Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

When considering accepting a business loan, it’s important to develop a repayment plan. Here’s how to calculate loan payments.

So you’re looking for one of the best business loans or financing options available. That’s great, but how do you know if you can actually afford it? Before you borrow funds for your business, calculate the monthly loan payments and determine whether you have the cash flow to support new debt. Irresponsible borrowing is one of the biggest reasons companies go bust, so this isn’t a decision to take lightly.

This article will demystify the financial jargon and terminology you might encounter when choosing a small business loan. We will also walk you through the math of a business loan so you know how to compute your monthly payments. (Don’t worry, the math isn’t that hard!)

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Before we get to the math, we need to define a few key business loan terms. In order to calculate what you would owe on an interest-only loan, you must first understand the following factors.

“Small business owners should look closely at interest rate, payment frequency and any fees when evaluating loans,” said Jeff Zhou, co-founder and CEO of Fig Loans.

You should also understand the different types of business loans, added Erik Jacobs, Circuit Judge for the 17th Judicial Circuit Court, Winnebago and Boone Counties. “The best advice for a novice is to speak with their attorney or accountant about what loan type may be more advantageous to them,” Jacobs said. “Critical is the deeper cash flow analysis … to determine whether the business generates enough income to be able to make the loan payments comfortably.”

Once you understand the terms and factors, calculating a business loan payment is much easier than you might think. All you need to know is the right formula for your particular loan, and then you can simply plug-and-chug. Here we’ll go through the math of an interest-only loan.

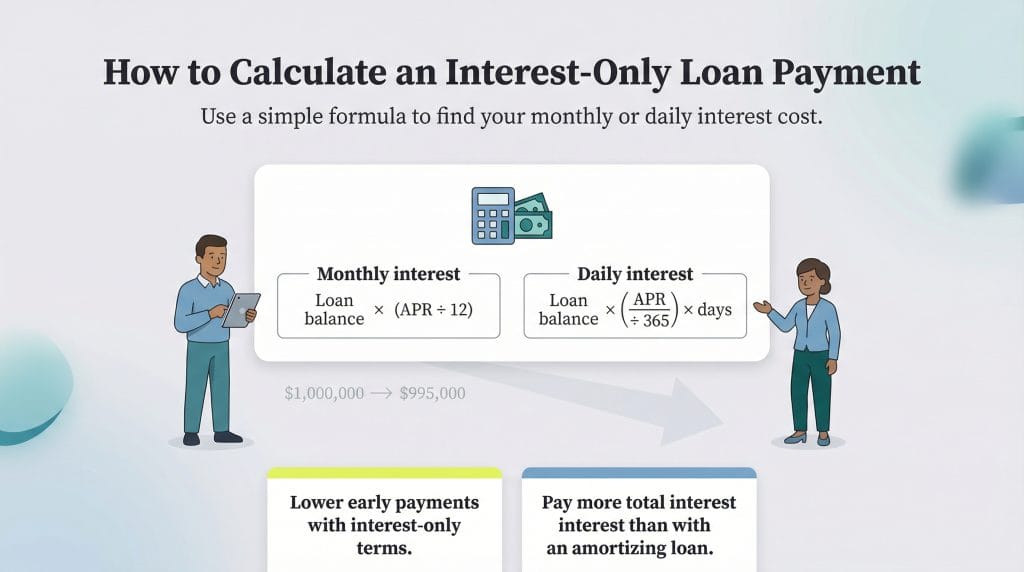

With an interest-only loan, you only pay down the interest portion of the debt for the first few years. The annual payment on an interest-only loan is calculated by multiplying the principal amount of the loan by the interest rate.

To calculate your monthly payments, apply the following formula:

Interest = Loan balance x (interest rate/12)

As an example, let’s calculate the monthly payments on a $1 million interest-only loan.

If you want to understand the second month’s payment, apply the same formula with the new balance of the loan. Here’s an example that builds on the first calculation.

Repeat this process for each subsequent month, adjusting the loan’s outstanding balance accordingly, to determine your monthly payment.

“If you pay down the principal of the loan, all you need to do is update the original $1 million with your new total principal and the calculation is good to go,” Zhou explained.

Alternatively, he said, you could calculate your loan payments on a daily basis by applying a similar process known as actual/365.

“The easiest way to calculate loan interest and payment for set amounts of time is to transform everything into days,” Zhou advised. “Interest rate is generally expressed as APR, which stands for ‘annual percentage rate.’ This can be turned into a daily interest rate by dividing the APR by 365. Then, all you need to do is multiply the total amount borrowed, the number of days [in the term], and the daily interest together to calculate how much interest you owe for that period of time.”

The advantage of an interest-only loan is that your payments are lower in the beginning. The downside is that you end up paying more interest over time than you would with an amortizing loan.

What happens if you have to make loan payments beyond covering the interest?

“If you are talking about the percentage of the loan amount that is being repaid in each payment over a period of time, then you are talking about amortization,” Jacobs said.

Amortization is the process of gradually repaying a loan through regular payments consisting of both principal and interest. At the beginning of the loan term, you might be surprised at how much of your payment is going to interest. The interest portion will be high because the loan balance starts out high. As you pay down the loan, the interest component shrinks until you get to the point where you are only paying the principal.

“Amortization would depend on a number of factors, such as interest rate and repayment term,” Jacobs explained. “Depending on your industry, business loans might have a 20-year amortization, [but] a five-year loan is more typical.”

Computing payments on amortizing loans is a bit more complicated than interest-only loans. To calculate an amortizing loan payment, use the following formula:

Loan amount x [ (r/12)/ 1 – (1+(r/12))^–n]

where r is the interest rate (expressed as a decimal) and n is the total number of payments over the life of the loan.

Let’s use our previous example of a $1,000,000 loan at 6 percent interest, except now it carries a term of five years, or 60 monthly payments. In that case, we would calculate the monthly payments like this:

Here’s what that looks like written out:

$1,000,000 x [(0.06/12)/(1–(1+(0.06)/12)^–60] = $19,332.80

Some business loans include what is known as a balloon payment at the end of the loan term. These types of loans are structured so your monthly payments at the beginning of the term are low. At the end, however, you will owe a larger lump sum, or balloon payment.

For example, an amortization schedule could include the interest payments needed to pay down a 30-year loan over a five-year period. During the first five years, the principal balance is reduced through amortization payments. At the end of the five years, a borrower might owe a balloon payment to cover the remaining balance on the 30-year loan, the principal balance of which has been reduced over the five years of amortization payments.

Jacobs noted that many business owners get their loan terms rewritten before the balloon payment. Either way, make sure you understand the fine print of balloon payments so you don’t face a nasty surprise from shady small business lenders. You might also consider opening a business line of credit if you only need the money for a short-term project or an emergency.

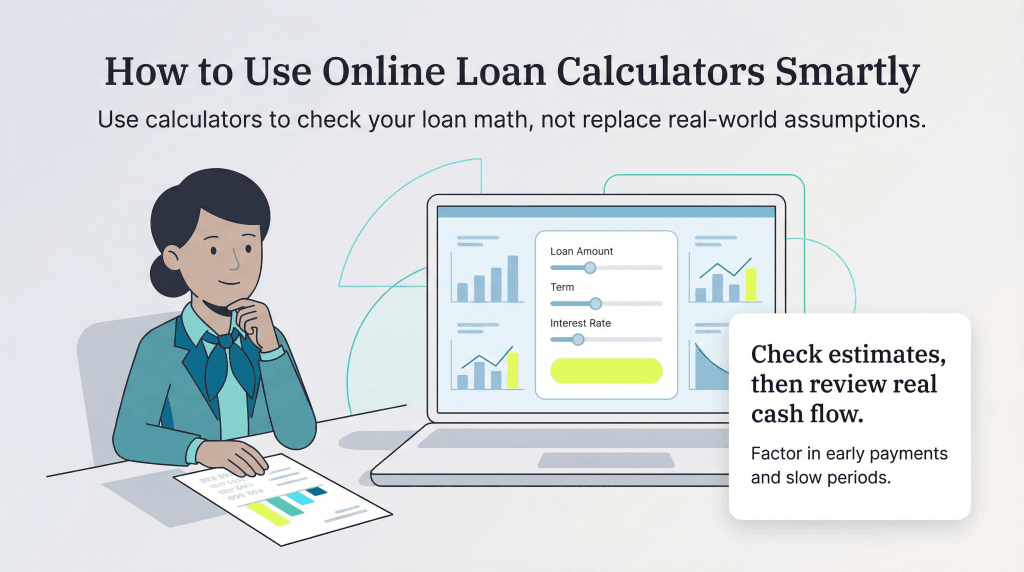

Online loan calculators are simple, free tools that allow you to easily check your work. For example, business.com offers a loan payment calculator and debt payoff calculator to help you estimate your borrowing costs. While this is useful for calculating a rough estimate, these tools can’t always account for the big picture. Therefore, you should use online loan calculators as a supporting tool rather than relying on them for everything.

“Online loan calculators are convenient but make multiple assumptions that are hidden from [small business owners],” Zhou said. “The biggest limitation of a loan calculator is the assumption of regular fixed payments. This rarely happens in reality, because you will want to pay early when the business is doing well and potentially extend the loan during less ideal times.”

Before taking out a loan, small business owners must consider whether they have the cash flow to both service the debt and continue normal business operations. An otherwise healthy business can rapidly spiral into failure if its cash flow doesn’t cover debt payments. That is especially true in a rising interest rate environment, where payments on variable interest rate loans can fluctuate over time.

“Pay attention to how much a small change in the interest rate makes over the life of the loan,” Jacobs warned. “The SMB owner should also be prepared to understand how their business will generate the income necessary to make the loan payments.”

By using these formulas to calculate your loan payments, you will be better positioned to decide which type of business loan is right for you. You’ll also be able to make sure your payments don’t interfere with your ability to pay the necessary expenses for your company. Loans are a great tool for small businesses, but many entrepreneurs eventually find themselves buried under debt they can’t afford. To avoid this all-too-common problem, do the math ahead of time and develop a repayment strategy. If you are uncertain, meet with a business accountant or financial professional who can walk you through the loan.

Julie Thompson and Adam Uzialko contributed to this article. Source interviews were conducted for a previous version of this article.