Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

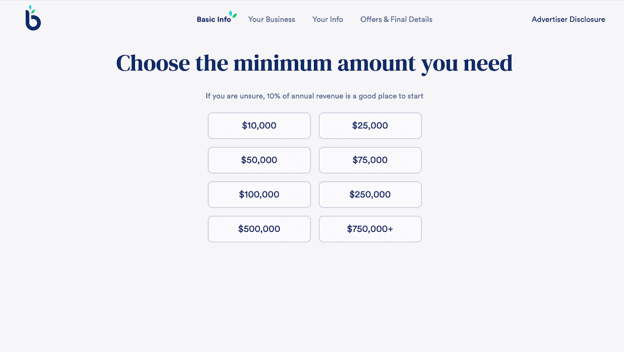

BusinessLoans.com is not a lender. Instead, it operates as a lending marketplace that matches businesses with financing from a network of lending partners. Based on our testing and information provided by the company, borrowers may qualify for loans ranging from $10,000 to $3 million. Rather than applying with individual lenders one at a time, business owners can answer a series of questions and compare potential financing options in one place.

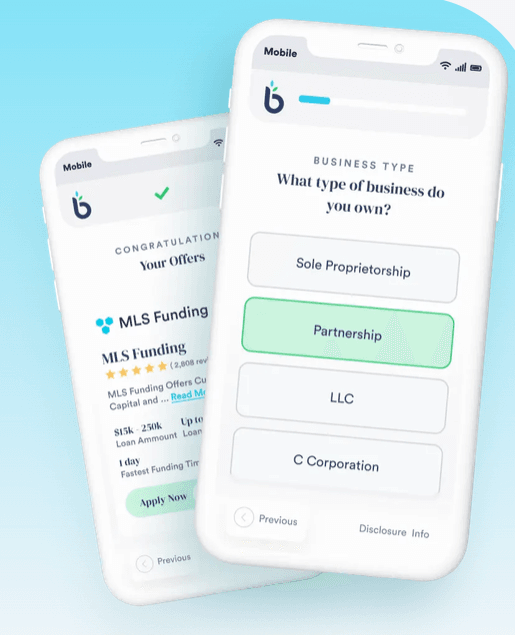

Funding speed and loan terms vary by lending partner. While some partners advertise funding in as little as one business day, others require additional underwriting or a separate application. What sets BusinessLoans.com apart from many competitors we’ve reviewed is its guided self-service experience. During our testing, we were able to complete a short questionnaire, receive multiple financing recommendations and choose which lenders to pursue without speaking to a representative.

BusinessLoans.com stands out by giving business owners a straightforward way to compare financing options without relying on a loan specialist. During our testing, we completed a guided application that asked about our business, funding needs, annual revenue and credit profile before presenting multiple lending offers. The process took only a few minutes and didn’t require speaking with a representative.

We also liked that the platform puts borrowers in control. After reviewing the available offers, we could decide which lender to pursue based on factors such as funding speed, loan amounts and repayment terms. Depending on the lender, selecting an offer either directed us to the lender’s application or continued the application process through one of BusinessLoans.com’s marketplace partners.

Although the experience is designed to be self-service, borrowers who have questions or need help with documentation can still contact a BusinessLoans.com representative for assistance. That combination of a guided online experience and optional human support is why we selected BusinessLoans.com as the best business loan and financing option for a self-service experience.

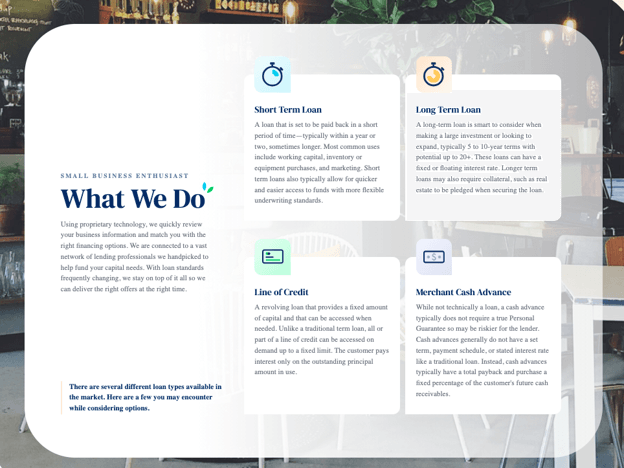

BusinessLoans.com matches borrowers with several financing products through its network of lending partners. Depending on your business profile and funding needs, you may qualify for term loans, business lines of credit, merchant cash advances, equipment financing, invoice factoring and other financing solutions. Because BusinessLoans.com is a marketplace rather than a direct lender, loan amounts, repayment terms, rates and eligibility requirements vary by lender.

BusinessLoans.com’s lending partners offer both short- and long-term small business loans. Term loans are a popular financing option for business owners who need a lump sum to expand their business, purchase equipment, refinance debt or cover other major expenses. Unlike a business line of credit, term loans provide the full loan amount upfront and are repaid through regular installments over a set repayment period.

During our review, we found partner loan repayment terms ranging from as little as three months to as long as five years, with longer repayment periods available for certain financing products, such as commercial real estate loans. BusinessLoans.com advertises annualized rates starting at 9 percent, although your rate ultimately depends on the lender, your credit profile and your business’s financials.

Every lender sets its own qualification standards, so your results will depend on who you’re matched with. As a general rule, businesses have the strongest chance of qualifying if they’ve been operating for at least six months, generate $100,000 or more in annual revenue and have solid credit. Some lenders do accept scores as low as 500, though borrowers with stronger business credit profiles generally receive more competitive offers.

BusinessLoans.com’s lending network includes merchant cash advances (MCAs), which provide upfront funding in exchange for a percentage of your future credit card or debit card sales. Businesses often use this type of financing to cover short-term needs, such as purchasing inventory, launching a marketing campaign or managing seasonal cash flow.

Unlike a traditional business loan, a merchant cash advance is repaid automatically through an agreed-upon percentage of your daily or weekly card receipts. That means payments rise and fall with your sales volume rather than following a fixed monthly schedule.

Merchant cash advances can often be approved more quickly than traditional business loans, making them a useful option when your business needs fast access to working capital. However, that convenience usually comes with higher borrowing costs. BusinessLoans.com’s guide notes that borrowers may repay 20 percent to 40 percent or more above the amount advanced, depending on the factor rate and other terms. Because of the higher cost, merchant cash advances are generally best reserved for short-term financing needs rather than long-term borrowing.

BusinessLoans.com’s lending network also includes invoice factoring, which isn’t a traditional loan. Instead, a financing company — known as a factor — purchases some or all of your unpaid invoices and advances a percentage of their value upfront. Once your customer pays the invoice, the factor sends you the remaining balance minus its fees.

Invoice factoring can be a good option for businesses with reliable customers but slow-paying invoices because it turns outstanding receivables into working capital without taking on traditional debt. BusinessLoans.com’s guide notes that businesses typically receive 85 percent to 95 percent of an invoice’s value upfront, with factoring fees generally ranging from 2 percent to 4.5 percent of the invoice amount.

Because repayment comes from invoices you’ve already issued rather than future sales, invoice factoring differs from both traditional business loans and merchant cash advances. However, your customers will usually make payments directly to the factoring company instead of your business.

Working capital loans help businesses cover everyday operating expenses and other short-term funding needs. Through BusinessLoans.com’s lending marketplace, you may be matched with lenders offering working capital financing for payroll, inventory purchases, rent, utilities, debt payments and other routine business expenses.

Unlike a merchant cash advance or invoice factoring, a working capital loan is a traditional loan with set repayment terms. You’ll know what your payments are ahead of time, and you won’t be giving up a percentage of your future sales or unpaid invoices.

A business line of credit gives you access to a set amount of funding that you can draw from whenever you need it. Unlike a term loan, you borrow only what you need and generally pay interest only on the amount you’ve used. As you repay the balance, those funds become available to borrow again. Business lines of credit are commonly used for short-term expenses, such as managing cash flow, covering payroll or purchasing inventory. BusinessLoans.com notes that many line-of-credit lenders in its network charge an annual maintenance fee of $150 after the first year, so be sure to factor any ongoing fees into your comparison.

Equipment financing helps businesses purchase the tools and equipment they need without paying the full cost upfront. You can finance almost any tangible business asset, including machinery, computer hardware, appliances, office furniture and specialized equipment. The equipment itself typically serves as collateral for the loan, which may make these loans easier to qualify for than some other financing options. BusinessLoans.com says interest rates generally range from 8 percent to 25 percent, depending on the lender and borrower, and many equipment loans require a down payment of 10 percent to 20 percent.

BusinessLoans.com isn’t a lender, so the loan terms you’ll receive depend on the lender you choose and your business’s qualifications. Through its marketplace, you can compare funding options with different loan amounts, repayment terms and interest rates to find one that fits your business’s needs and budget.

Keep these additional factors in mind when shopping for a loan through BusinessLoans.com’s self-service platform.

Although BusinessLoans.com’s platform is designed to match borrowers with lenders through a self-service application, borrowers can contact a funding specialist if they have questions after reviewing their financing options. We like that the company balances the convenience of an automated marketplace with the option to speak with a funding specialist when questions arise.

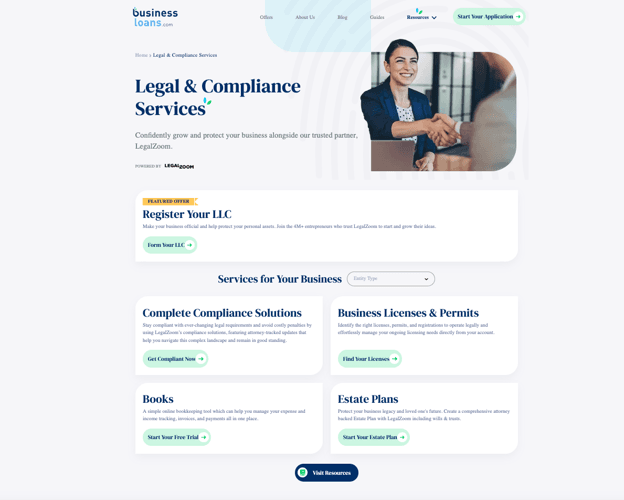

Beyond the application process, BusinessLoans.com offers an extensive online resource center with articles about business financing, loan guides, frequently asked questions and legal and compliance resources through its partnership with LegalZoom. The company’s online educational content makes it easy to learn about financing options before applying.

BusinessLoans.com has been accredited by the Better Business Bureau since 2022 and maintains an A rating. It also holds a Trustpilot rating of 4.8 out of 5 stars based on more than 1,000 reviews.

BusinessLoans.com offers an easy way to compare financing options from multiple lenders, but its marketplace model also comes with a few tradeoffs. Because lending requirements, funding timelines and loan terms vary by provider, it’s important to review each offer carefully before making a decision.

We reviewed business lenders across multiple financing categories to identify the best options for small businesses. As part of our research, we evaluated dozens of loan providers and lending marketplaces, comparing their loan types, eligibility requirements, minimum revenue thresholds, time-in-business requirements, funding speeds and customer support options.

We also compared key financial factors, including starting interest rates, loan amounts and repayment terms. To identify the best lender for business owners who prefer a self-service experience, we assessed each platform’s online application process, loan-matching technology, mobile accessibility and the variety of financing products available.

We recommend BusinessLoans.com for …

We don’t recommend BusinessLoans.com for …