Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Monitor loan industry trends to optimize your funding approval chances with various loan products.

If you need additional capital for your business and want to retain equity, you’ll likely investigate business loans or alternative funding options like a merchant cash advance or business credit card. However, financing trends may dictate your best option at any given time, making a specific funding source a better choice than another.

Understanding business lending trends can inform you of the optimal time to take out a loan, the best loan type for your business and when you should turn to alternative lending sources. In this guide, we’ll outline some current lending options, overall costs and what might impact your chances of funding approval.

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Many types of business loans exist, but all are impacted by overall trends in business lending. Here are a few to watch and what they may mean for your business.

The Federal Reserve cut its benchmark interest rate to 4 to 4.25 percent in September 2025, the first reduction since December 2024. The rise in unemployment and inflation spurred their decision, and they may lower the rates again if the economic outlook justifies it.

According to the Federal Reserve Bank of Kansas City‘s Small Business Lending Survey and the Small Business Administration, the average interest rates for several loan options are as follows:

Type of loan | Fixed-rate APR average | Variable-rate APR average |

|---|---|---|

Bank business loan | 6.7 to 11.5 percent | 7.59 to 7.86 percent |

Online business loan | 9 to 75 percent | |

7.16 to 7.24 percent | 7.76 to 8.08 percent | |

SBA loans | 12.25 percent to 15.25 percent | 3.0 percent and higher |

What this means for lending

Fixed-rate loans offer protection against potential rate increases. However, if the Fed begins cutting rates further as anticipated, variable-rate loans could decrease as well.

Numerous factors contribute to the overall uncertainty in the financial arena. The Consumer Price Index (CPI) increased 2.9 percent in August 2025 compared to a year ago because of rising prices. Additionally, ongoing geopolitical tensions, including conflicts in Eastern Europe and the Middle East, continue to impact global prices for grain and fossil fuels. They also affect global shipping, snarling supply chains. Finally, the uncertainty of the current tariff policy makes it difficult for businesses to plan and set prices, leading to possibly higher prices and less economic development.

What this means for lending

In addition to potentially lowering consumer confidence, the wars and tariffs will likely contribute to higher prices, keeping inflation a factor. When the economy is uncertain, consumers tend to spend less, which means businesses sell less and have less revenue. Lenders respond to this environment by tightening their criteria for loan approval, only lending to those businesses that can prove they’re profitable and cash-rich.

In the past, a business needing a loan would contact its bank and perhaps reach out to a few other large banks. Today, technology helps businesses easily and quickly shop around for the best loans through individual lenders’ websites and loan marketplaces. Businesses can see lenders’ rates and criteria at a glance and are exposed to many more choices, including large banks, alternative lenders and credit unions.

What this means for lending

When businesses have more choices, competition in the market increases. This situation can benefit businesses by keeping interest rates and lending qualifications somewhat in check.

Lenders are increasingly using artificial intelligence (AI) to assess borrowers’ risks instead of relying on humans in their underwriting departments. When dealing with people, it is easier to explain any less-than-optimal business results or ratios; AI does not accept this type of explanation and is unlikely to deviate from an initial decision.

What this means for lending

AI-driven risk assessment will likely prompt faster lending decisions. However, businesses must understand what factors and ratios will be used for these assessments and ensure these factors are optimal before applying for a business loan.

Given the current business lending trends, here’s how to improve your chances of getting approved for a business loan.

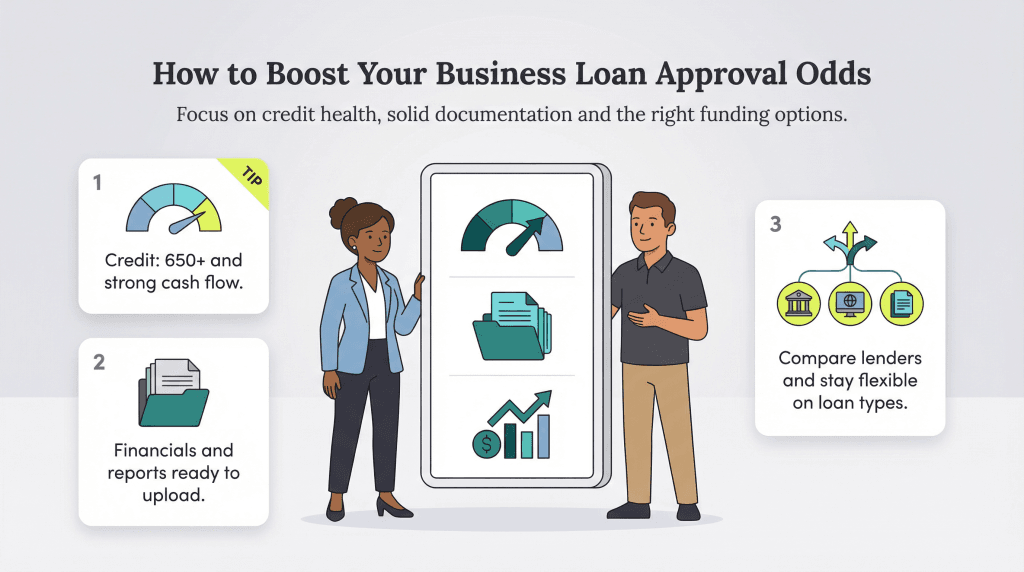

While maintaining business credit scores above 650 remain important, modern consumer lending trends emphasize comprehensive credit health. Review your business credit reports with Dun & Bradstreet (D&B), Experian Business and Equifax Business, and dispute any inaccuracies promptly.

Beyond traditional scores, focus on improving your cash flow consistency and maintaining healthy bank account balances, as many lenders now use bank data aggregation to assess creditworthiness. Aim to keep at least two months of operating expenses in your business accounts when applying for loans.

Lenders want basic information, such as how long you have been in business. However, they may also want to know how you plan to use the money you borrow.

When applying, have your financial statements and tax returns for the last three to five years on hand. Additionally, prepare digital versions of bank statements, accounts receivable reports and a detailed use-of-funds statement. Create a one-page executive summary that clearly articulates your business model, competitive advantages and growth trajectory. If you have plans for a strategic partnership, expansion or acquisition, have any relevant documents available.

To strengthen your company’s financial position, implement low-cost marketing initiatives, such as contests and co-marketing campaigns with complementary companies, to increase revenue. At the same time, ensure you trim waste and reduce operational costs. These measures will result in higher profitability.

There is ample information about business loans available online. Take the time to research your options to learn which loans you are most likely to qualify for based on your credit scores and other criteria. Apply only for loans for which you have a good chance of getting approval. Leverage modern loan comparison platforms that use AI to match your business profile with appropriate lenders. Such platforms analyze your financial metrics against lenders’ actual approval criteria, significantly improving your chances of success.

The evolving landscape of consumer lending trends has introduced innovative funding options that may better suit your business needs. Revenue-based financing (RBF), for instance, has become increasingly popular for businesses with high sales but small assets. When researching potential lenders, look at their years in business, customer ratings and financial stability. If those factors seem optimal, you should seriously consider applying with them.

Under different financial circumstances, you may not have considered options like a variable-rate loan, merchant cash advances or business lines of credit. However, these funding options may be more viable under some conditions than traditional term loans.

If you do all this and still can’t get a business loan, you may want to explore crowdfunding or consider revenue-sharing agreements with strategic partners. The next few years may be challenging for small businesses seeking funding. To obtain capital for growth, they will need to be particularly diligent, discerning and savvy.