Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Is an Audited Financial Statement?

When you need a loan for your business, potential lenders may ask to see your audited financial statement. Learn what this is and why lenders want to see it before they approve your business loan.

Written by:

Sally Herigstad, Senior Writer

Editor verified:

Shari Weiss,Senior Editor

Last Updated Oct 09, 2025

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

When you apply for business funding, lenders and investors want to ensure they won’t lose money on your venture. That’s why bringing detailed financial statements to your pitch meeting is crucial.

However, if potential stakeholders still have concerns about your company’s finances, it may be because you haven’t prepared an audited financial statement. Below, we’ll explain what an audited financial statement is and how it differs from an unaudited financial statement.

What is an audited financial statement?

An audited financial statement is an independent, objective evaluation of a company’s financial records by a certified public accountant (CPA). When a CPA firm audits financial statements, it ensures the business adheres to Generally Accepted Accounting Principles (GAAP) and professional auditing standards. The audit process provides the highest level of assurance that financial statements accurately reflect a company’s financial position and performance.

Without CPA verification, investors and lenders may question the accuracy of your financial reports. Such trepidation can reduce their confidence in your company’s financial stability.

An audited financial statement includes a detailed examination of these four key financial reports:

Balance sheet: A balance sheet provides a snapshot of your business assets, shareholder equity, liabilities and debts at a specific point in time.

Cash flow statement: A cash flow statement tracks cash and cash equivalents moving in and out of your company’s accounts. Cash equivalents include bank deposits, cash-convertible assets and short-term investments. For this type of statement, cash includes both cash available on hand and money stored in demand deposits. Cash equivalents must have maturities of 90 days or less.

Income statement: An income statement, also known as a profit and loss statement, details your company’s revenue, expenses, and net gain or loss. A balance sheet is a snapshot of your company’s performance at a specific moment in time, but an income statement captures that performance over a period, such as a fiscal year. It includes metrics such as gross profits, net earnings, revenue, expenses, cost of goods sold, taxes and pretax earnings.

Statement of changes in equity: While often included as a portion of the balance sheet, the statement of shareholder equity can also be prepared separately. It details all changes to your company’s value to shareholders or owners during an accounting period, including net income and contributions or withdrawals.

Darian Shimy recommended stringent preparation for this process, including using one of the best accounting software platforms to streamline recordkeeping. “I also suggest engaging a qualified CPA or auditing firm early in the process, as their guidance can prevent issues and simplify the audit,” Shimy, CEO and founder of FutureFund, added.

Did You Know?

An audited financial statement also includes an opinion letter from the CPA who assessed your reliability.

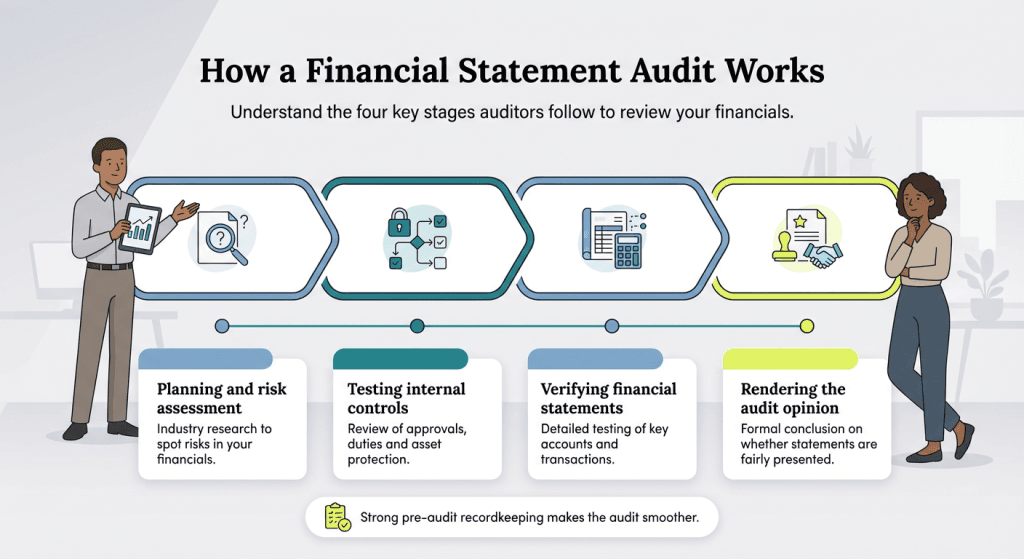

How a financial statement audit works

An audit of financial statements typically follows four key stages: planning and risk assessment, internal control testing, thorough statement verification and rendering an opinion.

Industry research and risk assessment: The auditing CPA begins by gaining a thorough understanding of your business, industry and competitors. This knowledge helps them identify potential risks that could affect the accuracy of your financial statements.

Internal control testing: The CPA will test your company’s internal controls to understand key processes, including employee authorizations, delegation of responsibilities and asset protection. Next, the CPA conducts control procedures. If your business has strong internal controls, a more complex audit may be required. If your controls are weak, the CPA may need to conduct additional financial assessments.

Thorough statement verification: The CPA will perform detailed testing of representative financial elements. For example, let’s say the CPA is verifying your accounts payable. They may reach out to vendors to confirm invoice amounts and cross-check transaction records to ensure accuracy.

Rendering an opinion: After completing the audit, the CPA will issue an opinion on whether your financial statements represent a true and fair view of the company’s financial position. As mentioned earlier, the best possible outcome is an unqualified opinion (full approval), while the worst is an adverse opinion (financial misstatements detected).

Auditors provide different opinions based on their evaluation of an organization’s financial statements, each reflecting varying levels of confidence in the accuracy and fairness of the presented information.

Unqualified opinion

An unqualified opinion, also called a clean opinion, represents the best outcome for any organization. The auditor concludes that financial statements present a true and fair view of the company’s financial position in accordance with applicable accounting standards. This opinion indicates no material misstatements were found, and the company has maintained proper accounting records and followed appropriate procedures throughout the reporting period.

Qualified opinion

A qualified opinion arises when auditors discover specific issues that are material but not pervasive enough to invalidate the entire financial statement. This opinion typically includes an “except for” clause highlighting particular areas of concern. Common reasons include limitations in audit scope, minor departures from accounting standards or insufficient evidence for certain transactions. While less favorable than an unqualified opinion, it suggests most financial information remains reliable.

Adverse opinion

An adverse opinion represents a serious red flag for stakeholders. Auditors issue this opinion when they determine that financial statements contain material misstatements that are both significant and pervasive, fundamentally misrepresenting the organization’s financial health. This opinion indicates widespread problems with accounting practices, suggesting the statements cannot be relied upon for decision-making purposes. Companies receiving adverse opinions often face severe consequences, including loss of investor confidence and potential regulatory action.

Disclaimer of opinion

A disclaimer occurs when auditors cannot form an opinion due to insufficient evidence or significant scope limitations preventing them from completing their examination. Unlike an adverse opinion, this doesn’t necessarily indicate problems exist. Rather, the auditor simply lacks adequate information to make a determination. Common causes include management restrictions on audit procedures or incomplete records.

Tip

Do you expect to receive funding from one of the best business loan and financing options? Then you'll want to obtain an unqualified opinion from your CPA before applying for financing. "Unqualified" in an audit opinion basically means "all clear."

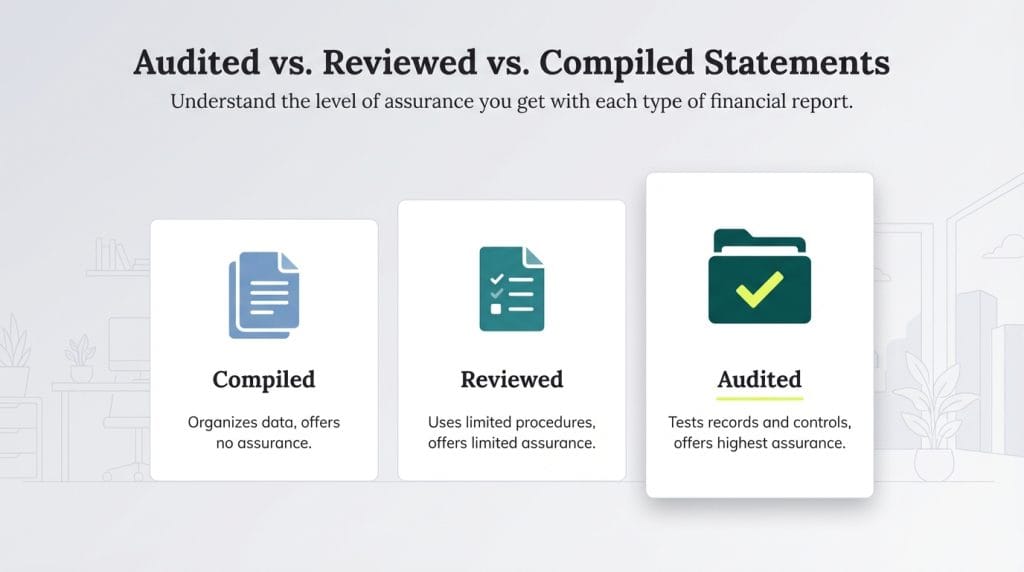

Audited vs. reviewed vs. compiled statements

Audited reports differ from other formal accounting reports, such as compiled reports and reviewed reports. These three types of financial statement services vary significantly in their level of assurance, complexity, cost and appropriate use cases.

Compiled reports: A compiled report, also called a compilation report, is created by organizing financial records into a standard statement format. While this type of report can be helpful for internal reviews, it’s not sufficient for external stakeholders. Compiled reports provide no assurance about the accuracy of financial statements.

Reviewed reports: A reviewed report undergoes a bit more scrutiny than a compiled report but less than an audit. For these reports, an accountant performs limited analytical procedures and submits a small number of inquiries to company management. The accountant verifies GAAP compliance but does not test internal controls. Reviewed reports provide limited assurance.

Audited reports: In contrast to compiled and reviewed reports, audited reports involve a thorough review of items on a financial statement. They also entail internal protocol testing to ensure financial transactions are accurately recorded. An audit provides the highest level of assurance, meaning that in the auditor’s opinion, your financial statements are fully accurate and present a true picture of the company’s financial position and performance.

Bottom Line

The primary differences between audited and unaudited financial statements are a CPA's involvement and an in-depth verification process. However, hiring the right accountant — whether or not they are a CPA — is key to ensuring accurate, reliable financial reporting.

Why audited financial statements matter

Audited financial statements are particularly valuable when applying for a business loan or seeking investor funding. These stakeholders want to ensure they are making a sound financial decision. The type of audit opinion can significantly impact a company’s access to capital, as lenders and investors often rely on audit reports to assess the company’s financial health and risk profile.

Shimy, whose platform helps K-12 schools streamline fundraising and volunteering, emphasized that growing businesses may find value in audited financial statements. “At FutureFund, having clear, audited financials has been key to earning the trust of school districts and demonstrating accountability,” Shimy explained.

Beyond securing financing, a clean audit opinion can enhance the company’s reputation and boost investor confidence, while a qualified, adverse or disclaimer of opinion can raise red flags about the company’s financial health and governance. Audited financials also demonstrate transparency and accountability, which are essential for building trust with regulators and other external stakeholders.

Crystal Stranger, CEO of OpticTax.com, noted that most businesses do not need audited financial statements, especially since audits can cost thousands of dollars. Typically, only companies publicly financed and regulated by the SEC are required to have audited financials.

“However, in certain situations, a set of audited financials can be helpful, such as when seeking a bank loan, during a partnership dissolution, or when executing equity exchanges from financial instruments such as options or SAFE notes,” Stranger explained.

Common scenarios requiring or benefiting from audited financial statements include:

Public companies: All publicly traded companies must comply with SEC regulations requiring annual audited financial statements.

Government contractors: Contractors working with federal agencies may be subject to audit requirements under the Federal Acquisition Regulation (FAR) and Defense Contract Audit Agency (DCAA) standards.

Financing rounds: Venture-backed startups and companies seeking significant investment often need audited financials to satisfy investor due diligence requirements.

Bank loan applications: Many commercial lenders require audited financial statements before approving substantial business loans.

Regulatory compliance: Certain regulated industries such as healthcare, construction and finance may require periodic audits.

Small businesses seeking financing, partnership agreements

Audited

High

CPA conducts full audit, opinion issued

Public firms, SEC compliance, major financing, investor requirements, contracts

FAQs about audited financial statements

Most small businesses do not need audited financial statements unless required by lenders, investors or regulatory bodies. Audits are expensive and primarily necessary for publicly traded companies regulated by the SEC. However, small businesses may choose to obtain audited financials voluntarily when seeking bank loans, major investment rounds or during partnership changes to build credibility with stakeholders.

Audited financial statements often take weeks or even months to complete, depending on the size and complexity of the business. The timeline varies based on factors such as the company's preparedness, the strength of internal controls, transaction volume and industry-specific requirements. Companies with well-organized financial records and strong internal controls typically experience shorter audit timelines.

A financial audit generally costs between $7,000 and $50,000 or more. However, this will depend on key factors such as your company size, industry, revenue, operation complexities and internal controls.

An audit is a formal, structured examination of financial statements conducted by an independent CPA to provide assurance that the statements are accurate and comply with GAAP. Due diligence, on the other hand, is a broader investigative process typically conducted before mergers, acquisitions or major investments. While due diligence may include reviewing audited financial statements, it also examines legal compliance, operational efficiency, market position, intellectual property and potential risks beyond financial reporting. Audits follow standardized procedures defined by professional auditing standards, whereas due diligence processes are customized to each transaction's specific needs.

Max Freedman contributed to this article. Source interviews were conducted for a previous version.

Did you find this content helpful?

Thank you for your feedback!

Share Article:

Written by: Sally Herigstad, Senior Writer

Sally Herigstad is a retired CPA who spent nearly a decade advising on tax and money issues for Microsoft properties, in addition to hemming a financial advice column for CreditCards.com. She is skilled at breaking down complicated tax guidance for both personal finance and business finance audiences and has even helped develop tax software.

At business.com, Herigstad covers accounting topics, particularly those related to taxation.

Herigstad is the author of the book Help! I Can't Pay My Bills: Surviving a Financial Crisis. Her expertise has been featured in U.S. News & World Report, Bankrate, Realtor.com, The Motley Fool and TaxAct, among others.