Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Before shopping for the best small business loans, you’ll need to know how to prepare your application so you’ll be approved.

Getting a small business loan means understanding the application process and doing your part to provide lenders with everything they need to make a decision. To improve your chances of securing the best small business loans, gather your financial statements and other supporting documentation before you apply. This guide is designed to help you understand the process and maximize your chances of approval, as well as what you can do if your application is rejected.

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

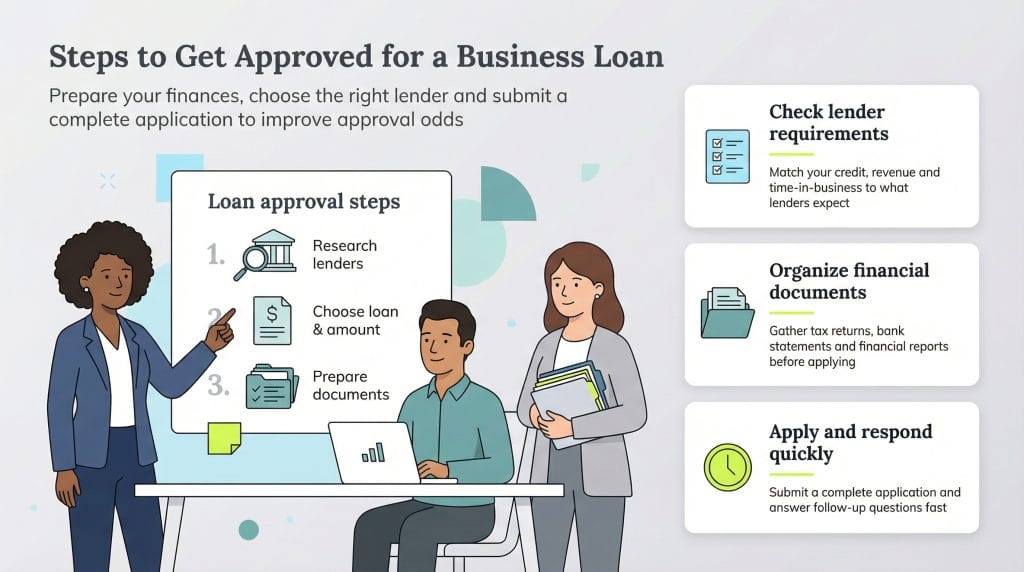

Before applying for a business loan, you must go beyond finding lenders with favorable interest rates and terms. You must work with lenders that are likely to approve your application. You don’t want to go through this process and pay application fees only to discover that you’re not a suitable candidate for a particular lender. For example, if you’re in a specific industry or have subpar credit, you may need a lender that provides high-risk business loans.

Some lenders will also provide more support during the process, while others leave applicants essentially on their own. Look for a lender that’s willing to work with you to help the process go as smoothly as possible.

“I can only imagine how overwhelming it is. The bank’s process needs to help people through it,” said Nate Marshall, SVP and Regional Market Executive at Civista Bank. “It varies [from lender to lender] from zero help and support to high levels of support. It depends on the institution.”

Many different kinds of business loans exist, including the following:

You’ll need to decide which loan type is best for your needs and circumstances and how much money you can afford to borrow. (We’ll dive deeper into the various types of business loans later in this article.)

Every lender has minimum business loan qualification requirements. Usually, these include a minimum credit score, average revenue and time in business. Every lender has its own requirements and risk tolerance, but this table offers a rough estimate of what you can expect these minimum requirements to be based on the type of loan you’re seeking.

| Loan Type | Min. Credit Score | Min. Time in Business | Min. Annual Revenue |

|---|---|---|---|

| Bank term loan | 680+ | 2 years | ~$250,000 |

| SBA 7(a) loan | 650+ | 2 years | Varies |

| Online lender | 500 – 600 | 6 months | ~$100,000 |

| SBA Microloan | 500+ | Startup eligible | None required |

| MCA | 500+ | 3 months | ~$10,000 per month |

When considering a lender, understand all its qualification requirements. If you don’t qualify for any reason, look for a lender with requirements you do meet. You can still get a loan with bad credit or low revenue from some lenders, though the cost of capital may be higher as a result.

Lenders won’t just take your word for it that you meet their minimum requirements. Before you can get a loan, they’ll require ample documentation from loan applicants to assess their lending risk.

“To apply for a conventional small business loan, you’ll first need to share all of your financial details, including your personal financial information, your future growth plans and precisely how you’ll use the requested capital,” explained Farhan Ahmad, group chief executive officer for PayNet.

Ensure you have all necessary documents in hand, including the following:

If you’re applying for an SBA loan, you will also need the following:

“Some applications will require even more information,” Ahmad noted. “Generally speaking, low-cost, long-term loans have more paperwork than high-cost, short-term ones.”

Having all this information on hand will ensure you can provide the lender with everything it needs. Your thoroughness can shorten the loan application process and give you a better chance of approval.

After researching lending options for which you qualify, deciding on a specific loan type and gathering your documentation, it’s time to apply for your top choice loan. Complete the application accurately, thoroughly and to the best of your knowledge.

The lender may contact you after you apply to ask you follow-up questions. Answer promptly and send any additional documentation it requests.

Lenders vary widely when it comes to business loan approval wait times. They must examine your financial statements, including your annual revenue, tax returns and existing loan balances, to determine whether your business can support new debt. They will also consider your credit history and ensure you meet their minimum credit score, a threshold that varies by lender. All of this can take some time.

“If you’re applying through a bank, you’ll then need to pay the application fee and wait for a period of two to four weeks to see if you’ve been approved,” Ahmad explained. Some loans can take 90 days or longer.

If the loan is approved, you’ll receive your funding.

The lender may contact you to pinpoint problems with your loan application as it currently stands. For example, it might say you must reduce your current debt load, improve your credit score or have more cash in the bank to be considered.

Addressing and fixing these issues to qualify for the loan will likely take time. You can either resolve the issues and reapply, apply with another lender with less stringent requirements or pursue alternative funding sources, such as applying for a business credit card or pursuing credit card receivables financing.

If you aren’t able to get approved for a business loan, you can work to try to improve your financial or credit situation or consider alternative funding. Here are the steps to take if you are turned down for a loan.

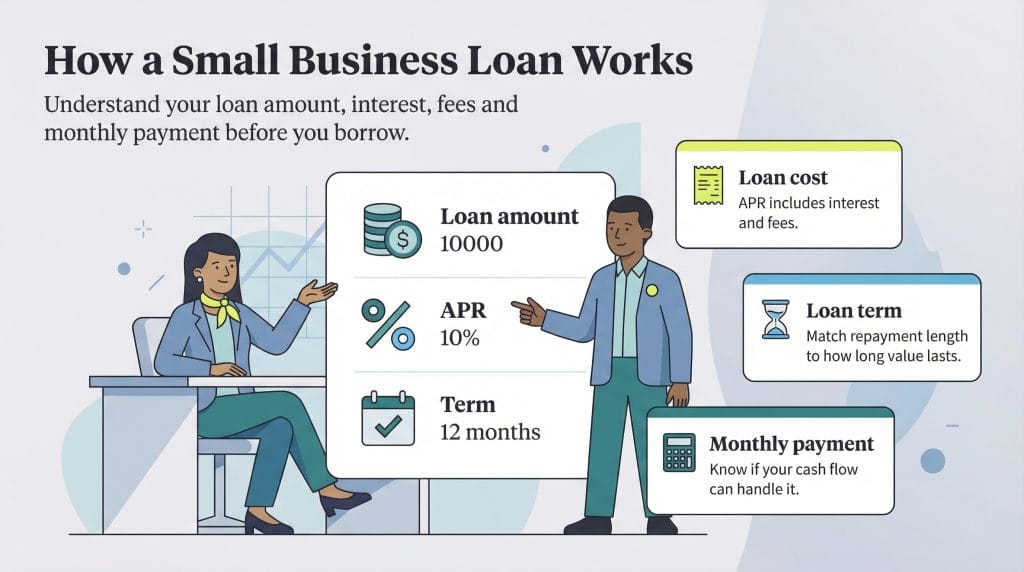

While small business loans vary in application processes and specifics, typical term loans (loans with a specific repayment schedule) all involve costs, terms and a loan structure.

Small business loan costs include the following:

Small business loan terms vary by lender. Some offer only short-term loans of no more than 24 months while others will let you repay loans for many years. When determining which loan is right for you, consider why you are borrowing the money and how far in the future the payback is. You don’t want to end up repaying a loan on something that lost its value long ago.

In our review of Fora Financial, we explain why this lender is a good option for short-term loans. Borrowers may do better with an SBA loan if they want to repay it over an extended period.

Here’s an example of the structure of a typical small business term loan:

This is a highly simplified example of a small business loan, but the general structure applies to all term loans.

Choosing the right type of business loan is critical for your business’s long-term viability. Any loan you accept should have reasonable fees and repayment terms you can handle.

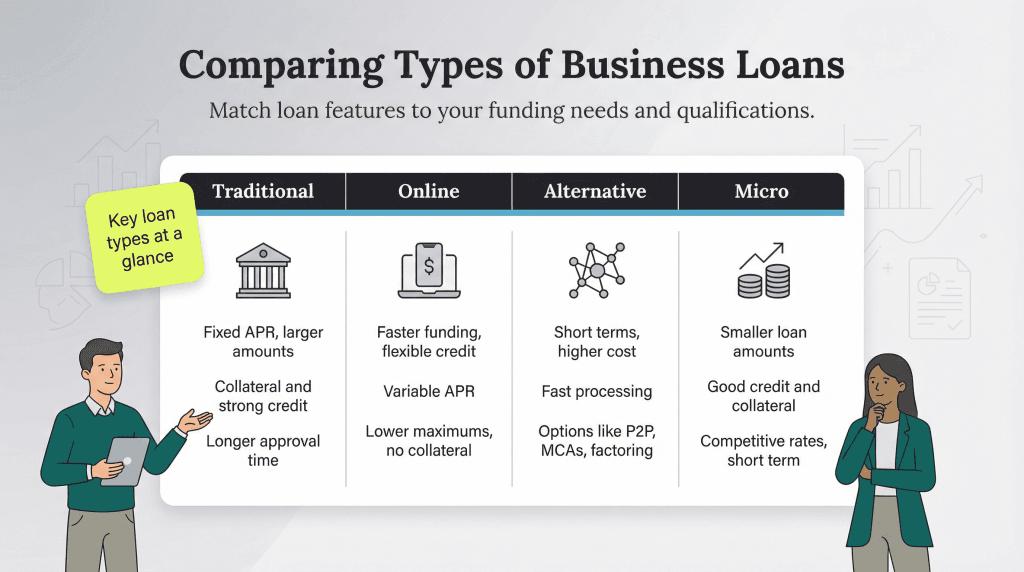

Here’s a breakdown of popular business loan types.

Most organizations look to traditional loans and SBA loans first. If you have good credit and proven assets, these loans provide crucial benefits. Notably, bank loans funded through the SBA have competitive interest rates. According to the SBA, interest rates range from 8% to 15.5%. Generally, SBA loans range in value from $500 to $5.5 million.

The SBA’s 7(a) loan program is a popular option for many businesses. While many small business loans require a personal guarantee from the borrower, the SBA guarantees these loans. With an SBA guarantee, borrowers who would otherwise be denied a loan may be able to secure funding. However, securing funding through the SBA 7(a) loan program takes time and requires solid annual revenue, a good credit score and at least two years in business.

If you can’t get a business loan from a traditional bank or need fast funding, online lenders may be a good option. Online loan companies are ideal for companies searching for quick approval and loan processing. They can also help those with less-than-stellar credit histories.

Standard APRs are likely to be higher than traditional loans, but these lenders may not require collateral. Application processing and approvals are faster with online lenders than with traditional banks, which is crucial if you need to improve cash flow quickly.

Alternative lenders generally provide fast approval and funding but charge higher rates. They also tend to have simple online applications and more latitude regarding application approval. Alternative lenders typically provide short-term loans, meaning you’ll likely have to pay higher installments than you would with a conventional bank loan.

Alternative lending opportunities are growing in popularity and include the following:

Microloans are short-term loans of smaller amounts than traditional loans. Microloans provide a low annual percentage rate (APR), but you must have a solid credit history and collateral. Many types of microloans exist.

According to the SBA, the average microloan amount is around $13,000. The program specifies what the funds can be used for, including supply inventory, working capital, machinery and equipment purchases and rentals and business furniture.

Before applying for a loan, get clarity on how much you need and what these funds will be used for. Loans are essential tools for entrepreneurs, but if they aren’t managed wisely and strategically, they could become an undue financial burden.

Ask yourself the following questions to ensure a small business loan is right for you:

If you need a small business loan and have good personal and business credit scores, thorough financial documentation, a history of strong cash flow and a manageable DTI ratio, you should have little trouble getting approved. However, securing a small business loan might be more challenging for businesses lacking in these areas. Still, with the proper documentation and guarantees, it’s possible.

If you discover that a conventional small business loan is unlikely, consider an alternative lender. However, be mindful that these lenders typically charge much higher rates, so ask yourself if it’s necessary before taking out a loan.

Securing any loan is a matter of demonstrating reliability to the lender. If you can show you can repay your loan with interest in the allotted time frame, your application will likely be approved on the first pass.

Matt Sexton and Jennifer Dublino contributed to this article. Source interviews were conducted for a previous version of this article.