Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

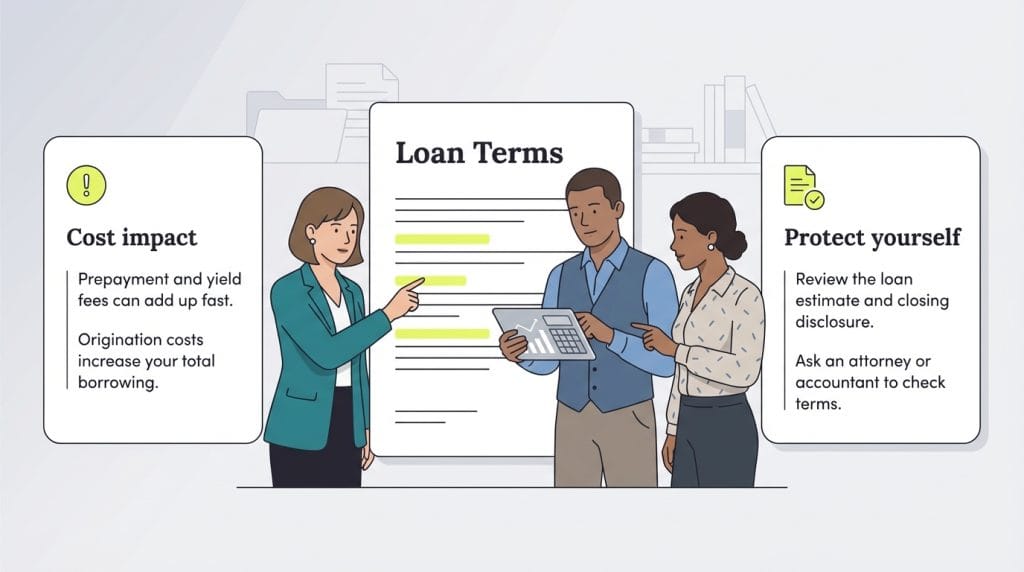

Discover hidden terms and fees in loan agreements to avoid surprises beyond your monthly payments. Learn what lenders might include.

Business loans are often an important aspect of launching and growing a small business. However, it’s easy to get in serious trouble when taking on debt. Some lenders may include terms and hidden fees in loan agreements that cause debt to balloon – which can potentially put your business in significant financial trouble.

By closely reviewing loan agreements a lender offers (along with asking an attorney or accountant to review them), you can arm yourself against an unfair repayment program. Know your loan repayment options and when it’s time to seek funding elsewhere. This guide will introduce you to the concept of business loan repayment, as well as outline certain terms and fees to look out for.

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

So you need a business loan. The process begins with a loan application, generally submitted to a bank, credit union or private lender. The lender then considers the borrower’s application, often assessing factors like income, credit score, cash flow, cash reserves and collateral, when applicable. Based on these factors, a lender might approve a borrower’s application and extend a certain set of terms: A lender offers X dollars at Y interest rate over Z months or years.

“Once funds from an approved loan are disbursed, interest begins to accrue immediately and is usually expected to be paid monthly,” said Larry Fuschino, owner of Overwatch Consulting. “Principal of the loan is to be repaid based on the terms of the loan, which can vary with each situation and borrower. However, these terms will be disclosed in the documentation provided by the lender.”

There is more to it than that. In addition to the principal, interest rate and repayment term, many lenders include other fees and terms in their loan agreements. For entrepreneurs, it is crucial to understand every aspect of the agreement before accepting a loan, as they can sometimes contain gotchas that can lead to significant expenses.

One of the most important elements of a loan is the repayment term, which is the amount of time it will take to fully repay the loan debt and the interest associated with it. In some cases, the loan can be repaid before it reaches maturity; in other cases, borrowers face a steep penalty for doing so.

“The repayment term is also known as the loan period, or the duration of time over which the borrower will complete repayment of the loan to the lender,” said Jared Weitz, founder and CEO of United Capital Source.

The terms can vary by nature of the loan. However, the repayment term and whether you have the option to repay the debt early without penalty are key factors in determining whether a business loan is right for you.

Whereas your loan term is the entire duration over which you repay your loan, your loan period is the amount of time that passes between payments. For example, if you make monthly loan repayments over five years, your loan term is five years and your loan period is one month.

You’ll also see “loan period” used to describe the time of year during which a loan is available, but this definition is less pertinent to small businesses.

Loan repayment terms vary drastically. Review the standard financing terms of each type to determine which one works best for your business. A good idea for any type of loan is to calculate the total loan cost. The total loan cost reflects how much you pay in full at the end of the terms.

FREE TOOL: Loan Payment Calculator

These are some of the most common types of loan repayment policies.

Term loans follow a set repayment schedule. The bank or lender provides you with a specific amount of time to pay back the loan. For instance, you may have a total of fixed monthly payments to make over the course of five years. After five years, as long as all payments are made, the loan is paid in full. Term loans often have a fixed interest rate agreed upon at the start of the loan. However, variable interest rates can also apply to term loans.

There are subcategories of term loans. Term loans are separated into short-, intermediate- and long-term loans. Short-term loans usually require repayment within 12 to 18 months. Intermediate-term loans range from one to three years. Long-term loans’ repayment periods range from three years to 25 years.

Among private term loan providers, small businesses may benefit the most from SBG Funding and its flexible loan payment terms. Your SBG Funding loan term can be as short as six months or as long as five years. Learn more in our SBG Funding review.

Loans from the U.S. Small Business Administration (SBA) have specific repayment terms. The maximum loan amount for the standard program from the SBA is $5 million. Interest rates are variable based on the lender, but they must not exceed the maximum amount permitted by the SBA. For example, the SBA states that 7(a) loans of $50,000 or less must not have a total interest rate above 6.5 percent plus the current prime rate. The prime interest rate as of July 2025 is 7.5 percent, so that means that the SBA mandates the maximum interest rate for this type of funding to be 14 percent. Keep in mind that oftentimes SBA interest rates are variable rates, so they will change throughout the lifecycle of the loan.

The loan terms for SBA lending programs depend on how you plan to use the funding. For working capital and daily expenses, you must repay the loan within seven years. For any equipment purchases, the loan terms are up to 10 years. If you plan to use the SBA loan for a real estate purchase, your business has up to 25 years to pay back the loan.

Although SBA loans are government loans, many private companies excel at helping small businesses find them. One such lender is Truist, which offers loans with terms spanning five to 25 years.

A merchant cash advance is ideal for a business that relies on credit card and debit card sales. Funding is provided upfront in exchange for a percentage of the company’s future sales. Merchant cash advance terms are short, with repayments usually made within three to six months. Terms for merchant cash advances are typically faster depending on your business sales. Payments for merchant cash advances could happen daily. For instance, payments may be 10 percent of your daily credit card sales.

Microloans offer a short-term option for financing. The maximum time frame is six years, but most loans require repayment in three to four years. The maximum amount for a microloan is $50,000, according to the SBA. Interest rates for microloans are established by the current rates set by the U.S. Department of the Treasury.

In the case of microloan provider Accion, microloans also open you up to one-of-a-kind, customizable loan repayment terms. When you choose Accion for your microloan, you and the company will work together to craft unique loan terms that work for you.

A business line of credit provides you with a predetermined amount of money you can use for your business. Instead of paying interest on the total amount, interest is applied to how much is utilized. A business line of credit works similar to a credit card, so there’s not a set repayment date given.

Invoice financing works as an advance against any unpaid invoices your business may have. Invoices are submitted to the lender, and the company provides you with the amount of each invoice minus any interest fees. These loans are short term and usually paid off within three months after invoices are paid by clients.

When accepting a loan, you need to be sure you will make payments on time. Never take on debt that you can’t service. However, it’s also important to be sure you’re getting a fair deal. Just because a lender is extending funding to your business doesn’t mean it’s doing so on fair terms. There is more to a loan than paying the monthly installments. You should closely review any loan agreement before you sign it.

Matt D’Angelo and Sean Peek contributed to the reporting and writing in this article. Source interviews were conducted for a previous version of this article.