Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Is supply chain finance right for your business, or would invoice factoring suit it better? Here's what you need to know about both types of financing.

As the owner of a growing business, you might consider ways to sustainably finance your company. Two popular options are supply chain finance programs and invoice factoring. Supply chain finance programs allow you to access cash without affecting your credit score, while invoice factoring is a loan-based cash advance. Each option has unique benefits and considerations. We’ll explain more about each alternative lending option to help you determine which is right for your business.

Searching for invoice factoring services and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Supply chain financing is a way for businesses to improve cash flow by working with third-party funders to pay suppliers early. This small business financing tool allows buyers to settle invoices ahead of schedule without affecting their business credit scores or causing suppliers to lose money while keeping supplier relationships strong.

In this arrangement, a third-party funder advances payment to the supplier for outstanding invoices. When the buyer’s payment date arrives, the buyer pays the funder or supplier, depending on who holds the account.

Unlike debt or loans, supply chain financing helps free up capital without adding liabilities. While third-party funders may charge a fee for each transaction, this is not an asset-based lending program.

Invoice factoring is a type of small business loan that allows companies to immediately access the money they’re owed from outstanding invoices. The business, typically a supplier instead of a buyer, works with a third-party lender that purchases the outstanding accounts receivable (A/R).

Unlike supply chain financing, invoice factoring is an asset-based lending program that uses a company’s A/R as collateral. In fact, some of the best business loan and financing options can help you with invoice factoring.

“Invoice factoring is the sale of a business’s outstanding accounts receivable to a third-party lender for a discounted rate,” explained Jim Pendergast, senior vice president and general manager at altLINE by The Southern Bank. “This essentially means that a factoring company will buy an invoice for 95 to 98 percent of its value in exchange for providing the cash to the business upfront. Factoring improves the cash flow of businesses by giving them access to working capital more quickly.”

Invoice factoring can be a quick, easy way to get cash. However, note that factoring companies charge fees for each transaction.

In supply chain financing, a buyer works with a third-party lender to pay a supplier’s invoice early. In contrast, with invoice factoring, a supplier sells its A/R at a discount to a third party — known as a factor — for early payment.

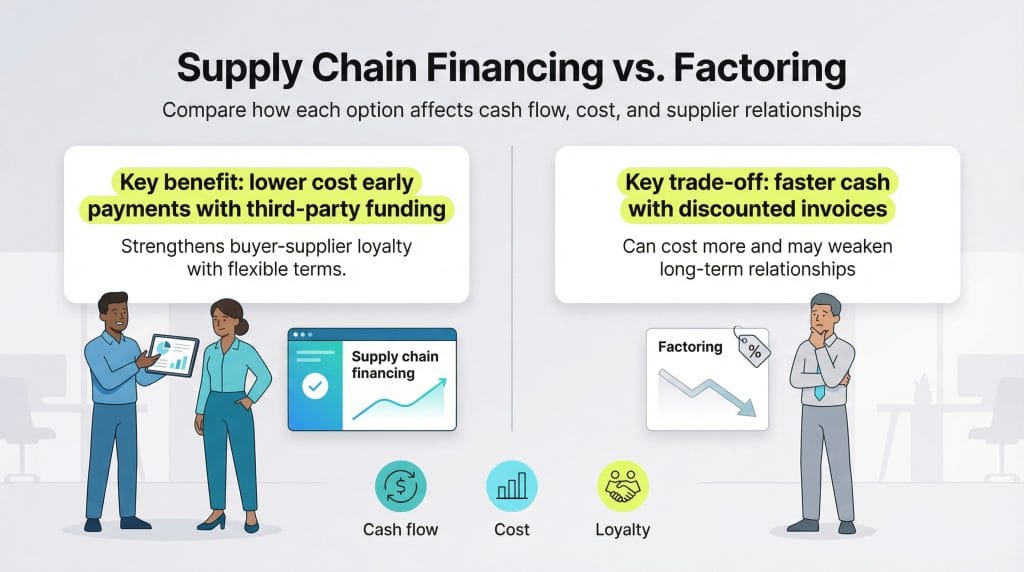

Brandon Spear, CEO of TreviPay, explained that supply chain financing, unlike invoice factoring, is about more than cash flow. “Buyer-seller loyalty hinges on a better payment experience, which is especially important in business-to-business transactions,” Spear explained. “Businesses that deliver a convenient and customizable payment experience for their suppliers can help drive loyalty to grow average order values.”

Spear referenced the results of TreviPay’s November 2023 study of 300 global business buyers to support this assertion. “Flexibility with payment options is so important that 78 percent of global business buyers or suppliers claim it is necessary for merchants to offer invoicing, and 51 percent would switch to a different merchant if it offers flexible net terms,” Spear shared.

The supplier benefits from early payment without the higher fees associated with securing this cash via invoice factoring. Supply chain financing is a new electronic take on the old 2/10 net 30 payment term, but the buyer initiates the request for early payment through the use of technology.

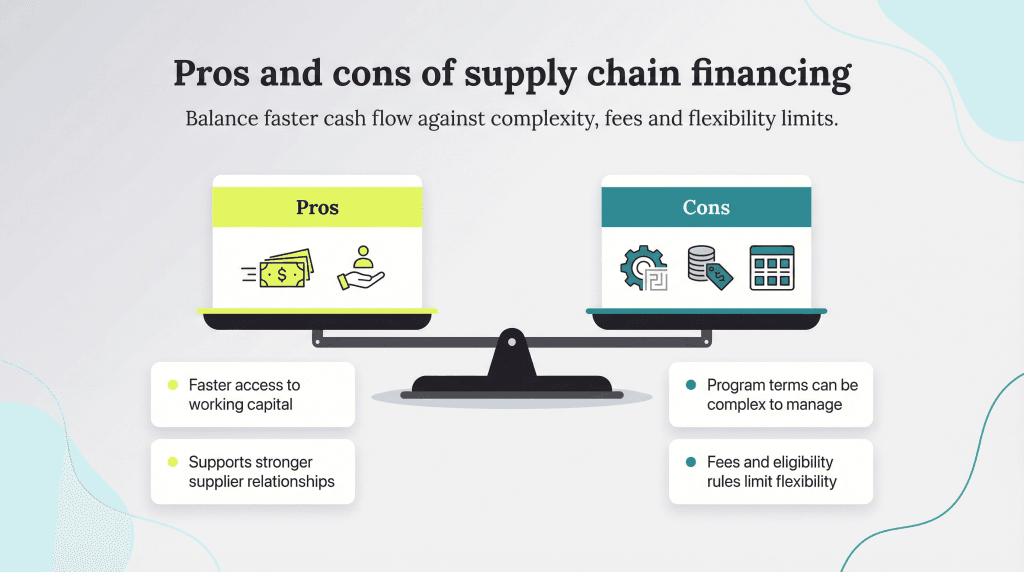

If you’re considering supply chain financing, you should be aware of its advantages and disadvantages.

Invoice factoring also comes with upsides and downsides.

Supply chain financing and invoice factoring serve different purposes and are unlikely to replace one another entirely. Factoring has been around for hundreds of years because it allows smaller suppliers to access cash flow when big buyers delay payments. When a smaller supplier sells to a larger buyer, the buyer often dictates payment terms, regardless of what was agreed upon.

Supply chain financing does not fundamentally change this power dynamic. It is initiated and controlled by the buyer, who determines which suppliers can participate, how quickly payments will be made, and what discounts or terms will be applied to future orders based on the improved buyer-supplier relationship.

Additionally, supply chain financing is not universally available. Some buyers may not have the financial resources, technology or interest to offer this option to all suppliers, often limiting it to their largest or most strategic partners. Even when offered, buyers can withdraw the program at any time due to cash flow issues or shifting priorities, leaving suppliers without a guaranteed solution.

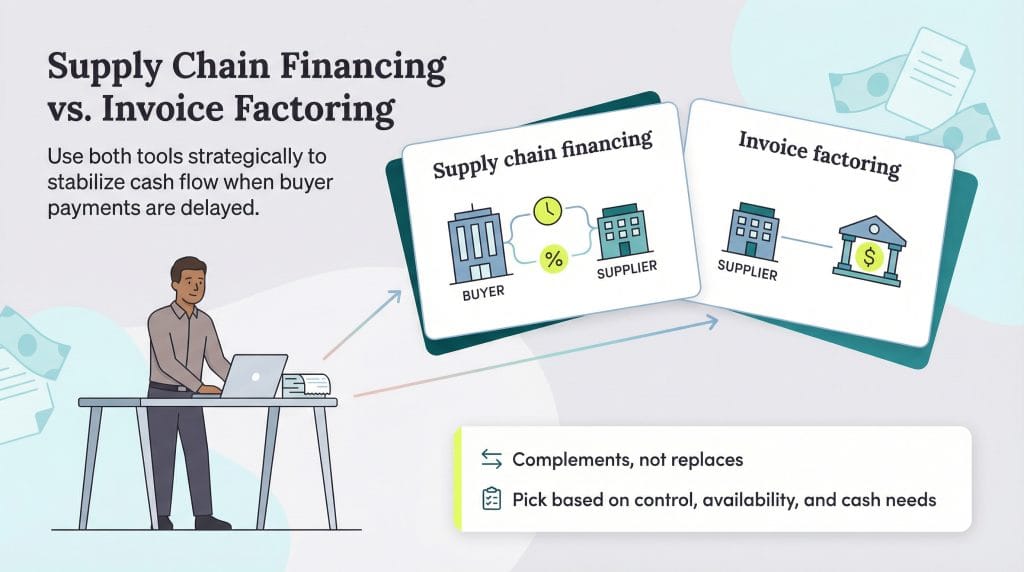

Supply chain financing can complement invoice factoring, but it does not replace it. Suppliers still rely on factoring as an independent method to access cash when buyer payment terms remain unpredictable or unfavorable.

Pendergast noted that it’s not necessarily an either-or when considering supply chain financing versus invoice factoring.

“A supplier can use both factoring and supply chain financing at the same time,” Pendergast explained. “The primary caveat to using both types of lending is that a supplier cannot fund the same invoice through both institutions, and each lender will need to file UCCs [uniform commercial codes] that are limited to the scope of the invoices they plan on financing.”

Supply chain financing can be a great option for a business trying to access cash without immediate debt or penalties. Getting paid earlier means more flexibility for spending, growth and security for your company.

Still, supply chain financing may not be the best option for every business. Some third-party funders may require access to all your receivables, leaving little room for flexibility. As a business, you may not have control over which receivables are used for financing. Additionally, as Pendergast noted, you typically cannot use the same receivables for additional loans since they are already tied to the financing arrangement. Along with third-party funder fees, you may also incur factoring fees for the receivables.

Large corporations offer many supply chain finance programs. Some use their cash to fund the programs, while others have partnered with banks or hedge funds to fund early supplier payments.

If a customer invites you to participate in their supply chain finance program, ask yourself, “Has anything really changed?” What guarantee do you have that supply chain financing will be available for your next invoice or the one after that?

Factoring gives your business more control over cash flow. You determine which invoices you will factor and when to meet your ever-changing cash flow needs. You deal with one factor for all your invoices instead of working with a different program, process and platform for each customer.

Suppliers that need to convert their A/R into cash before the client pays can use either supply chain financing or invoice factoring — but not both for the same invoice. Supply chain financing typically shifts the responsibility of paying the third party to the buyer, whereas invoice factoring places that responsibility on the supplier.

The question, then, may come down to solely whether there’s room in the budget for a third-party payment. And if that’s not a deciding factor, consider all the other pros and cons outlined above instead.

Max Freedman contributed to this article.