the goal of adding a rider to the policy.

“Custom endorsements allow … for a more accurate pricing model. But if not done carefully in conjunction with the standard policy it could provide an opportunity for businesses to overpay for overlapping coverage if the same coverage is afforded on the standard policy,” said Sheila Flores, a commercial adjuster with years in the industry. “Being specific on endorsement language will allow the flexibility to cover specific risks.”

Of course, wrapped up with choosing the right rider is finding the best business insurance provider. We’ve saved you the trouble and researched insurance companies to find the best business insurance providers for you.

One of the great things about a rider is there is no added work if you file a claim. As long as you pay your premium, the claims process is seamless and includes losses related to the rider.

Here’s how making a claim on a rider works:

Nathan Weller contributed to this article.