Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Here are some important elements to keep in mind before selling your company.

Selling a business is a major milestone. Building a company from the ground up takes years of energy, late nights and tough decisions, so parting with it can feel like letting go of a piece of yourself. That’s why it’s essential to understand what goes into a sale long before you list the business.

Before you start the process, take time to look closely at the financial, operational and personal factors that shape a successful exit strategy. Here’s what you need to know about selling your company — including the steps to take, what to think through and how to recognize the right moment to make your move.

Selling a business can be stressful, but with careful planning, you can ensure a smooth transition for all parties involved.

Before you even begin the selling process, think about what your life will look like after the deal closes. Most entrepreneurs pour years of energy, identity and routine into their business. When it’s gone, even by choice, the sudden change can leave a surprising gap.

If you’re planning to start another venture, give yourself some breathing room before diving back in. Take time to reconnect with friends and family, catch up with old colleagues or finally take that vacation you’ve been putting off. Many business owners report feeling a sense of loss after a sale, so building in space for a personal reset can make the transition much easier on your mental and emotional well-being.

Before you sell, make sure the decision is coming from a thoughtful place rather than pressure or impatience. You should never feel rushed into a deal. Take an honest look at whether you, your business and your team are truly prepared for this transition.

On the business side, shore up any weaknesses you can before entering negotiations. Small improvements can have a real impact on your valuation. Because it’s hard to view your own company objectively, consider asking trusted employees, partners or even a few long-time customers where they see room for improvement. That perspective can help you make smarter adjustments before you start talking numbers.

Every big business decision comes with trade-offs, and selling is no different. Take time to look at what you may be leaving behind — future growth, work you genuinely enjoy, or projects you haven’t had a chance to pursue. It’s also worth thinking about how letting go of the business could shape your career and your personal life moving forward.

Understanding these trade-offs can also help you negotiate more effectively. For instance, if selling the business would limit your ability to work with a specific patent, technology or customer segment, you may be able to include a provision in the agreement that protects your ongoing involvement. When you’re clear about what matters most, it’s easier to structure a deal that supports your long-term goals.

Before you enter negotiations, take a clear inventory of what your business is worth today and what its future potential adds to that number. Buyers want to see both: proven performance and realistic growth opportunities.

Because it’s easy to overvalue or undervalue your own company, consider hiring an independent business valuation expert. A third-party assessment gives you a more objective picture of your business and adds credibility to your asking price, which can make discussions with buyers smoother and more transparent.

When more than one buyer is interested, you create competition, and that often leads to stronger offers and a faster path to closing.

As you review bids, look beyond the price. Consider how each buyer plans to use the business, what the transition would look like and whether the proposed terms support your long-term goals. This is also a smart point in the process to consult a merger and acquisition advisor, especially if you’re weighing complex or competing offers.

Selling a business can stir up a lot of emotions. Buyers will inevitably look at your company through a critical lens, and their feedback or valuation may feel harsher than you expected. Try not to take it personally. A buyer’s assessment reflects their priorities, not your worth as a founder.

Staying clear-headed and objective will help you navigate the process more effectively. Give yourself space to process the emotional side while keeping negotiations grounded in facts, numbers and long-term goals.

Buyers want to see a business that’s already performing well and positioned for profitable growth, not one that relies solely on predictions or best-case scenarios. Include long-term potential in your valuation, but don’t let it overshadow the company’s current reality.

At the end of the day, buyers pay for what the business is today. Holding out for an inflated price based only on future hopes can stall negotiations and cause strong offers to disappear.

The number on the check is only one piece of a business sale. Deal structure can matter just as much — sometimes more. Salary guarantees, stock payouts, installments, earnouts, future ownership stakes and other provisions can significantly change the true value of the offer.

Look at the entire contract, not just the headline price. Make sure you and your team understand how each term affects your financial future and the transition that follows.

A business often feels like an extension of its founder, so it’s natural to care about what happens after you step away. Look for a buyer who respects the legacy you’ve built and plans to maintain the company’s product quality, brand and mission statement. This is especially important if your name will remain tied to the business or if long-time employees and customers helped shape the culture you worked hard to build.

Choosing a buyer whose values match yours can make the transition smoother and give you confidence that the business will continue in the direction you intended.

Think carefully about how the sale will affect your team. Will roles change under the new owner? Are jobs secure? Will salaries or employee benefits shift? These are the questions employees worry about most, and having clear answers can ease a lot of stress.

Whenever possible, structure a deal that protects your staff or sets them up for new opportunities. If that isn’t fully within your control, do what you can to support them through the transition, whether that means open communication, severance package options or helping them find their next role.

Several factors can influence both the process and the final outcome of your sale.

Naturally, how much you’ll earn from the sale — and how quickly you’ll find a buyer — depends on the value of your company. Buyers will look at both your current performance and your projected value over time. Understanding where your business stands on both fronts will help you set a realistic price and negotiate from a position of strength.

Timing can have a major impact on what your business is worth. Market conditions, industry trends and broader economic factors all play a role. Spending time researching the current environment can help you determine whether it’s the right moment to move forward or if waiting could produce better offers.

Choosing the right deal structure can minimize tax liabilities and help you walk away with the best overall outcome. Most small business sales fall into one of two categories:

Selling your business requires sharing certain information with potential buyers, but that also means competitors could gain insights into your operations or customer base. To protect yourself, it’s common to have prospective buyers sign nondisclosure agreements and to work with legal advisors to make sure those agreements are clear and enforceable.

Not every buyer approaches a sale with genuine intent. Some competitors may pose as interested parties simply to collect information. Others may be sincere but lack the capital or commitment to close the deal. A thorough vetting process — including financial checks and reference reviews — can help ensure you’re working with reputable, capable buyers who are truly aligned with your goals.

When word gets out that your business is for sale, customers may feel uneasy, especially if they’re worried about changes to service or support. Suppliers also need timely communication so that contracts, pricing agreements and delivery schedules continue without interruption.

Providing buyers with detailed documentation, including major contracts, service agreements and internal policies, while maintaining open, honest communication with customers and suppliers can help keep relationships strong during the transition.

You must remain compliant with employment laws throughout the sale. Employees are often expected to continue working during the transition, and any layoffs or role changes must follow proper legal procedures. If contracts need to be updated or terminated — for example, in a merger or acquisition — ensure everything is handled correctly and documented.

It’s crucial for a buyer and a seller to thoroughly review the terms of the deal, including any fine print or specific clauses. Both parties must be comfortable with these terms and prepare to meet any requirements to complete the sale as envisioned. Clear communication about future goals and expectations on both sides can help prevent potential conflict.

Once a buyer accepts your offer, the next step is due diligence. You’ll need to supply documents such as contracts, licenses, financial statements, projections and company policies to support your valuation. Building time for this process into your timeline is essential. Working with legal support services to review materials ahead of time can streamline the process and help avoid delays.

Your role doesn’t necessarily end when ownership transfers. Depending on your goals, you may stay on as an employee, join the board of directors, act as a consultant or retain a financial stake as a shareholder. Each option comes with different levels of control, time commitment and financial benefit, so you can choose what aligns best with your personal and professional plans.

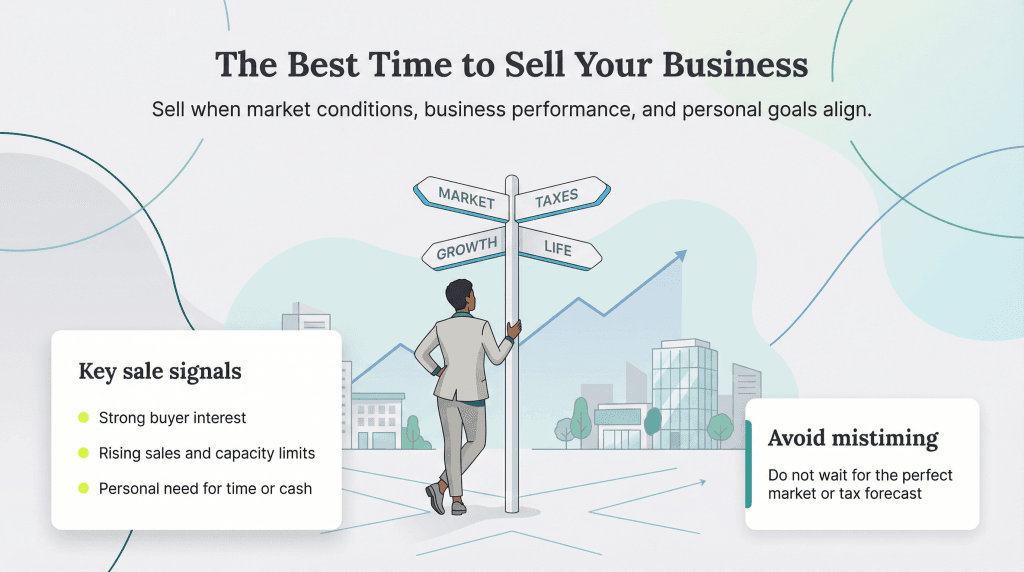

It makes sense to consider selling a business when the following conditions are present.

The market for business acquisitions and mergers fluctuates with economic conditions and industry trends. In recent years, private equity activity and strategic acquisitions have remained active, creating strong buyer interest across many sectors. According to Private Equity International’s Full-Year 2024 Fundraising Report, private equity firms raised $746.48 billion globally in 2024, signaling that there is still significant “dry powder” (unused capital set aside for acquisitions) available.

That said, don’t try to time the market perfectly, as it’s nearly impossible. As a general rule, if you’re already considering a sale and market conditions happen to be favorable, it may be a good moment to take the first steps.

Tax laws aren’t set in stone. Congress and the president can change rates to respond to economic conditions, and although these changes usually come with advance notice, they can still affect the timing of a business sale. Because selling a business is a taxable event, a higher tax rate could reduce your net proceeds. If you anticipate a tax increase on the horizon, you may want to complete the sale before new rates take effect.

If demand for your products or services is rising, it may be a good time to consider listing the business. Strong, consistent sales growth is attractive to buyers and can help you command a higher price. Just don’t fall into the trap of trying to time the market perfectly; focus on showing a solid sales record and demonstrating reliable growth.

Every business hits a ceiling at some point. Maybe you need new leadership to take the company to its next stage, or perhaps the business requires a level of investment you can’t take on yourself. In these situations, selling may be the most strategic option.

If this is the case, be upfront with potential buyers during negotiations. Many deals are structured to account for future investment needs, and business transparency can help both sides reach an agreement that supports the business’s long-term health.

Running a business is more than a full-time commitment, and burnout is common. If you increasingly feel the pull toward more personal time — whether to travel, reconnect with family, or simply rest — selling the business may be the right move to achieve a better work-life balance.

It’s important to remember that selling isn’t a sign of failure. Priorities shift, and stepping away can be the healthiest decision for your mental and emotional well-being.

Selling a business often results in a significant cash payout. For some owners, that influx of capital is necessary to navigate a major life change such as a health issue, divorce or retirement. Others may use the proceeds to fund a new venture or opportunity.

Just avoid spending the money too quickly. Take time after the sale to understand your financial picture, plan your next steps and ensure the funds support your long-term goals.