Small business owners must deal with numerous accounting reports to monitor their business’s finances and ensure its financial health. Profit and loss statements, accounts receivable aging reports and cash flow statements are just a few of the essential documents necessary for planning growth and staying on top of money matters. However, some small business owners may overlook the statement of shareholders’ equity ― part of the balance sheet ― while focusing on money coming into and leaving the organization. That said, income shouldn’t be your only focus if you want a genuine idea of how your operations are faring.

We’ll explain more about the statement of shareholders’ equity and how it fits into your business’s overall financial picture.

What is a statement of shareholders’ equity?

A statement of shareholders’ equity, also called a “statement of stockholders’ equity” or a “statement of owners’ equity,” is a section of a business’s balance sheet that lists the difference between total business assets and total liabilities. It gives shareholders, investors and the company’s owner a true picture of how the business is performing and is usually measured monthly, quarterly or annually.

Stan Gregor, CEO of Summit Financial LLC, emphasized that a statement of shareholders’ equity provides crucial financial accounting information about a business’s value.

“This gives stakeholders a clear understanding of how a company’s equity has been affected by factors like profits, losses, dividends and stock issuances,” Gregor explained. “Statement information is frequently used by analysts and investors to determine a company’s general financial health. For a fast-growing company, maintaining and analyzing this statement regularly is vital.”

The statement of shareholders’ equity may intimidate some small business owners because it’s a bit more complicated than other financial calculations. However, in simplest terms, it’s essentially what your organization has earned that remains in the business.

“The statement of shareholders’ equity tends to be overlooked because people focus on the profit or loss statement or cash flow,” noted Craig M. Steinhoff, a certified public accountant (CPA) and information technology professional with HBK CPAs & Consultants. However, it’s a crucial tool for helping business owners evaluate potential investments and measure their business’s performance and worth.

The statement of shareholders' equity is the part of a balance sheet or ledger that calculates and explains shareholders' equity. It provides crucial

financial accounting information about a business's value.

What is shareholders’ equity?

Shareholders’ equity is what remains after subtracting all liabilities from a company’s assets. Shareholders’ equity can increase in the following situations:

- If business owners or investors contribute more capital.

- If the business’s profits improve as it sells more products.

- If the business increases its margins by cutting business expenses.

For a company with stock shares, stockholders own the equity. Otherwise, business owners or investors own the equity. Shareholders’ equity has several components, each with its own value and meaning:

- Share capital: Share capital is the cash a company raises by issuing stock. In an initial public offering, a set amount of stock is sold for a set price. After that, the stock can be traded freely, but the money paid directly to the company for the initial offering is the share capital.

- Retained earnings: Retained earnings are the money left in a business after the shareholders are paid dividends. With dividend stocks, shareholders are entitled to a percentage of the company’s profits. The company must still calculate how much money it has to work with after making these payments; that calculation is the retained earnings.

- Net income: Net income is the money left after subtracting expenses and deductions from the total profit. In this case, profit is the amount of money made after subtracting the cost of operations.

- Dividends: Dividends are funds paid to shareholders. Investors who own stock in a company own a portion of the business and are entitled to a percentage of the profits. A dividend is the amount of money paid per share of stock. The company sets aside a portion of its profits to pay dividends (that portion is usually outlined in the stock agreement).

When

selling a business, shareholders' equity is the amount distributed to the business's owners after all the company's debts are paid.

Who uses a statement of shareholders’ equity?

Businesses of all sizes use the statement of shareholders’ equity (or owners’ equity if the business isn’t public). Gregor explained that while it’s a necessity for all businesses, how it’s used may differ across business types and sizes.

“It is essential for publicly traded companies, as they are required to disclose their financial statements, including the statement of shareholders’ equity, to their shareholders and the public,” Gregor said. “Private companies can also benefit from using a statement of shareholders’ equity, especially if they have investors or are seeking funding.”

For smaller businesses, a statement of shareholders’ equity also paints a clear picture of your financials.

“If you have more than a sole proprietorship, it’s always a good idea to have a statement of stockholder equity,” advised Meredith Stoddard, former group team lead at Fidelity Investments. “It’s an important document that spells out where the assets and liabilities are and who owns what.”

Why should you use a statement of shareholders’ equity?

In both prosperous and challenging times, small business owners must understand how their business is faring over a specific period. Without a statement of shareholders’ equity, that can be difficult.

A statement of shareholders’ equity is a valuable tool for gauging a business’s health for the following reasons.

1. A statement of shareholders’ equity can help you make financial decisions.

A statement of shareholders’ equity can help you value your business and plan for the future. It can reveal whether you should borrow money to open another business location, cut costs or profit from a sale. It can also help you find and attract investors — who will undoubtedly want to review this statement before injecting capital into your business.

When calculating your

business valuation, disregard capital assets. Instead, focus on gross income and outgoing payments.

2. A statement of shareholders’ equity can tell you how well you’re running your business.

A statement of shareholders’ equity is helpful for gauging how well the business owner is running the organization. Gregor outlined how to gauge business success when reviewing a statement of shareholders’ equity.

“Strong performance is reflected on the statement by a positive and growing shareholders’ equity, a rising return on equity (ROE), and a healthy retained earnings balance,” Gregor explained. “This information shows the company has more assets than liabilities, and that the value of the company’s ownership stake is increasing. A rising ROE indicates that management is effectively using shareholder investments to create value.”

However, if shareholders’ equity declines from one accounting period to the next, it’s a telltale sign that something may be going wrong.

“A decrease in retained earnings, a negative shareholder equity, or a high debt-to-equity ratio all suggest a company is not generating sufficient profits or is relying heavily on debt,” Gregor cautioned. “A low ROE or negative ROE can indicate that the company is not generating sufficient returns for its shareholders.”

3. A statement of shareholders’ equity can help you get through financial difficulties.

The statement of shareholders’ equity is essential in trying times. It can reveal whether your business didn’t generate enough income to sustain operations or whether you have enough equity to weather a downturn. The statement also shows whether you’re likely to get approved for a business loan, whether there’s value in selling the business and whether it makes sense for investors to contribute.

Shareholders' equity can be negative or positive. If it's negative, the company owes more than its total assets. This situation is called balance sheet insolvency and signals that changes must be made.

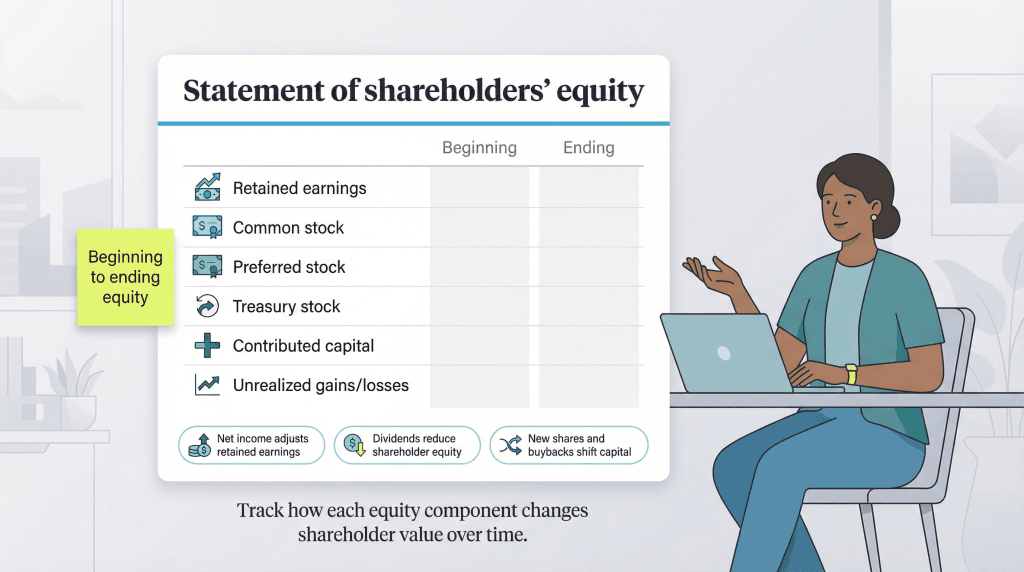

What does the statement of shareholders’ equity include?

Statements of shareholders’ equity vary depending on business size and operational factors. Jason Pack, chief revenue officer at Freedom Debt Relief, explained that most are usually broken down by type of equity, like common stock and retained earnings.

“It starts with the beginning equity balances, then shows the net income or loss for the period, which increases or decreases retained earnings. It also clearly lists any dividends or distributions paid out to shareholders, which reduce retained earnings,” Pack said. “Other common items include adjustments for any new stock issued during the period, increasing contributed capital, or any stock repurchased by the company.”

In general, most statements will include the following:

- Preferred stock: Preferred stock is a share in the company (or an ownership stake) issued as stock or equity. Preferred shareholders are held in higher esteem than common shareholders regarding dividends and asset distribution.

- Common stock: Common stock is also a share in the company, but it takes a back seat to preferred stock when paying out equity. For example, if the business decides to liquidate, preferred shareholders will get paid before common shareholders. However, common shareholders tend to have voting rights while preferred shareholders usually don’t.

- Treasury stock: Treasury stock refers to shares the company buys back, whether to prevent a hostile takeover or drive the stock price higher. This type of stock typically pertains to publicly traded companies.

- Retained earnings: Retained earnings are net profits on the income statement that aren’t paid out to shareholders or used as the owner’s draw. They are reinvested in the business. They can be used to purchase new equipment, invest in research and development or pay down costly debt.

- Contributed capital: Often referred to as additional paid-in capital, contributed capital is the extra amount investors pay for shares over the par value of the business. This additional capital is created when a company issues new shares. It can be reduced when the company buys back its shares.

- Unrealized gains and losses: These are the gains and losses a business sees as a direct result of a change in the value of its investments. Unrealized gains occur when the business has yet to cash in those gains, while unrealized losses are the reductions in value before the investment is unloaded.

Ultimately, the statement provides transparency around how shareholders’ value has changed throughout the reporting period. “It tells shareholders the direct financial impact of the business’s operations and policies on their ownership stake and how their claim of the company’s value has changed,” Pack added.

How do you create a statement of shareholders’ equity?

You’ll structure your statement of shareholders’ equity with four sections that paint a picture of how the business is performing:

- Section One: Beginning equity. The first section shows the business’s equity at the beginning of the accounting period.

- Section Two: New equity infusions. This section lists new investments that shareholders or owners made to the company for the year. Net income is also included in this calculation.

- Section Three: Subtractions. This section subtracts all dividends paid out to investors and any net losses.

- Section Four: Ending equity balance. The final section shows your ending equity balance for the period you’re tracking.

The statement’s heading should include the company name, the statement title, and the accounting period to prevent confusion when reviewing financial statements later.

Business owners can create a statement of shareholders’ equity using Excel, a downloadable template or one of the best accounting software platforms, which will automate much of the work.

Here’s an example of a statement of shareholders’ equity:

Natalie Hamingson and Jennifer Dublino contributed to this article. Some source interviews were conducted for a previous version of this article.