Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Business expenses allow you to write off certain things on your taxes. Learn what you can deduct from the cost of your work vehicle.

When you use a vehicle for business, you can deduct various expenses from your taxes, including auto insurance. However, you may be better off taking a mileage deduction when figuring out the best tax strategy for your business vehicle. Review both options with a tax advisor to make sure you choose the most advantageous way to take the deduction.

Here’s what business owners need to know about commercial auto insurance and other vehicle expenses you can write off on your taxes.

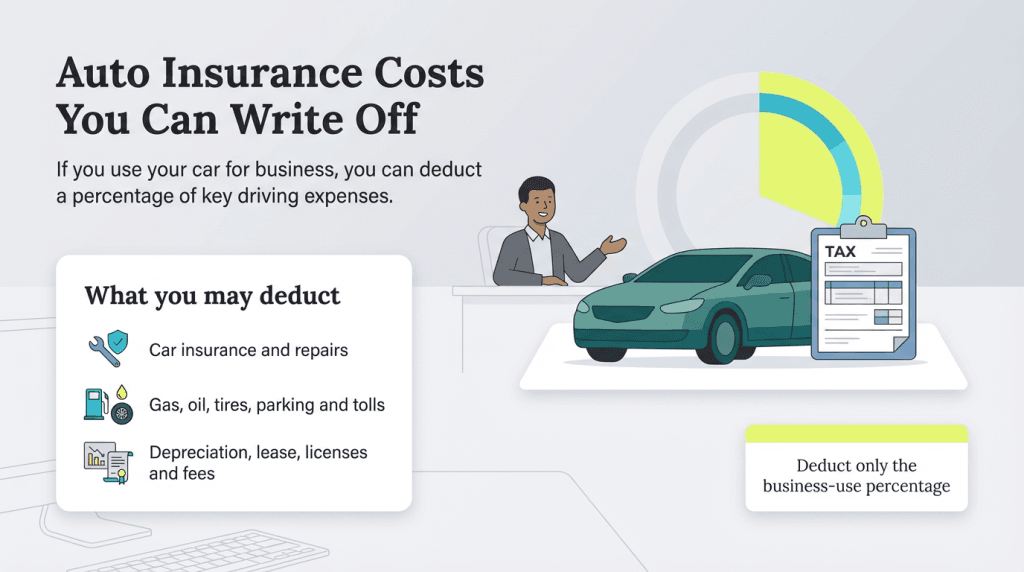

When you use your auto for business purposes, you can deduct part of the total expense associated with running and maintaining the vehicle, including auto insurance expenses. Whether you can write off every expense depends on whether you use the vehicle for personal and professional purposes or you use it exclusively as a work vehicle.

For example, an Uber or Lyft driver will use their car for personal and business purposes. When they have the app on and are on call or driving a passenger, they are on business hours. The rest of the time, they’re using the car for personal purposes. When there’s a split like this, the tax deduction will depend on the percentage of commercial usage versus personal usage. So, if the Uber driver works only 40 percent of the time, they can deduct only up to 40 percent of their costs.

When using the mileage calculation, the driver can track mileage and take a standard mileage deduction only for miles traveled while working. The 2025 standard mileage deduction is $0.70 per mile tracked for business. While you can deduct taxes, insurance costs and other auto expenses, most people opt for the mileage deduction, as it’s easier and often yields a better deduction.

Keep in mind that filing the right return allows you to take the deduction. “You must file a business-related tax return, such as a Schedule C for self-employed individuals or have a specific tax return to qualify for the deduction,” explained Adam Rauscher, vice president of insurance services at the Merit Financial Group.

If you decide to deduct actual expenses rather than mileage, you can deduct your insurance costs and a lot more. If you plan to take actual deductions, make sure to keep receipts from all maintenance and other costs to validate your claims. Realize that there are limits to what can be deducted. Dennis Shirshikov, adjunct professor at City University of New York explained, “If you use half the car for personal use and half for business, you can deduct 50 percent of the cost of your premiums and expenses.”

These are some of the expenses you can deduct:

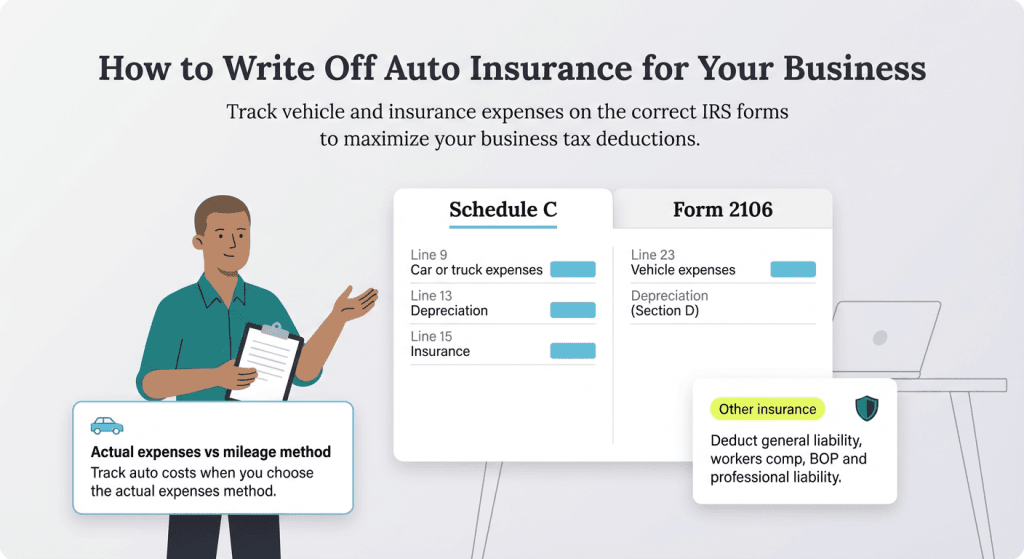

You’ll report expenses on one of two forms, depending on how your business is established. If you’re self-employed, you’ll add the information to Schedule C. If you have business entities and file Form 1120, you’ll use Form 2106 to tally the expenses.

Your business entity and how you file taxes will determine the form you use to write off your car insurance deductible. Self-employed individuals who file a personal return, Form 1040, will track expenses on Schedule C. “The business-specific portion of the tax return dealing with automobile deductions is itemized when the actual expenses method of deduction for vehicle-related business expenses is chosen instead of a standard mileage deduction,” Rauscher said.

On Schedule C, you’ll see a section to list all expenses in Part II. This is where you’ll track auto expenses. Line 9 summarizes the car or truck expenses. Line 13 tracks the vehicle’s depreciation, and Line 15 is devoted to all business insurance expenses other than health insurance. These line items, along with all the other expenses in your business, will be tallied on Line 28.

IRS Form 2106 is similar to a Schedule C in that it tracks business employees’ expenses. You’ll start with Section C for the actual expenses. Unlike Schedule C, Form 2106 doesn’t separate insurance as a line item. You’ll include your insurance with other vehicle expenses on Line 23. Depreciation is handled in Section D for vehicles.

“There is no dollar limit on what portion of the premium can be deducted for business use, but the key limitation is how much business versus personal use the car was put to,” according to Shirshikov. For the most accurate tax reporting, follow these tips:

Unless you have a vehicle that is used solely for your business, such as a delivery van, you will use your automobile for personal purposes some of the time. Determine what percentage of the time, by mileage, it is used for business. Multiply that percentage by the vehicle’s annual mileage to get the number of miles you can deduct. If you are using individual vehicle-related expenses rather than mileage, multiply the expenses by the percentage to get the amount you can write off. Remember, if you use the vehicle to commute to your office, that is considered a personal use of the vehicle, not a business expense.

As an alternative to using the percentage method, you can track the miles that you drive for business using a mileage tracker app. Each time you get in the car, launch the app and designate the trip as either personal or business. At the end of the year, the app will total all business trip mileage.

Put the receipts for all vehicle-related expenses, including vehicle maintenance, repair, insurance, gas and tolls, in a file folder. This not only makes it easy to calculate accurate vehicle expenses when you are doing your taxes, but it also serves as a printed record if you are audited at some point. The IRS may take several years to do an audit, so it is a good rule of thumb to keep these records for at least five years.

When using the expense method, you might be able to deduct local or state annual property taxes from your federal return, as long as you have not already met your state and local tax deduction maximum amount.

If you bought an electric or hybrid vehicle, you might qualify for a tax credit. This is limited based on the purchase price, the make and model of the vehicle, whether it is new or used, and your overall income.

If your vehicle was damaged or destroyed due to a federally declared disaster, such as a hurricane, flood, fire, tornado or earthquake, you may be able to write off the amount of the loss that was not covered by insurance and/or salvage value. The same applies to theft of a vehicle. However, if the money you get from the insurance company is more than the value of the vehicle, that difference is taxable as income.

Just because you can write some expenses off doesn’t mean you shouldn’t get the best rates possible. Explore our best business insurance for options.

Jennifer Dublino contributed to the reporting and writing in this article.