Self-funding a business is not for the faint of heart. It can take years to get a company off the ground, so entrepreneurs must get creative with their finances to keep their businesses going.

Despite this challenge, many business owners have found success using self-funding. Here are the steps you can take to self-fund your business, along with tips to help you along the way.

How to self-fund your business

Self-funding a business is more complex than going through a bank or venture capitalists. Here are four steps for securing enough funds to start your business. [Read related: You Can Do It: How to Start a Business Without a Loan]

1. Set up a business bank account.

The first step in self-funding your business is to open a separate bank account, typically a business checking account. Separating your personal funds from your business funds protects your assets, especially if you’re using your personal funds to fund your business. This separation is crucial for maintaining clear financial records and can simplify tax filing, allowing accurate documentation of business expenses and income.

There are several

business checking account options, but look for an account that enables online bill pay, doesn’t require a minimum balance and won’t charge for overdrafts.

2. Analyze your potential sources of funding.

Once your business checking account is open, consider your potential sources of funds to help finance your business. While there are several options to pursue, each carries certain risks because you’re relying on your personal assets to fund your company. If you’re having trouble deciding which funding option is best, create a list of the pros and cons to objectively assess the potential benefits and liabilities of each one.

Here are some possible funding sources:

- Personal savings and investments: Before you look into potential funding options for your business, review your personal finances, including your checking and savings accounts, to see how much you can contribute directly to your business. Consider liquidating non-retirement investment accounts if needed, but be aware of potential capital gains taxes.

- Rollover for business startups (ROBS): ROBS is an option that allows you to take funds from your retirement savings account — without the typical taxes and penalties associated with an early withdrawal — to finance your business. However, this strategy requires establishing a C-corporation and implementing a qualified retirement plan, which can cost $5,000 or more in setup fees.

- Friends and family: Once you’ve reviewed your assets, ask your closest friends and family whether they’d be willing to financially support your business as a gift, for an equitable stake in the company or as a loan with flexible repayment terms. Always formalize these arrangements with written agreements to prevent misunderstandings and protect relationships.

- Bootstrapping: Bootstrapping means reinvesting your earned revenue into the business to continue expanding your company. Many entrepreneurs opt to bootstrap rather than seek funding from an external source, since it allows them to retain complete control of the business.

- Crowdfunding: There are two ways to crowdfund your business: ask for cash from general backers or earn the funds through product presales. Offering product presales is the more common method because funders are rewarded for their contributions with a bonus gift or discount in addition to being one of the first to receive your product(s).

3. Transfer your personal funds.

If you’re transferring personal funds to finance your business, you can classify those transactions as either a loan or equity in the company. Make sure you correctly categorize and track these transactions to ensure accurate tax records.

4. Accurately record the transaction.

When you’re funding your own business, especially if you’re dipping into your personal accounts, use accounting software to document your transactions consistently. This ensures that you record all of your business expenses for tax purposes and that you understand the fundamentals of your business’s finances. That includes managing all incoming and outgoing payments and knowing your company’s monthly expenses.

Pros and cons of self-funding your business

The right financing strategy for your business depends on your situation and needs. Here are some of the benefits and drawbacks of self-funding a business.

Pros

These are some of the benefits entrepreneurs who self-fund their business can expect:

- More autonomy in decision-making: Self-funding keeps business owners in control of all decision-making. It provides the flexibility to run your business how you want to, without having to follow the direction of investors or ask for approval.

- The ability to maintain company ownership: Entrepreneurs who self-fund without selling equity or sharing ownership have complete control over their company. This gives you total autonomy, as you alone are sustaining the business financially.

- Potentially higher profits: Self-funding a business means you don’t have to share your profits with an external entity, so your business can earn fas

Cons

Self-funding your business has downsides, too. Consider these drawbacks before you commit to this financing strategy:

- Increased financial risk: When self-funding a business, entrepreneurs are personally liable for any unpaid debts or losses. According to the S. Bureau of Labor Statistics, approximately 20 percent of new businesses fail within their first year, and about 50 percent fail within five years, making personal financial loss a possibility.

- Limited capital: Self-funded businesses often rely on personal assets for financing, which means there’s less money available to invest.

- Reduced growth potential: Without external financial assistance, businesses may struggle to meet market demands, scale or capitalize on growth opportunities that require significant resources or expertise.

Investors contribute more than just financial capital; they also bring valuable experience and knowledge that can help your business avoid costly mistakes.

Tips for self-funding your business

If you’re ready to self-fund your business, here are some tips to get you started.

Pay as few people as possible in the beginning.

The first thing that prevents young businesses from dying on the vine is doing as much work on your own as possible in the early stages. The fewer people you have to pay, the more easily you’ll minimize your startup costs. If there is crucial work you can’t do yourself, get creative. For example, if you need a developer to design software, consider asking a developer you trust to co-own the business rather than paying them directly for their services.

Maintain outside income.

Most self-funded entrepreneurs will tell you it takes years of hard work for your business to become profitable. However, many people don’t realize that it can take months — or years, depending on the industry — even to generate revenue.

During your business’s early stages, maintain additional income streams to fund your company. While going all in may give you more time to develop the business and make it profitable, you’ll likely burn through your savings before that happens. For many businesses, it takes years before owners transition to working full time at the company, and that’s OK. Consider freelancing, consulting or part-time work in your field to maintain cash flow while building your business.

Be flexible.

Juggling a full-time job while running a fledgling business is no easy feat. However, until you can devote all your time and energy to your company, it’s vital to manage your time carefully and wisely.

If you reach a point where your business starts to interfere with your full-time job, look for creative solutions that will allow you to devote more time to your company. In some cases, you can negotiate a more suitable arrangement with your employer, such as working remotely or becoming an independent contractor.

Pay your bills.

You’ll be amazed by how quickly money disappears when you start a business. Many self-funded entrepreneurs take out credit cards or refinance their houses until their business is profitable.

Always pay your bills on time to give your business the best chance of becoming profitable. Responsibly managing your debts will help you maintain a good credit score and develop positive relationships with banks, thereby opening opportunities for you and your company. Chances are, you will have to sacrifice some luxuries to pay monthly minimums and the mortgage, but failure to pay bills can devastate a young business. Set up automatic payments and maintain a cash reserve equal to at least three months of operating expenses to avoid missed payments during lean periods.

Get as much credit as you can.

Consider asking the bank to increase the credit lines on your cards when you’re starting out. Business credit cards often offer higher limits than personal cards and can provide valuable rewards and cash back on business purchases. You may even want to refinance or take out equity on your home, especially if you qualify for a low interest rate.

When you switch from a full-time job to self-employment, your income may drop significantly or even go negative. If you apply for a new loan or open new lines of credit that accrue debt, your credit score will inevitably dip. When this happens and you can’t make the minimum payments, the new banks won’t be as open to working with you or your business.

Find happiness in the little victories.

If you decide to self-fund, your journey will almost certainly be longer than if you got help from a venture capitalist. That’s why it’s important to savor the small victories during your company’s infancy. Enjoy onboarding your first client, receiving your first check and the day your books finally turn from red to black. These moments will keep you motivated to push through setbacks and doubts. Consider keeping a journal to document these milestones — it can provide valuable motivation during harder times.

Be patient.

You will have to make sacrifices to self-fund your business. In extreme cases, some entrepreneurs put most of their home’s equity into the business and accrue debt on a dozen credit cards. As a result, you may have doubts and frustrations. It’s important to be patient. Most self-funded business owners will tell you the early days of their business were the most difficult times of their lives but it was worth it.

Self-funding your business can affect your personal life, especially at the start. Consider any lifestyle changes you’ll need to make, as well as the potential strain on your relationships and well-being.

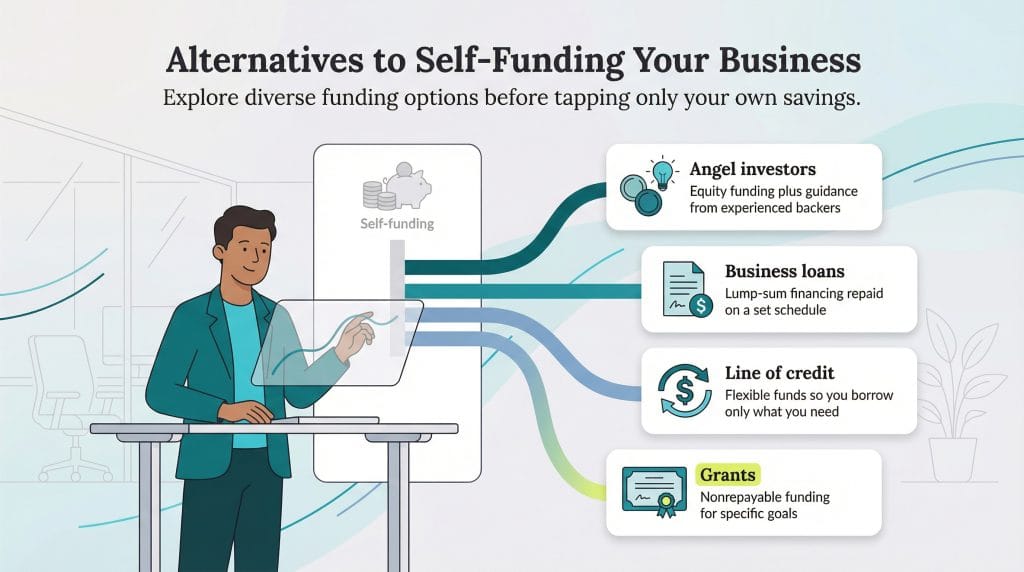

Alternatives to self-funding your business

Self-funding isn’t the only financing option you have as an entrepreneur. Here are some alternatives to consider.

Angel investors

If you’re willing to part with some equity, angel investors can provide the financing and expertise your business needs. These investors use their own money to invest in organizations they believe in, bypassing banks and intermediaries. This poses less risk to entrepreneurs, particularly regarding repayment, but business owners must meet investors’ requirements and expectations.

Business loans

Business loans are a common financing strategy for small businesses, offering a lump sum that must be repaid after a set period. Research lenders to find the right financing option for you, as different types of loans are available. These include traditional and Small Business Administration loans, each of which caters to specific organizational needs. SBA loans, while requiring more documentation, typically offer lower interest rates and longer repayment terms than conventional business loans.

Business line of credit

Unlike lump-sum business loans, business lines of credit allow you to access a fixed amount of funding as you need it, accruing interest only on the amount withdrawn. You can borrow funds during the draw period, which usually lasts two to five years. After that, you’ll repay the amount in full, plus interest and fees, during the repayment period.

Grants

Both government and private entities offer grants, a type of funding that doesn’t need to be repaid. These grants are typically awarded for specific purposes, such as expanding the business or achieving a particular goal. Grants often require an extensive application process, and businesses must meet specific eligibility criteria.

If your ultimate goal is to sell your business for a profit, self-funding probably isn’t the right option for you. On the other hand, if you want to own your business — with all the challenges and successes that entails — then self-funding might be the way to go.

Dan Roberge contributed to the reporting and writing in this article.