Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

When your business needs a quick infusion of cash, what are your options? Learn about the different types of fast business loans and what you need to apply for them.

They say the only two things certain in life are death and taxes, but in business, there’s a third constant: the need for money. When you can’t immediately cover that need with your own cash or assets, fast business loans may help. These alternative lending options can get you the cash you need more quickly than many traditional lenders. Read on to learn whether a fast business loan is right for you, what you’ll need to get one, and what types of fast business loans are available.

Searching for a business loan and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

While many lenders tout speedy funding, it pays to be cautious and choose a reputable option. In our reviews of the best business loan and financing options, the following lenders stood out for their established reputations and reliable service.

| Lender | Best for | Time to fund | Loan size | Min. credit score | Min. revenue |

|---|---|---|---|---|---|

| Advance Funds Network | Fast funding | Same day | Up to $3 million | 500+ | $300,000 |

| BriteCap | Accessible funding | Same day | Up to $1 million | 500 | $75,000 |

| BusinessLoans.com | Self-service | 1–7 days | $10,000–$3 million | 500 | $100,000 |

| Fora Financial | Short-term loans | 1 day+ | Up to $3 million | 570 | $240,000 |

| CapFront | Transparency | 1 day+ | Up to $5 million | 560 | $60,000 |

| Biz2Credit | Marketplace lending | 3 days+ | $25,000–$2 million | 575 | $250,000 |

| Fundbox | Technology features | 1 day+ | Up to $150,000 | 600 | $100,000 |

| Fundera | Comparing loans | 1 day+ | Up to $5 million | 500 | Varies |

| Big Think Capital | Flexible requirements | 1 day+ | Up to $5 million | 500 | $50,000 |

| Fundible | Startups | 1 day+ | Up to $6 million | 500 | $96,000 |

For businesses that need cash fast, Advance Funds Network (AFN) is hard to beat on speed. This alternative lender has been operating since 2008 and has funded over $1 billion in capital to small and medium-sized businesses across the U.S. and Canada. AFN offers a range of financing options, including term loans, lines of credit, working capital loans, merchant cash advances, equipment financing and consolidation loans. Applications can be approved in as little as an hour, with funds deposited the same day. AFN also employs a team of more than 50 financial advisors who can help you identify the right product for your situation. The trade-off for that speed is cost — AFN’s rates tend to be higher than traditional lenders, and the company doesn’t publicly disclose specific rate ranges on its website. Learn more in our complete Advance Funds Network review.

BriteCap Financial is another same-day funding option and stands out for its accessible qualification requirements. This California-based lender has been in business for more than two decades and has provided over $1 billion in financing to more than 20,000 small businesses. BriteCap offers term loans and lines of credit (including its BriteLine revolving credit product) with a two-minute online application that won’t impact your FICO score. To qualify, you’ll need at least one year in business, $75,000 in annual revenue and a credit score of 500 or higher. One limitation to note: BriteCap currently does not offer products in North Dakota, Rhode Island and Vermont. Learn more in our complete BriteCap review.

BusinessLoans.com takes a marketplace approach, using an algorithmic matching system to connect you with the most suitable funding source from its lender network. The platform offers access to a range of loan types, including term loans, merchant cash advances, invoice factoring, working capital loans, lines of credit and equipment financing. You can borrow between $10,000 and $3 million, with terms ranging from three months to five years. Funding timelines vary; some lenders on the platform offer same-day funding, though it may take up to a week depending on the match. The self-service model is a plus for borrowers who want to compare options without extensive back-and-forth. Learn more in our complete BusinessLoans.com review.

Fora Financial is our top pick for short-term business loans, offering approval in as little as four hours and funding within 24 to 72 hours. Loan amounts range from $5,000 to $3 million, and the lender works with businesses across more than 100 industries. To qualify, you’ll need six months in business, $240,000 in annual revenue and a credit score of at least 570, no collateral required. Fora uses a factor rate pricing model (typically 1.13 to 1.50), which can translate to effective APRs of 20% to 40%, plus a 3% origination fee. The higher cost is the trade-off for speed and accessibility. One benefit: Fora offers prepayment discounts and lets you increase your funding after repaying 60% of the original loan. Learn more in our complete Fora Financial review.

CapFront sets itself apart with a focus on transparent, ethical lending. After completing the online application, you’re assigned a dedicated relationship manager who helps you weigh different products and guides you toward lower-cost options over time. CapFront offers a wide variety of financing, including SBA loans, term loans, lines of credit, merchant cash advances, invoice factoring and equipment financing, with loan amounts up to $5 million. The lender also provides credit score improvement services, bridge funding and CFO consulting. CapFront requires just a 560 credit score and three months in business — among the lowest thresholds we’ve seen. Keep in mind that while working capital products can fund within a day, SBA loans through CapFront may take 60 to 120 days.

Biz2Credit is a marketplace lender that connects small business owners with term loans, revenue-based financing and commercial real estate loans. Term loans charge simple interest (no compounding), and amounts range from $25,000 to $2 million. Biz2Credit’s application takes about four minutes, and you’ll typically receive funding options within 24 hours. Once approved, funds can arrive in as little as two business days. Each borrower gets access to a funding specialist who can help evaluate the best terms. The qualification bar is higher than some competitors — you’ll need at least $250,000 in annual sales, a 575 credit score and 12 to 18 months in business, depending on the product. Learn more in our complete Biz2Credit review.

Fundbox specializes exclusively in business lines of credit, offering up to $150,000 with terms of 12 to 24 weeks. What makes Fundbox stand out is its technology: the platform integrates directly with accounting software like QuickBooks, FreshBooks and Zoho, and uses digital tools to help you manage cash flow and determine optimal repayment strategies. Fundbox also offers a mobile app for Android and iOS and a Flex Pay service that ensures funds are always available for payroll and vendor expenses. Funding can arrive as soon as the next business day. You’ll need a minimum credit score of 600 and $100,000 in annual sales to qualify. Learn more in our complete Fundbox review.

Fundera by NerdWallet is a loan marketplace that connects small business owners with a network of vetted lending partners, including OnDeck, Bluevine and Fundbox, through a single application. The platform offers access to term loans, SBA loans, lines of credit and equipment financing, with loan amounts up to $5 million depending on the product and lender match. Fundera uses a soft credit pull during the initial matching process, so applying won’t affect your score. A dedicated loan specialist walks you through your options. The platform has helped more than 82,000 businesses secure over $6.4 billion in funding, and there’s no fee charged to borrowers for using the marketplace. Funding timelines vary by lender but can be as fast as one business day for certain products.

Big Think Capital is a funding marketplace that has helped more than 25,000 businesses access over $1 billion in financing since 2017. The platform connects borrowers with a network of lenders offering term loans, SBA loans, lines of credit, working capital advances, equipment financing and commercial real estate loans. Big Think Capital stands out for its flexible requirements — a 500 credit score and just $50,000 in annual revenue can qualify you for certain products. Working capital advances can fund in as little as 24 hours, though SBA and commercial real estate loans follow significantly longer timelines. Each applicant works with a dedicated funding manager who clarifies the trade-offs between speed and cost before you commit.

Fundible is both a direct lender and a lending marketplace, making it a strong option for startups and businesses with limited credit history. The platform offers term loans, lines of credit, equipment financing, bridge loans, invoice factoring and SBA loans, with funding amounts up to $6 million. Fundible accepts credit scores as low as 500 and requires a minimum of $96,000 in annual revenue. Same-day approval is possible, with funding arriving as soon as the next business day. The company has earned a 4.9 rating on Trustpilot across more than 600 verified reviews, with borrowers frequently praising its personalized support and fast turnaround — even for applicants who were turned down by other lenders.

Consider the following options if time is short and your financial need is immediate.

Business credit cards can provide a convenient funding source for your company. They often come with low or no fees, and you can avoid interest charges if you repay your balance on time. Approval can take anywhere from just moments to as long as two weeks.

When you apply, you may need to provide details such as your company’s size, industry and tax classification. Most of the companies and banks that offer personal credit cards also offer business credit cards.

With invoice financing — sometimes called invoice factoring — you can turn unpaid customer invoices into quick working capital. If a client hasn’t paid and you need their cash now, a financing company can advance a portion of the invoice’s value. You may receive funds in as little as 24 hours after submitting financial documents. Depending on the arrangement, either you or the financing company will collect the customer’s payment, which is used to repay the advance along with fees and interest.

Short-term loans are a broad category that includes any loan you can get within a few hours or days. These loans usually come with a quick repayment timeline — typically one to two years — and include interest and fees. Lender requirements vary, but many ask for proof of income, a credit check, and documentation showing how long you’ve been in business. You’ll usually find these loans through online alternative lenders.

A merchant cash advance is provided by your credit card processing company. You’ll get a cash infusion from your payment processor, and in return, the processor will take a percentage of your future credit card sales until the advance is repaid. Alternatively, your card processor may regularly withdraw fixed amounts from your account. You can usually get cash within a day, but your loan fees may be exceptionally high.

If you’ve ever paid for an expensive item in monthly installments instead of all at once, then you’re familiar with equipment financing. With this type of fast business loan, you can get equipment immediately and pay for it over time.

You can often be approved in as little as two days, and paperwork requirements are usually minimal. That’s because equipment financing is a low-risk option for the provider: The equipment itself serves as collateral. If you fall behind on your payments, your provider may take back the equipment, leaving you without the tools you need — and with less money than you started with. This type of financing is typically available from equipment sellers, although many banks also offer it.

You may not think about SBA loans when considering fast business loan options, in part because they’re known for their lengthy approval periods. However, for SBA loans under $150,000, you may be eligible to receive funding in as little as one week instead of several weeks. Additionally, loans under $50,000 fall under the SBA Microloan Program, which is designed for startups and small businesses and typically offers faster funding through nonprofit intermediaries.

Your requirements would be the same as those with other lenders. However, your interest rate would be lower, and your repayment term would be longer. Although SBA loans may not be as fast as other options, the better interest rates and terms may be worth the wait.

Any business concerned about waiting for approval from a traditional lender may want to consider a fast business loan. “Traditional banks tend to have a longer approval period and may have stricter standards,” explained Eric Rosenberg, a business and personal finance expert. “Other funding sources, including credit cards and online lenders, are often faster if you need funds right away.”

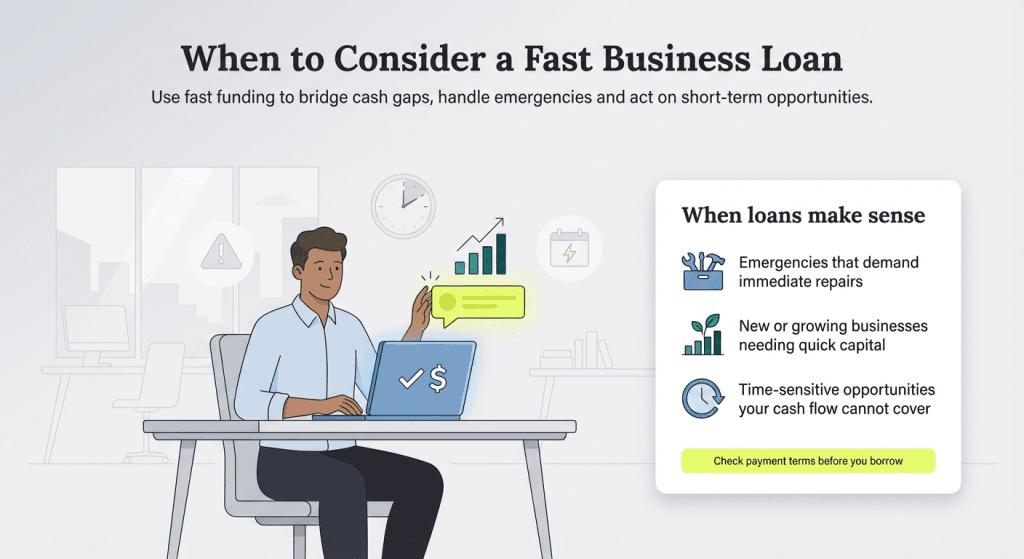

If your company is facing any of the following situations, a fast business loan might be a good option to get some breathing room and continue operations:

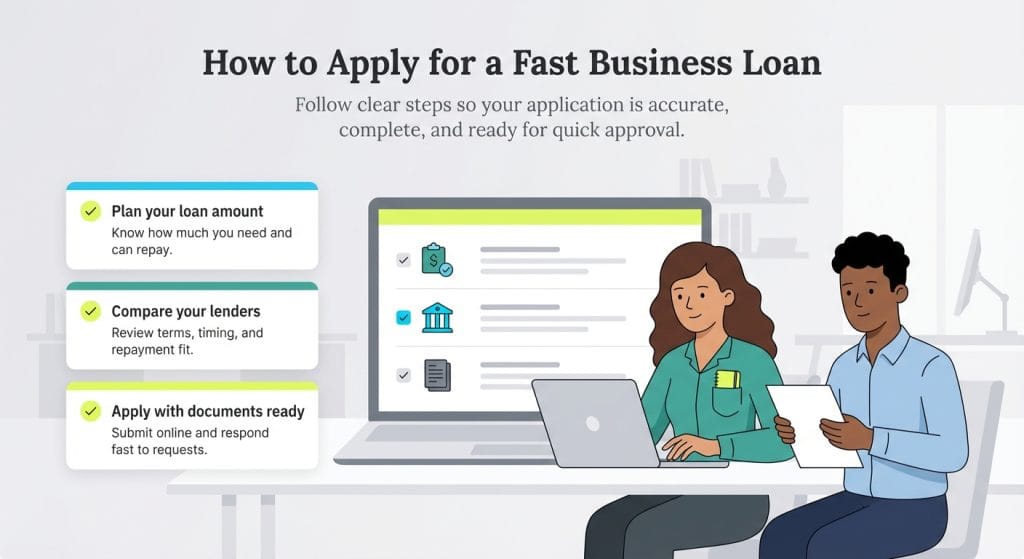

Once you decide it’s time to apply for a fast business loan, take the following steps to increase your chances of quick approval.

No two providers have exactly the same requirements. However, it’s generally safe to gather the following documents before you apply for a fast business loan:

Here are a few additional best practices to consider before agreeing to a fast business loan.

Miranda Marquit and Jennifer Dublino contributed to this article.