Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Hard money business loans offer quick access to capital and flexibility. Learn how securing this type of loan can impact your business.

Hard money loans are a common financing type in the world of private lenders. This type of funding is considered more flexible than what banks or other traditional lenders offer. Because hard money loans require borrowers to use their assets as collateral, private lenders are often more willing to work with borrowers with bad credit or more modest cash reserves.

Although hard money lending can give you faster access to cash, the process also comes with substantial risks. It’s vital to understand the pros and cons before accepting any money from a private lender.

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

A hard money loan is a type of financing based on the value of some collateral, usually real estate, the borrower offers up. A private lender will offer a loan as a percentage of the asset’s appraised value.

“What a hard money loan does is allow a company or individual to turn a real estate asset to cash, which they could use for any legal business purpose they desire,” said Jon Hornik, chairman of the Private Lender Group. “It’s a way to convert a hard asset into cash.”

A significant benefit of hard money loans is that they don’t require the same underwriting criteria conventional lenders use. Conventional lenders, such as banks, look at the borrower’s credit score, debt-to-income ratio, revenue and other factors when reviewing a loan application. Although private lenders also look at these elements, the collateral’s value is the overriding factor for hard money loans.

“The focus is mainly on the value of the asset,” said Matt Cole, executive managing director at Silver Arch Capital Partners.

Hard money loans are short-term loans backed by a collateral asset, typically some form of real estate. They are funded by a private investor rather than depositors at a banking institution. The private funding nature of the money provides lenders with more flexibility in deciding which loans to approve or deny.

When applying for a hard money loan, it’s essential to recognize that each private lender might have unique underwriting requirements. Two private lenders might handle a loan application in very different ways. However, a hard money loan generally comes back to the value of the collateral asset. You’ll request a percentage of the value of the collateral asset as a loan, which is known as the loan-to-value ratio.

Generally, lenders charge points (or 1 percent of the loan value each) that are due at the closing of the loan, as well as the principal and its interest. Depending on the loan’s terms, this can become quite expensive. Here’s a breakdown to simplify the process.

“Hard money lenders typically charge between 8 percent and 15 percent interest, which may depend on the credit history and experience of the borrower,” said Melanie Hartmann, owner of Creo Home Buyers. “The borrower’s relationship with the lender may also have an impact on the interest rate. Additionally, hard money lenders typically charge points that can either be paid upfront or added to the principal balance of the loan.”

Most hard money loans carry a 12-month term, but it’s not unheard of to find a two- to five-year term.

Some private lenders do require a deposit upon signing. The amount is generally based on the deal’s risk profile, including additional elements of the borrower’s history, such as their business credit score. The deposit could be 5 percent to 25 percent of the total value of the loan.

Proceeds from a hard money loan can be used to fund any legal business purpose. These are some of the most common purposes.

When seeking a hard money loan, you’ll need to find a nonbank lender; traditional banks and credit unions don’t offer this kind of loan. A hard money loan lender could be a financial institution that isn’t deemed a complete bank or a direct lender specializing in this kind of funding.

Caleb Liu, owner of House Simply Sold, suggested going online to find a hard money lender. “Google is a decent place to start,” he said. “There are a variety of nationwide hard money lenders. However, you should seek out hard money lenders that are active in your target market.”

Other ways to find hard money lenders include attending networking events, joining real estate investor clubs and asking for referrals. Because this type of loan requires you to pledge your assets as collateral, it’s critical to make sure the lender is legitimate and trustworthy.

Liu suggested asking these questions:

When you’re choosing a business loan, deciding between a bank loan and a hard money loan may come down to practicality factors, your timeline and your precise requirements. While evaluating your options for business lending, the following pros and cons can help steer you in the right direction.

Hard money loans offer several advantages to businesses in need of capital because they are:

Though hard money loans can help businesses land funds quickly and easily, they also come with some disadvantages like:

Since a hard money loan could end up costing you dearly if you can’t repay it within the short maturity window, why would you take one? There are good reasons why businesses take out hard money loans every day, and many successfully pay them back without incident.

Hard money loans and private money lenders typically serve businesses that fall into at least one of these categories:

A conventional lender must abide by strict underwriting requirements. A mediocre credit score or poor debt-to-income ratio can preclude businesses from obtaining a loan. Banks also typically cap the number of loans they’ll give to one individual or business entity. Hard money loans could be a way to secure more funding when you already have multiple conventional loans.

“If you have less-than-stellar credit, then hard money loans are great because the underwriting is based on the asset, not your credit history,” said Shawn Breyer, owner of Breyer Home Buyers. “Banks [also] limit the number of conventional loans that an individual can have at one time. Since hard money loans are not based on the individual, the number of loans is not restricted.”

Private lenders offering hard money loans have more approval flexibility because the money comes from private investors. Businesses that can’t get conventional financing often seek out private lenders instead.

Many businesses that could land a conventional loan still go to private lenders because their application processes are much quicker.

“Most of the time with a hard money lender, you talk to a guy who, if he’s not writing the check himself, is a decision-maker for a group of people who are,” Cole said. “It cuts right to the chase.”

The typical conventional lender’s approval process can take several months. Private lenders often approve funding within a few days.

Hard money financing is useful for construction and rehabilitation projects as well as real estate acquisition. A short-term hard money loan for these purposes lets you use the property as collateral and clear the debt from your books quickly. For businesses that want a short-term or small-dollar loan, hard money loans are more effective than conventional ones.

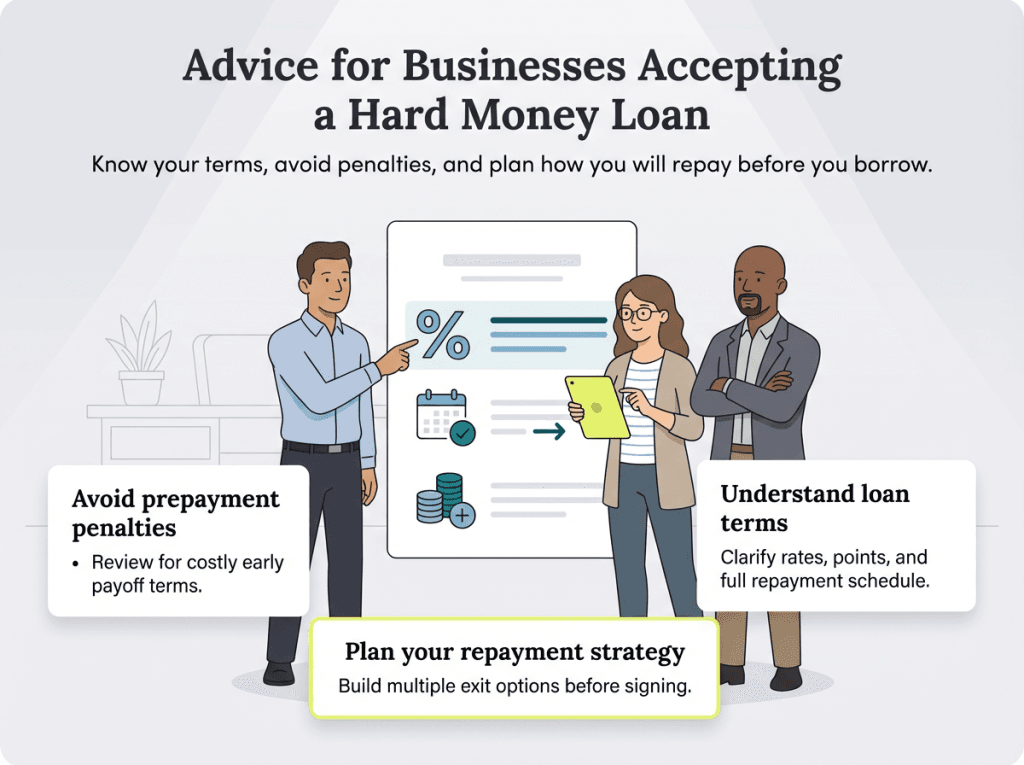

Never accept any loan, especially a hard money loan, without doing your due diligence first. Failure to repay has steep consequences, particularly when your property is on the line. Defaulting on a hard money loan opens you up to foreclosure, so take time to develop a loan repayment plan and stick to it.

Here’s some advice from the experts on accepting a hard money loan.

Steep prepayment penalties basically run counter to the idea of a short-term loan. Make sure to review the loan agreement for any clauses regarding prepayment penalties. If these penalties are excessive, stay away. Better yet, find a hard money loan that doesn’t carry a prepayment penalty at all.

“The most critical thing to look for in a hard money loan is whether there is a severe and egregious prepayment penalty,” Reischer said. “The goal of a hard money loan is to act as short-term financing. As such, if there is a severe prepayment penalty were the loan to be paid off early, then it is usually an attempt by a hard money lender to lock a borrower into a high interest rate for a long period or otherwise suffer a punitive penalty.”

You should be clear on the loan’s key elements, including the interest rate, points (a fee of 1 percent of the loan value per point) the lender charges on the loan, and when you can make those payments (upfront or on top of the principal). Always be especially clear on the repayment schedule of the loan to avoid defaulting.

The best way to make a hard money loan work for you is to first plan how and when to repay it. Ground that plan in the terms and conditions of the loan agreement. Ensure you have multiple ways to manage the repayment amount if unforeseen circumstances impact one of your strategies.

“Have multiple exit strategies planned before starting the project,” said Cassie Villela, property manager for Silverbridge Realty. “For example, if a flipped home isn’t selling by a certain date, it can be rented out and then refinanced into a conventional loan.”

These alternative loan options can provide quick access to funds but with fewer or different potential drawbacks than with hard money loans.

If you need equipment for your business and require help covering the cost, equipment financing may be a good option. The equipment you buy serves as collateral and you repay the loan over time with interest. This is an ideal option for a business that is looking to purchase machinery and can be easier to qualify for than a traditional business loan.

>> Learn More: The Ins and Outs of Farm Equipment Loans

A business with a large number of outstanding invoices and in need of immediate funds may want to use an invoice factoring company, which pays you for the invoice and collects payment from your client. For the services, the company will take out any interest or fees, and you will receive the remaining amount. The downside can be hidden fees as a result of working with the company. You can also only participate in invoice factoring if your client’s credit qualifies.

If you are looking for a loan that does not rely as heavily on collateral, a short-term loan might be right for you. Similar to hard money loans, short-term business loans have flexible requirements, and many do not require you to have any physical collateral. If you have a good credit score and have been in business for at least six months, you may be eligible for this type of loan.

The benefits of a hard money loan are numerous for businesses that can’t get a conventional loan, need capital quickly or want a short-term loan. However, their high cost and short maturity windows could prove problematic for businesses unprepared to repay quickly. Failure to repay the loan could result in foreclosure, even if you’ve performed significant work on the property.

Hard money loans make sense for businesses that need fast capital or can’t access other types of financing, but preparation and smart financial habits are key to avoiding the major pitfalls of this type of lending.

Always consult an attorney and/or an accountant before accepting a loan. Maintaining relationships with knowledgeable professionals can help you protect your business from costly mistakes that could result in closure. Never sign a loan agreement without the advice of these professionals, and always have a clear-cut plan to pay back any borrowed money.

Matt D’Angelo and Sean Peek contributed to the reporting and writing in this article. Source interviews were conducted for a previous version of this article.