Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

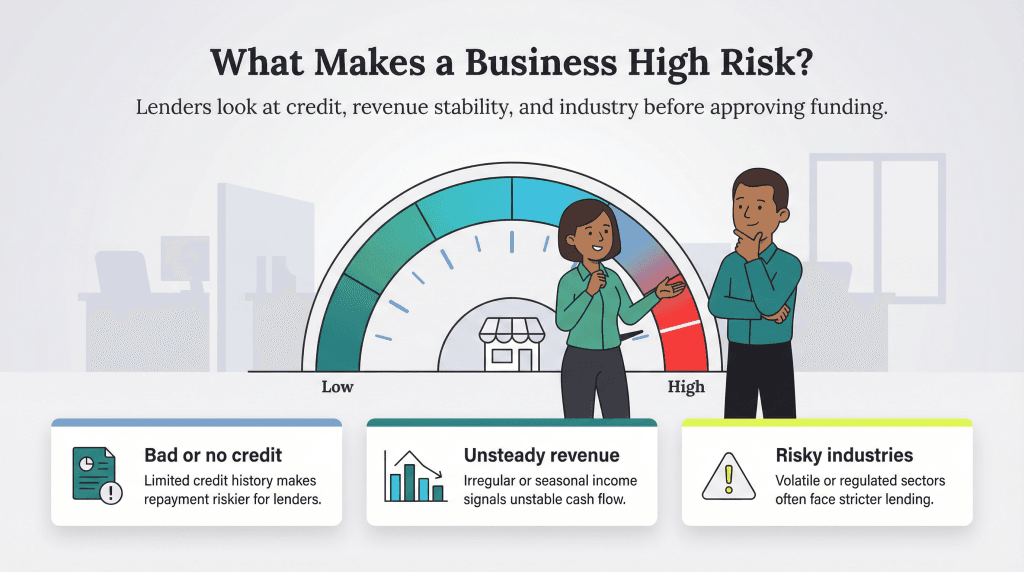

A high-risk business loan is a financing alternative for businesses deemed too risky for conventional loans.

Startups, companies with poor credit, and businesses in nontraditional industries are often left with few places to turn for financing help. While perhaps not ideal, they may be able to secure a high-risk business loan — potentially incurring higher interest rates, stricter repayment guidelines and short-term agreements. We’ll explain more about high-risk business loans, discuss businesses that may be considered high risk and share expert advice for organizations that find themselves in this precarious position.

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

A high-risk business loan is a last-resort financing option for businesses considered too risky by traditional lending standards.

When you apply for a business loan, the lender will analyze your creditworthiness based on the five C’s of credit:

Businesses that fall short in any of these areas are categorized as high risk and will likely find it challenging to obtain a traditional business loan. Instead, they must seek alternative financing.

Neal Salisian, a business attorney and managing partner at Salisian Lee LLP, outlined specific conditions that often constitute a high-risk loan.

“High-risk business loans are ones with high interest rates, large payments or frequent payment requirements,” Salisian explained. “They are short-term, have interest rate hikes at default and are collateralized with important assets or are personally guaranteed.”

In short, high-risk business loans often include one or more of the following factors:

Although the conditions for financing a high-risk business are often similar, several types of loans fall under the alternative lending umbrella. Each comes with its own set of advantages, disadvantages and stipulations.

Here are several high-risk business loans you should know about.

An MCA is not a traditional loan — it’s a cash advance a lender provides based on your business’s past and current sales. You repay the lender by giving up a percentage of your future revenue, typically from credit card receivables, until the advance and fees are paid in full.

To qualify, a small business owner typically needs a personal credit score of 500 or higher, and the business must have been in operation for at least five months and generate annual revenue of $75,000 or more. However, qualifications vary by lender, so it’s important to verify the minimum requirements with each MCA provider.

If your business has outstanding unpaid invoices, you may be able to use them to access working capital. While these two funding options sound similar, there’s a key difference: Invoice factoring involves selling your invoices to a third party while invoice financing uses your invoices as collateral for a loan or line of credit:

Short-term loans are the most traditional type of high-risk loan, typically with a maturity of 18 months or less, according to Zachary Weiner, vice president of finance at Paka Apparel.

“The shorter time frame provides money lenders with an assurance of lesser default risk than conventional loans,” Weiner explained.

You may be able to get a short-term loan from a bank, credit union or alternative lender, such as Fora Financial. (Our Fora Financial review explains more about this lender and its specific requirements.) Typically, business owners need a personal credit score between 560 and 600. Your business must be in operation for at least six months and have a minimum of $50,000 in annual sales revenue — although at least $100,000 in revenue is more commonly accepted.

As long as you follow the set terms, a personal loan can be a good option for a startup with no credit history and limited annual revenue. In this case, the business owner — not the business — takes out the loan personally and is responsible for repayment. You’ll need a strong personal credit score to qualify, and you can apply through a bank, credit union or online lender.

Applying for a business credit card may be a way to secure financing. However, if you have a lower credit score and limited sales revenue and are approved, you may pay higher interest rates than you would with other lending options. Still, there are instances where using a credit card can be a more affordable option, as some offer cash-back features or an introductory 0 percent annual percentage rate. Remember that credit cards can help cover short-term expenses, but carrying a balance over time can become costly.

Subprime loans are generally intended for borrowers with a poor credit score or limited borrowing history. Borrowers who don’t qualify for prime-rate loans will likely need to look elsewhere for financing. Subprime business loans, including equipment financing, can be an option, though the term “subprime” is a bit misleading. These loans often come with higher-than-average interest rates, not lower ones, which is the main risk of taking them out.

When you take out a hard money loan, the loan amount is based on the value of the collateral you provide, often real estate. Typically, the loan is issued for a percentage of the collateral’s appraised value. As such, the asset’s value matters more to hard money lenders than your credit score or borrowing history. The risk is that if you can’t repay the loan quickly, the high interest rates can make it prohibitively expensive.

An asset-based loan is any loan secured by collateral. Hard money loans are a type of asset-based loan, as are most secured loans. This category can include Small Business Administration loans, term loans and lines of credit. Equipment, inventory and invoice financing can also fall under this definition. Whichever asset-based loan you choose, the risk is clear: Failing to repay may result in the seizure of your assets.

The following types of businesses are typically considered high risk by lenders:

High-risk commercial lenders provide money to businesses that can’t secure funding through traditional lending options. By assuming greater risk, they expect a higher return.

Here are some of the key characteristics that define a high-risk commercial lender:

While potentially risky, as the name implies, high-risk loans bring benefits to both borrowers and lenders.

While they come with potential downsides, high-risk loans can offer important advantages — especially for businesses that can’t secure capital through traditional means.

Here are key benefits for borrowers, along with some expert insights:

Lending to high-risk borrowers may seem too risky to be worth the reward. However, when done strategically, high-risk lending can be profitable for lenders.

Potential benefits for lenders include the following:

Because of their cost and risk, the experts we interviewed recommend using high-risk loans only as a last resort. Fortunately, there are several alternative funding options, depending on why you’ve been categorized as high risk.

“Alternatives for high-risk loans include peer-to-peer [P2P] lending, angel investors, external lenders and getting a co-signer for the loan,” Weitz said. “All [are] enticing options that should be vetted during the financing process.”

Here’s a closer look at why these alternatives can be a better choice:

Misheloff added that small business owners can investigate other alternatives, such as supplier (trade) financing, borrowing from friends and family and seeking a personal loan. He said that personal loans are often cheaper than business loans.

How you finance your business is a critical decision that can shape your long-term success. Analyze every option carefully and, once you secure funding, manage your cash flow wisely to reduce future borrowing needs.

Simone Johnson and Sean Peek contributed to this article. Source interviews were conducted for a previous version of this article.