Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Everything to Know About Farm Equipment Loans

Farm equipment loans are often the only way farmers and other agricultural producers can afford pricey equipment. Learn about USDA farm loans and other lending options.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Farm equipment loans are a vital financing tool for agriculture producers across the country. Whether you need to purchase a tractor-trailer, irrigation equipment or a high-tech fertilizer spreader, there are loans available that can help you buy the equipment that you need.

These farm equipment loans have proven particularly useful as farm owners modernize operations to tend to their crops. With self-steering tractors and commercial applicators that fertilize crops at the micro level, farmers need an affordable way to take advantage of the latest technological advances in agriculture. However, before you sign up with a farm equipment loan provider, there are some pros and cons to keep in mind.

Searching for loans and financing, but not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

What are farm equipment loans?

Farm equipment loans provide financing so farmers can obtain the funds necessary to purchase or lease farming equipment for their business. Farm equipment loans tend to be short-term, lasting 12 to 60 months, with the equipment serving as collateral. These types of loans typically have repayment installments made on a weekly or monthly basis. [Learn about business loan repayment terms.]

“It’s attractive to farm owners because the payments are fixed,” said Kevan Wilkinson, a small business loan expert. “You always know your payment, like a mortgage. There’s never a surprise.”

There are two options with farm equipment loans: Financing and leasing. When you finance the purchase, you own the equipment once the loan is paid off. In contrast, when you lease the equipment, you must return it at the end of the lease term or make a balloon payment to purchase it.

Leasing may be more sensible if you don’t need the equipment for a long period of time or if you plan to upgrade the equipment every few years. Leasing protects you from depreciation. However, the downside of leasing is that you can’t write off your lease payments on your business taxes, nor are you able to build equity in the equipment.

For either financing or leasing equipment through a farm equipment loan provider, you can get speedy approval and funding. That is critical if you’re trying to replace expensive equipment that is essential to keeping your operation moving forward.

“Banks require collateral and, in most cases, they also require a lot of financial paperwork dating back two or three years and a higher credit score,” said Wilkinson. “Most farm equipment lenders can loan up to a quarter-million dollars the same day as you apply.”

Tip

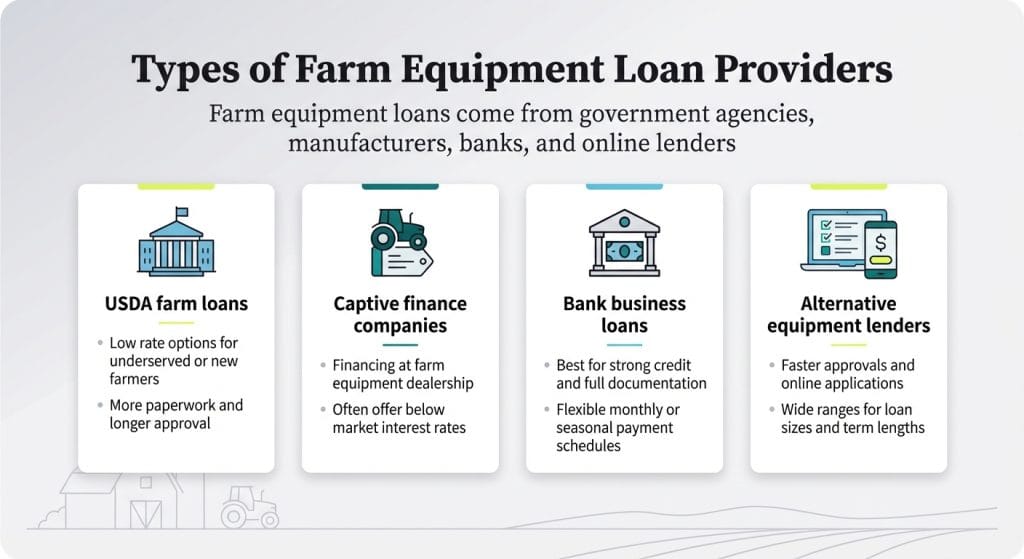

If you need farm equipment financing fast, you might want to search for a captive finance company or an alternative lender. These funding providers offer online applications, fast approvals, minimal documentation requirements and quick turnaround times. However, they charge more interest than what banks charge.

Who are farm equipment loan providers?

Options abound for farmers and others in need of farm equipment funding. From government-backed loans to alternative lending, here are the top providers offering farm equipment loans.

United States Department of Agriculture (USDA) farm loan programs

The USDA provides financing to farmers and ranchers to get started, expand or maintain their farms. The loans are aimed at borrowers who can’t secure credit elsewhere. Zach Ducheneaux, administrator of the Farm Service Agency at the USDA, said many of the loans go to socially disadvantaged farmers, those who are starting out or those who have faced economic hardship.

The USDA offers both direct loans and loans the government agency guarantees for lenders. It’s similar to the Small Business Administration’s loan program. “Because of the way the statute is written, borrowers can’t come to us first. In many circumstances, they have to try to get credit elsewhere and prove they tried to get credit elsewhere,” said Ducheneaux.

Eligible borrowers pay low interest rates with USDA farm loans, but there tends to be more paperwork and longer approval times. The USDA offers several loan types, including the following:

Operation loans: These loans can be used to purchase livestock, seed and farm equipment. They can also be used to cover operating costs and living expenses when you’re getting a farm up and running.

Farm ownership loans: Proceeds from these loans can be used to purchase a farm or ranch or expand an existing one.

Microloans: These are small-sized loans of around $50,000 or less. They’re aimed at new farmers and ranchers who need a small amount of startup capital.

Emergency loans: These loans help ranchers and farmers recover from hardship caused by a natural disaster or other calamities, such as a global pandemic.

Bottom Line

The USDA offers low-interest loans for farmers who otherwise find it difficult to obtain financing.

Captive finance companies

The farm equipment industry is dominated by a few vendor names, some of which have their own financing departments. Known as captive finance companies, these lenders work with you at the point of sale to provide financing for your purchase.

John Deere Financial is an example of a captive finance company. It offers financing for its products through its dealers, similar to vehicle manufacturers. “Oftentimes, the products will carry some incentive such as a low rate,” said Ryan Steenblock, John Deere Financial’s director of marketing for the U.S. and Canada. “It’s very much like you see in the auto industry.”

The interest rates from captive lenders vary, as they depend on your business’s performance and credit profile. Other leading farm equipment manufacturers that offer farm equipment loans include AGCO and CNH Industrial.

FYI

One advantage of captive lenders is that they often provide loans at below-market interest rates.

Bank loans

For borrowers with good credit, getting approved for a business loan from a bank is another option. Farm Bureau Bank is a popular lender for farmers, given its focus on agriculture businesses since 1999. Borrowers can pay back their loans monthly, quarterly, semiannually or annually. The bank may require a down payment and you’re typically required to provide a lot of documentation. [Read our roundup of the best small business loan options.]

AgDirect: AgDirect offers farm equipment loans for purchases at dealerships starting as low as $5,000. Repayment terms can be as long as seven years. Interest rates start at 7.75 percent and vary depending on the length and size of the loan and your credit history.

Balboa Capital: The lender requires borrowers to be in business for a minimum of a year, have a moderate credit score and earn $100,000 in annual revenue. Balboa Capital offers same-day funding of up to $250,000, an online application process and doesn’t require collateral. It also has flexible term lengths and fixed monthly payments.

Farm Credit Mid-America: This company provides a variety of loans for farmers and ranchers, including farm equipment loans. It offers loans as small as $1,000 and doesn’t cap the loan size at a specific limit. For loans of $75,000 or less, you can apply directly on the lender’s website. Farm Credit Mid-America has both short-term loans and lines of credit for farm equipment.

Pros and cons of farm equipment loans

Farm equipment loans can bridge the gap between your current resources and the equipment you need. However, as with any loan, it’s important to weigh the pros and cons before deciding if this financing option is right for your farm.

Pros

Acquire essential equipment: Farm equipment loans allow you to purchase necessary equipment when you need it, even if you can’t afford all the costs upfront. This can be crucial for starting or expanding your farming operation.

Spread out costs: Farm equipment loans break down the cost of expensive equipment into manageable monthly payments. “The majority of producers will leverage some kind of financing for purchasing farm equipment either [utilizing] installment loans or leases,” said Steenblock. “A major benefit is the ability to preserve cash flow. You don’t have to invest all the capital upfront.”

Tax benefits: In some cases, interest payments on farm equipment loans may be tax-deductible. Consult a certified public accountant to see if this applies to you. This potential tax advantage can further improve the affordability of the loan.

Lower interest rates: Farm equipment loans may have lower interest rates compared to other types of business loans, especially if you have good credit and qualify for government-backed loan programs.

Cons

Debt burden: Farm equipment loans add to your overall debt burden. Consider your ability to make the monthly payments carefully before taking out a loan. Make sure your farm’s income can comfortably support the additional debt to avoid financial strain. [Find out more about business debt.]

Depreciation: Farm equipment depreciates in value over time. You may end up owing more on the loan than the equipment is worth (also known as being “underwater” or “upside-down” on the loan). This can be a concern if you need to sell the equipment before the loan is paid off or if the equipment becomes obsolete.

Down payment requirements: Many farm equipment loans require a down payment, which can be a significant expense. Be prepared to make a substantial initial investment alongside the loan.

Farm loan FAQs

Equipment eligible for farm equipment loans runs the gambit from farmland to tractor-trailers. Wilkinson said loans can be used for any equipment you need to operate a farm or ranch. Balboa Capital gets a lot of requests for farm irrigation and water-dispersing equipment. Other popular products farmers borrow money for include equipment to lay seeds, fertilize the soil and maintain crops.

The documents required for farm loans vary by provider. Depending on the lender you work with, you may be required to provide reams of documentation or financial information for the past several years.

A USDA loan requires you to provide the following documentation:

A business plan detailing your operations now and into the future

Three-year financial history

Three-year production history

List of current creditors

A balance sheet

Your projected actual income and expenses

Description of your farm training and experience

Tax returns for the past three years

Leases and contracts

Environmental compliance information

A loan from an alternative lender requires you to provide the following documentation:

Government-issued ID

Bank statement

Tax returns

Business financial statements

Federal tax ID number

Farm equipment loans tend to have short term lengths. You can typically finance the purchase of farm or ranch equipment across as little as 12 months to as long as seven years.

A farm line of credit is designed to meet the operational needs of farms and other agricultural businesses. It's similar to a business line of credit, except that repayment terms are based on farms’ unique cash flow cycle and seasonal nature.

Who is eligible for an agricultural loan may depend on the lender. Generally speaking, however, agriculture loans are designated for farmers who are starting out or those who have an existing farm or ranch and have extenuating circumstances. There are loans available for struggling farmers and those who are underrepresented historically in the industry. Your credit profile and financial performance will also determine which loans you’re eligible for and the interest rate you'd pay. The higher your credit score, the less it typically costs you to finance the purchase of farm equipment.

You can potentially get farm equipment financing if your credit score is low. Many alternative lenders consider factors other than your credit score when reviewing your application. But if you're turned down, USDA farm loans are a great option. The USDA is designed to be a lender of last resort. They require you to apply elsewhere for a loan first before turning to the agency for assistance. These loans offer low interest rates and flexible terms, but there is a lot of paperwork involved when applying for these loans. With a USDA farm equipment loan, you must provide a detailed business report, which isn’t a requirement with some alternative lenders and captive finance companies. See our full guide to business loans you can get with bad credit for more information.

Although there is no one-size-fits-all answer to this question, lenders will look carefully at your farm’s cash flow to determine appropriate debt levels. In general, farm lenders like to see a debt service ratio (operating income divided by principal/interest) of at least 1.5.

Mike Berner contributed to this article. Source interviews were conducted for a previous version of this article.

Donna Fuscaldo, who has 25 years of experience navigating the convergence of business, finance, and technology, is a trusted advisor to small business owners. Her expertise in business borrowing, funding, and investment strategies equips her to provide reliable counsel on everything from business loans to accounting and retirement benefits.

At business.com, Fuscaldo covers business grants and other financing options, business credit cards and retirement funds.

Her analysis has also graced publications like The Wall Street Journal, Dow Jones Newswires, Bankrate, Investopedia, Motley Fool, Fox Business and AARP, solidifying her authority in the field. Beyond her contributions to the financial landscape, Fuscaldo also lends her wisdom on employment matters, with her expertise sought after by platforms like Glassdoor and others.

Armed with a bachelor's degree in communication arts and journalism, Fuscaldo has the unique ability to simplify complex business and career-related topics into actionable insights. This makes her a valuable resource for professionals seeking practical solutions in today's dynamic business environment.

Armed with a bachelor's degree in communication arts and journalism, Fuscaldo has the unique ability to simplify complex business and career-related topics into actionable insights. This makes her a valuable resource for professionals seeking practical solutions in today's dynamic business environment.