Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

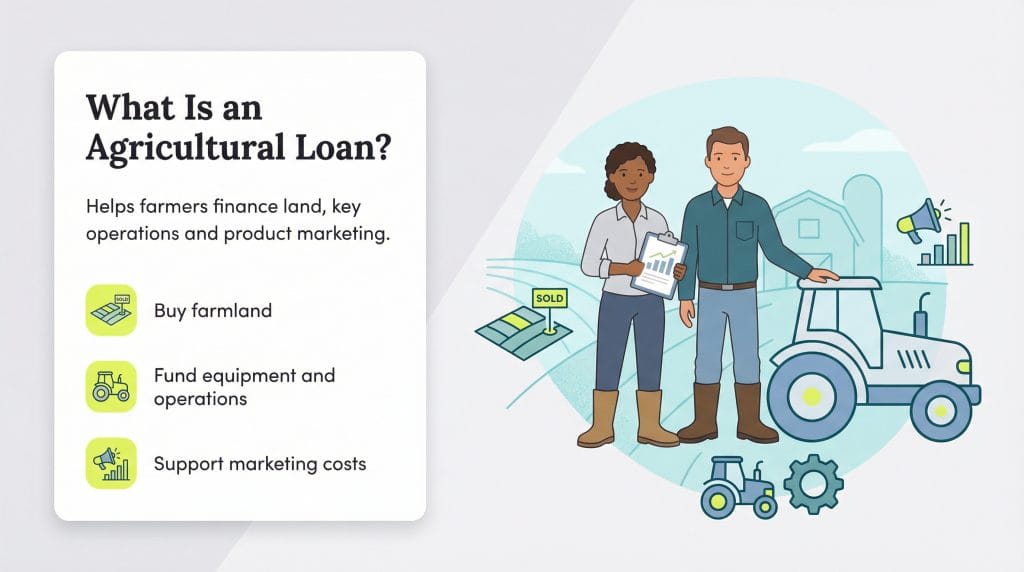

Start or expand a farm with agricultural land financing. Here’s how to get started.

Running a farm isn’t cheap. From buying land and equipment to managing seasonal cash flow, agricultural operations face unique financial pressures. For this reason, many farmers turn to agricultural loans. Agricultural loans provide the capacity to purchase a new farm or expand current operations. Farm loans are available through traditional lenders and dedicated government agencies. Your experience and credit score will play a vital role in whether you are approved for a farm loan.

We’ll explain more about agricultural loans and explore how to qualify and apply for this type of financial assistance.

An agricultural loan is a funding option designed to help farmers and ranchers run their operations more efficiently. Managing the costs of running farms and ranches can be uniquely challenging, so farmers often need low-interest agricultural loans to help them stay afloat. The government often steps in with low-interest loans and other subsidies that help farmers turn a profit.

Approved borrowers can use agricultural loans to do the following:

To qualify for an agricultural loan, you’ll need to take the following steps:

Every lending institution has distinct requirements to qualify for any specific loan program. One of the first things a lender looks at is your current business credit score. Most agricultural lenders require a minimum credit score of 680, though some specialized farm credit institutions may accept scores as low as 640 for already established farming operations. The lender may also ask for a business plan before considering you for an agricultural loan.

The Farm Service Agency (FSA) has dedicated officers to review applications for agricultural loans. The officer reviews the applicant’s eligibility based on what type of loan they want. For instance, those who wish to apply for a farm ownership loan must have a minimum of three years of business operations experience on a farm or ranch.

Similarly, those seeking a farm operating loan must meet the FSA’s education, on-the-job training or farming experience requirements. Beginner farmer loans ask that the farmer or rancher have less than 10 years of farm operation experience.

Agricultural loans aren’t a monolith, and the above loan types are only a small piece of the pie. FSA loans are also available for those who require assistance with only a down payment for a new farm. In this case, the applicant must be able to produce a cash payment of at least 5 percent of the purchase price.

Agricultural loans are also available for those who currently own a farm and need emergency funding. For example, if the farm is located in a designated disaster county and the farmer has suffered a production loss of at least 30 percent, an emergency loan may be granted.

Farmers have several different places to turn to when in need of an agricultural loan.

While it can be a huge hurdle, you can still get a business loan with bad credit. Consider the following strategies:

Prospective farm owners can search for companies and alternative lenders that lend to those with poor credit. Although good credit earns you better interest rates, lenders still approve those with bad credit, albeit with higher APRs and stringent repayment terms. Once your credit score improves, you could refinance the loan at a lower rate.

Government programs like the FSA are less restrictive about what credit scores they permit from applicants.They will look at your credit score but consider your background in the farming industry too. If you have significant farming experience, you’re more likely to be approved even with a less-than-desirable score.

Another tip for getting approved for a farm loan with bad credit is enlisting a co-signer’s help. If the co-signer has better credit than you, your loan will likely be accepted by the lending agency.

Some lenders will approve you based on your farm’s income instead of your credit score. These lenders will let any farm with income above a specific minimum, which varies by loan provider, borrow money. These loans are often quickly approved, though they may be on the smaller side.

Farming experience can prove more important than your credit score to some lenders. Other factors matter too, such as the business debt you carry, your debt-to-income ratio, your business plan and possession of high-value assets — particularly farm equipment, livestock or land that can serve as collateral. Lenders typically prefer a debt-to-income ratio below 40 percent for agricultural operations. Include these items with your loan application, and you just might get the funding you need.

Kimberlee Leonard contributed to the reporting and writing in this article.