Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

An exit strategy is a key component of entrepreneurship, as it can provide a sense of safety and peace of mind.

You wrote a business plan when you launched your company. Now, if it’s time to say goodbye, you need an exit plan — one that maximizes your return on your investment and limits your potential future exposure to risks related to the company. But, years of experience teach you that nothing in business is predictable, including ending your tenure.

We’ll explain why every business owner needs an exit strategy — or two! — and share factors, advice and effective tactics to consider.

Natalie Roberts, CEO and president of iKadre, a mergers and acquisitions (M&A) advisory for women-owned businesses, emphasized the importance of establishing an exit strategy from day one. “Through my experience leading HP’s $13.9 billion acquisition of EDS and helping countless women entrepreneurs exit their businesses, I’ve learned that the most successful exits begin with the end in mind,” Roberts explained.

It may seem counterintuitive to launch or buy a business while simultaneously planning how to exit it. However, this approach brings numerous benefits, including the following:

We’ve been discussing the importance of an exit strategy, but, in reality, you’ll need to prepare two plans: one for a voluntary exit and one for an involuntary exit.

With a voluntary exit strategy, you’ll know the following:

An involuntary exit strategy helps you prepare as best you can for unforeseen situations, including the following:

Voluntary and involuntary exit plans will both address the following factors:

Sidharth Ramsinghaney, director of corporate strategy and operations at cloud communications firm Twilio, noted that an involuntary exit strategy is more than a crisis response plan; it’s a comprehensive risk management framework.

“Smart owners maintain updated data rooms, clean financials and documented processes not just for planned exits but as insurance against unexpected market shifts or personal circumstances,” Ramsinghaney explained. “This preparation typically reduces transaction timelines when speed becomes critical.”

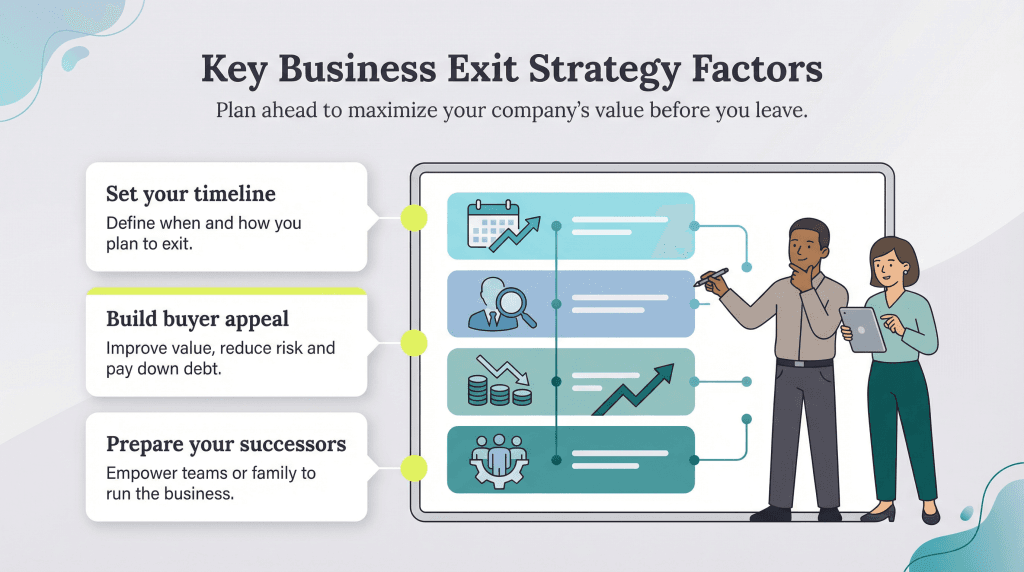

Developing a well-rounded exit strategy requires close attention to the following.

For your voluntary exit strategy, set a date in the future and a metric you want to achieve, such as hitting a particular level of company revenue and profitability. If you reach the end date but miss your targets, decide in advance whether you’ll still want to proceed with a sale.

When you have a fixed departure date in mind, your approach to running the business changes. You’ll start thinking both short-term and long-term in your decision-making. You’ll be focused on navigating day-to-day operations successfully while also looking for ways to build more value in your business to make it as attractive as possible to potential buyers.

Develop buyer personas — documents that detail the type of person or company likely to buy your business. (These are similar to customer personas, which are developed to identify your ideal customer.) Here are a few examples of buyer personas for various business types:

Company type | Likely buyer |

|---|---|

Local retail or hospitality business |

|

Fast-growing e-commerce company |

|

Scientific or professional services company |

|

As-a-service subscription model |

|

“By building your business to appeal to multiple buyer types, you create competitive tension that typically delivers higher valuations,” Ramsinghaney explained. “I always advise clients to structure operations and reporting with this endgame in mind.”

Don’t limit your company’s selloff potential by only considering buyers in your specific field.

Consider this example: You’re an e-commerce retailer; you’ve developed custom software that places your products in prominent search positions on third-party sales platforms. That, of course, would be of great value to a purchaser in your sector.

However, that software may hold even greater value to a technology company, and you could make significantly more money selling or licensing it than selling your business. Additionally, if your company encounters financial difficulties, you could sell the rights to the software to raise cash quickly.

Keep looking for ways to improve operations and profitability, bringing more customers to your e-commerce or brick-and-mortar store. For example:

Your goal is to add value to your assets and remain efficient. Your competitors can give you some ideas. Where are they doing better than you, and how can you match or beat them to stand out from the competition?

Achieving profitable growth will impress potential buyers. To do this, experiment with your advertising and marketing methods to achieve lower per-sale costs and boost successful conversions. Your goal is to show future buyers that your digital marketing ROI continually helps you achieve your goals.

Promote deals to customers through email marketing campaigns and short message service messaging, and aim to make as much money as you can on each sale. Always keep your future buyer in mind when setting prices and pursuing new business opportunities.

Customer loyalty is key to both voluntary and involuntary exit plans. Any potential buyer will value your loyal customer base. And, if a crisis arises, you can raise money quickly with one-time sales to loyal clients.

To establish and retain loyal customers:

Use customer tracking tools to calculate customer lifetime values and annual spending. Buyers typically look for those types of metrics. They also prefer companies with robust opt-in email marketing lists and text subscribers.

The hardest types of businesses to sell are mom-and-pop shops and one-person operations. To a buyer, it’s like buying a job, not a company. It’s also challenging to sell businesses where there are 10 to 20 employees, but the owner is still firmly in charge. It’s like buying the job of a senior manager.

To avoid those situations, ensure an able management team can run things in your absence. Ramsinghaney noted that building a business that can thrive without its current owners will improve your exit strategy and grow profitability.

“This means investing in systems, processes and people that make the business transferable,” Ramsinghaney explained. “Businesses with strong infrastructure and documented processes consistently command valuation premiums over comparable companies.”

Here’s some advice:

Is your exit involuntary, perhaps due to an illness? Then having these measures in place ensures you can step away for a while and still draw money, thanks to your responsible and empowered staff.

Some business owners intend to pass their company on to a family member, such as a child. If this is your plan, focus on creating a clear path for bringing them into the business and setting them up for success.

That’s exactly what Justin Eugene Evans, founder and CEO of EvansWerks, intends to do. His son has shown an interest in and aptitude for business, and Evans has a long-term plan for handing over control and stepping down.

“I think one of the worst mistakes that most leaders make is [not knowing] when to let go,” Evans explained. “It’s not about me and my ego, although I have one. I try to keep it in check and remind myself that … I am merely a temporary steward of something bigger than me.”

Not every child or relative will want to take over your business, and they will not necessarily have your skills and aptitude. However, if they’re willing to see how good a fit they are for the business and business management, bring them into the business as soon as you can.

Try to pay down as much business debt as possible. If another company takes over at some point, business equipment loans and factoring service agreements cannot be novated. In other words, your debts must be settled by “completion day” (the day you sell your business).

Normally, whatever you owe creditors is subtracted from the agreed-upon price you sell your company for, so you want less debt to subtract. Paying down debt also reduces your monthly servicing costs, resulting in more profit.

Selling your business can be costly — incurring lawyer fees, accountant fees, professional service fees, broker commissions and more. For a business with $1 million in annual revenue, expect to pay up to $150,000 for a successful sale. If a deal is agreed upon but falls through, you’ll still have to pay your outside advisors and experts.

If your business is struggling financially, having sufficient savings gives you more time to delegate day-to-day tasks to staff and raise cash by selling assets. Reducing payroll costs and finding other ways to save will help buy you even more time.

Roberts emphasized the importance of conducting a gap analysis to reduce risk for the buyer — whether the exit is voluntary or involuntary.

A gap analysis helps you identify weaknesses or gaps in your business that could lower its perceived value or discourage buyers. By addressing these gaps and reducing risks, you can increase the attractiveness of your business and potentially boost its sale price.

“When the risk is reduced, the multiple goes up,” Roberts explained. “That is a key item on how to create more value. It is not always about the EBITDA. If you can increase the multiple for a client and they listen, then it works the best for the seller.”

Startups and established businesses typically choose different ways to exit.

Follow these tips and best practices when executing your exit strategy.

Your buyer will likely have an advisory team, and you need one, too. You want people on your side who know the intricacies of selling companies and can help protect your interests.

Consider hiring part-time chief financial officers or fractional chief marketing officers well before putting your company on the market. Bringing in experienced, proven talent with broader business connections to your C-suite can help you improve the organization. They’ll be invaluable when executing your exit strategy and demonstrating the hidden but exploitable extra value in your firm.

Ramsinghaney believes a savvy team is crucial in a successful business sale. “Today’s M&A market demands more sophisticated exit preparation than ever before,” Ramsinghaney explained. “Buyers have become increasingly diligent about operational integration risks, making clean operations and strong management teams essential.”

Inform your business accountant that you want to be in a constant state of readiness in case you receive a purchase offer unexpectedly or decide to put your company on the market. Once you’ve identified the financial areas of greatest interest to your buyer type, ensure your accountant updates financial reports weekly or monthly and maintains accurate records.

“Potential buyers will scrutinize your financials, so they need to be more than just good — they need to be great,” business lawyer Justin McInerny cautioned. “This means partnering closely with your accountant or bookkeeper to ensure your records are not only current and accurate but also presented in a way that highlights your business’s strengths and profitability.”

Retain a business lawyer, preferably one with M&A experience. Your buyer’s corporate lawyers will vigorously defend their interests. They’ll also try to use the information you provide about your business during the due diligence process to lower the selling price. You need someone on your team to advocate on your behalf.

“Get a good M&A attorney to represent you personally,” Matt Brubaker, chairman and chief executive of human capital advisory firm FMG Leading, advised. “Your firm, your PE firm and others in the deal will have perspectives that are adjacent but not identical to your needs. Take the time to learn the structures and waterfalls and get grounded in what you’re stepping into.”

Opinions differ on the effectiveness of business brokers and M&A advisors for companies with an annual revenue of less than $1 million. If you’re confident enough, it might be worth forgoing an advisor and handling the process yourself.

Still, brokers perform vital functions, like:

Brokers may also intervene during the due diligence stage. During due diligence, the buyer’s lawyers and accountants will ask for detailed information about your company, often over a period of 3 to 6 months. Their job is to help the buyer understand exactly what they’re buying.

Tempers often become strained during due diligence for various reasons. When this happens, brokers often act as go-betweens to smooth relations and keep the deal on track.

In years past, a buyer’s lawyer would enter a private room at your lawyer’s office called a “data room.” Here, they’d inspect financial and employment records, as well as documentation regarding intellectual property ownership and previous and ongoing legal disputes. Today, most data rooms are virtual, with the buyer and seller’s teams typically exchanging documentation via email.

Create your own online data room as soon as possible and ask your accountants, lawyers and managers to submit updated reports every month. Delays in providing information can frustrate buyers — something you want to avoid.

Ensure your current lease will fit into any deal to sell your company. McInerny cautioned that a commercial lease with unfavorable terms can ruin a deal. “A favorable lease can significantly increase your business’s appeal, while a problematic one can kill a deal,” McInerny explained.

Most leases need the written consent of landlords before a lease transfer or reassignment to the business’s new owner can be made. “Landlords often have broad discretion in granting or denying consent,” McInerny noted. “This means your potential buyer needs strong financials and a solid credit history to be considered. Start thinking about this early in the process.”

Short leases can also be problematic and may even devalue your business. “If you’re serious about selling, a long lease term is essential,” McInerny advised. “This might mean negotiating a renewal, even if it means committing to a longer term initially. The understanding is that the new owner will assume the lease.”

After selling your business, you may want to stay involved for a while to help smooth the transition. The new owners may welcome this involvement to better understand current systems and processes and decide what needs to be changed.

However, returning to a workplace you no longer run can feel strange. Your former team may even look at you differently. That’s OK and completely expected — it’s all part of the transition.

Brubaker emphasized the importance of being seen as the new owner’s most enthusiastic and vocal supporter. “Dogmatic assertions — and, even worse, sabotaging new owners by commiserating with your former team about how ‘out of touch’ [they] are — destroys value 100 percent of the time,” Brubaker warned. “Be part of the future — your earn-out depends on it!”

Once you’ve settled on an exit strategy, limit your focus on it to no more than 30 minutes per day — even if you have a deal on the table going through due diligence. Instead, concentrate on running your business as effectively as possible to retain and build on the value you’ve already created. Buyers expect this, and they’ll be monitoring the updated information in the data room to ensure their interests are protected.

“Leaders should continue to run their organizations as though they intend to run them forever with an eye on long-term, sustainable value creation,” Brubaker explained.

In other words, keeping business as usual while preparing for the future is the best way to be ready for a voluntary or involuntary exit.