Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

The SBA and USDA offer loans to assist entrepreneurs and business owners who need funding.

Financing is an essential step for any company and may include finding business investors or applying for a business loan. Entrepreneurs seeking loans might turn to a bank automatically, but another significant capital funding source exists for businesses: The federal government.

Several loan programs are available to startups and growing businesses and understanding which ones suit your needs is vital to unlocking additional capital for your venture. We’ll examine popular federal loan programs and explain how they work, how to qualify and how to apply for them.

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Government loan programs are available through the federal Small Business Administration (SBA) and the United States Department of Agriculture (USDA) for qualifying businesses that intend to use the funds for specific purposes, such as purchasing equipment, expanding operations or boosting working capital.

SBA loans are provided by banks and other lenders, including community development organizations and microlenders. However, the federal government guarantees a portion of the loan, lowering lender risk. The main benefit of these loans is they offer small businesses the opportunity to receive financing on more favorable terms than they would receive without the SBA guarantee.

Here’s an overview of the most popular SBA loan programs:

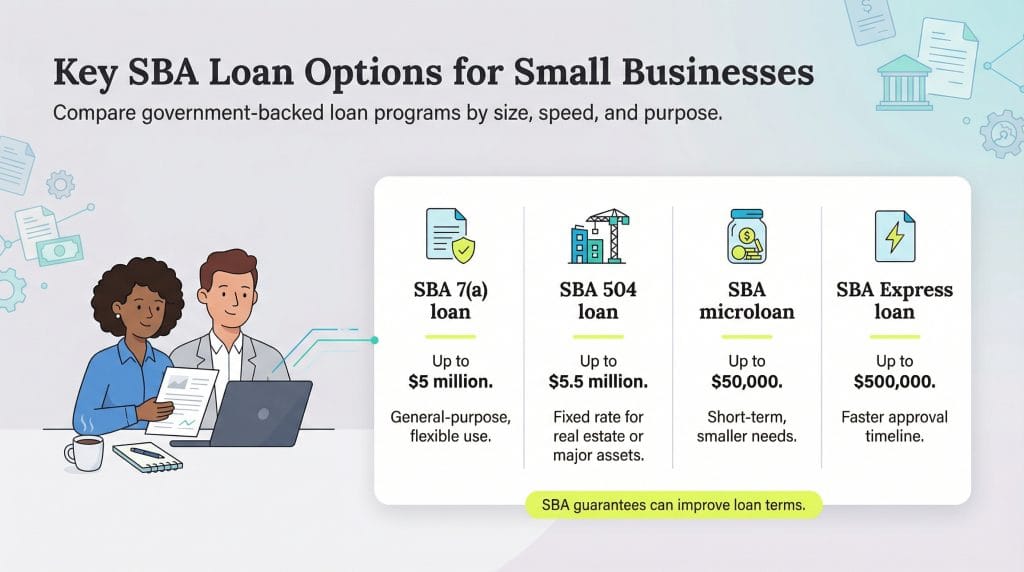

The SBA 7(a) loan is one of the most popular and flexible federal loan programs. It’s generally used to help minimize startup costs or assist growing businesses and can be used for the following purposes:

The SBA will guarantee up to $5 million for this type of loan. If you’re looking for a loan of $350,000 or more through this program, the SBA will require your lender to ask for the maximum possible amount of collateral to offset the risk of default. Note that borrowers must meet specific criteria, such as size standards and creditworthiness.

The 504 loan program is designed for businesses that will directly benefit their communities by creating jobs or meeting essential local market needs. These loans feature a fixed rate and are structured for long-term financing, with a maximum value of $5.5 million.

Typically, when a 504 loan is funded, the lender will initially cover 50 percent of the borrower’s costs, the SBA will cover 40 percent and the borrower will be responsible for the remaining 10 percent of financing the project. The borrower must personally guarantee at least 20 percent of the loan.

The SBA’s microloan program is often used for short-term financial needs, such as bolstering inventory or furnishing office space. The maximum amount for this type of loan is $50,000.

The SBA Express loan program provides expedited funding for business owners who need a fast business loan. Applications receive a response within 36 hours, though funding typically takes 30 to 60 days to complete.

Loans of up to $500,000 are available through SBA Express financing, with collateral potentially required for loans exceeding $25,000. These loans can serve as working capital (with five- to 10-year terms), lines of credit (seven-year terms) or commercial real estate financing (25-year terms).

The federal government’s disaster assistance loan program provides low-interest, long-term financing to businesses and property owners recovering from declared disasters. This program helps businesses restore their operations and properties to pre-disaster conditions after hurricanes, floods, wildfires and other natural disasters.

To be eligible for SBA loans, businesses or individuals must meet the following criteria:

After determining the SBA loan you want and ensuring you qualify, applying is the next step. Borrowers work directly with SBA-approved lenders rather than applying to the SBA itself. Many borrowers initially apply for conventional small business loans. If they don’t qualify for standard financing, the lender can then request SBA backing. Alternatively, you can apply directly for an SBA loan through participating lenders.

Note that while the SBA guarantees these loans, they are administered by SBA-partnered lenders.

The USDA is highly focused on rural areas and the agricultural industry, which is often capital-intensive. Its loan programs focus on economic development and job creation in rural communities, primarily targeting small businesses and farmers.

The USDA’s grants and financial assistance programs can be used for:

Consider the following USDA loan programs:

To qualify for USDA business and industry loans, businesses or individuals must:

Some lenders may require that borrowers meet additional criteria to qualify for USDA business and industry loans.

The USDA’s Rural Business Services Program Discovery Tool can help you learn more about the available loan and grant programs and program eligibility requirements. Consult your state’s Rural Development Office to start the loan application process.

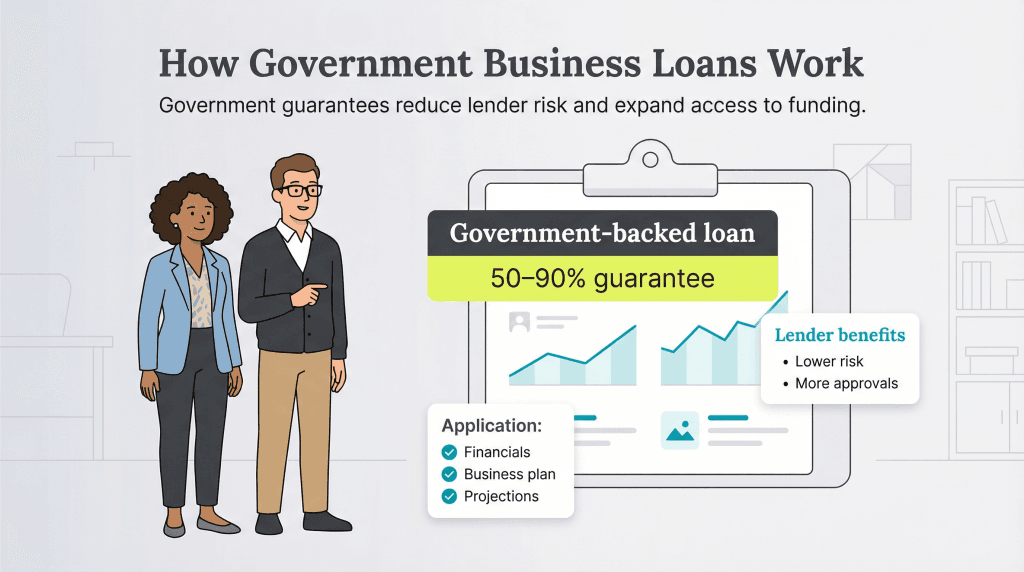

Federal loan programs typically don’t provide direct financing to businesses. Instead, the federal government guarantees a portion of the loan amount — often 50 to 90 percent — which reduces risk for conventional lenders and makes them more willing to approve loans for businesses that might otherwise struggle to secure financing.

“The SBA and the USDA provide guarantees to banks on a portion of the loan balance with a corresponding underwriting guideline that opens up the borrowing opportunity to a larger group of businesses,” explained Bernie Dandridge, a sales and operations specialist at Seaside Bank and Trust.

Businesses applying for federal loan programs must work with approved lenders and complete a comprehensive application process. This includes providing detailed financial records, business plans and projections to demonstrate your ability to repay the loan.

“[Entrepreneurs] should expect a careful financial review and be prepared with their financial documents, including a business plan,” Dandridge cautioned. “They should also understand that working capital and debt coverage are very important components in the evaluation.”

Government loan programs help businesses that might face challenges securing traditional financing — whether due to lack of credit, an unproven business model or other factors — by providing federal backing that reduces lender risk. Consider the following benefits:

Entrepreneurs entering government loan programs must consider the following:

Before accepting government-backed financing, carefully evaluate your business’s ability to meet loan obligations. Create detailed cash flow projections and consider various economic scenarios to ensure you can maintain payments even during slower business periods. If you can service your debt reliably, you should have little to worry about.

Mike Berner and Max Freedman contributed to the research and writing in this article. Source interviews were conducted for a previous version of this article.