Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Launching a new venture is an exciting milestone, but thorough preparation is key to survival. Below are 10 essential steps to take before opening your doors, along with common pitfalls to avoid.

Business ownership is on the rise, with budding entrepreneurs taking the leap every day. According to the U.S. Census Bureau’s Business Formation Statistics, more than 5.4 million new business applications were filed in 2024, proof that plenty of people are still willing to bet on themselves.

If you’re thinking about joining their ranks, there are some essential steps you need to take — and a few costly mistakes to avoid. This guide walks you through what to do before you launch so you can start your business on solid footing and position it for long-term success.

Before you start filing paperwork or spending money, take time to think through the essentials. The checklist below covers the most important steps to handle before launching your business.

Every successful business starts with an idea. Whether you have a clear vision or you’re still in the brainstorming phase, shaping that initial concept into something workable is an essential first step.

“Before diving into logistics, ensure your business idea solves a real problem or fulfills a market need,” advised Grzegorz Kowalski, founder and CEO of Tripoffice.com.

Kowalski advises getting feedback early from your intended target audience. Informal conversations, quick polls or a small focus group can help you spot weak points and refine your idea before you invest too much time or money.

Spending time or money upfront can feel risky when you’re still testing an idea, but it’s often better to uncover potential issues early. “This will lay the foundation for every other step,” Kowalski said.

Once your idea starts to take shape, it can be tempting to move straight into execution. Before you do, take time to understand the industry you’re entering and the competitors you’ll be up against.

Looking at the broader market helps you see where your business fits, what customers already have and where there may be room to do something better or different to help you stand out from the competition. One helpful way to frame this research is with a SWOT analysis, which examines your strengths, weaknesses, opportunities and threats in the context of the competitive landscape.

“Understand your industry, target audience and competitors. This involves identifying market trends, gaps and customer preferences,” Kowalski said. “A deep understanding of the market will help you position your business strategically.”

A business plan is more than a document you check off a list. It’s a working roadmap that helps guide your growth, clarify your thinking and prepare you for challenges before they arise. Writing one also forces you to answer detailed — and sometimes uncomfortable — questions about how your business will actually operate.

“The process of creating a business plan forces founders to analyze the market, evaluate competitors, define their brand and outline a marketing strategy,” explained Eric Proos, founding partner at Next Era Legal. “It can even help clarify which legal structure may be most appropriate for the company.”

A business plan is also often required when you’re seeking outside funding, whether you’re applying for a business loan or seeking investors. It gives potential funding sources a clear picture of your idea, your industry knowledge and how you plan to turn that idea into a viable business, including your financial needs and potential for profitable growth.

“Down the line, a solid business plan is often indispensable when seeking funding from banks or investors,” Proos noted.

The legal structure you choose shapes how your business operates in some important ways, from how you’re taxed to what paperwork you’re required to file and how easily you can raise money. Each type of entity comes with its own rules, costs and limitations, and the right choice depends on your goals, risk tolerance and growth plans.

Common legal structures for small businesses include:

“A simple LLC [limited liability company] should suffice to start,” advised David Salerno, founder of Entrepreneur Sherpa. “You can start without setting up a more complex structure like a C-corp [C corporation] until your business generates significant sales and growth, justifying the legal setup and recurring costs.”

Because this decision can have long-term tax and liability implications, it’s wise to consult with a business lawyer or a certified public accountant (CPA). Choosing the wrong entity upfront can create avoidable tax burdens or legal issues that are costly to unwind later.

Once you’ve chosen a legal structure, the next step is making your business official. That typically means registering with your state, securing any required licenses or permits and obtaining a federal tax identification number.

“Find a resource online to help you do this efficiently, like LegalZoom or ZenBusiness,” Salerno recommended. “Getting legal help might be justified if you have more complex needs.”

Taking the time to register properly helps you avoid fines, delays or compliance issues later. A simple checklist can go a long way toward making sure you’ve covered the required filings at the federal, state and local levels.

Launching and growing a business takes money, and most founders use a mix of funding sources to get started. The right option depends on how quickly you want to grow, how much control you want to keep and what your business can realistically support early on.

Common ways to finance a new business include:

Many businesses use a combination of these options. Smaller ventures often start by bootstrapping, sometimes supplemented by help from friends, family or a modest loan. Businesses with larger ambitions or heavier capital needs may require outside investment earlier on.

Before you open your doors — virtual or physical — you need to know where your business will live. That might be a home office, a co-working space or a dedicated storefront, but either way, you’ll want the basics in place before your first day of operations.

For a physical location, that typically includes:

At the same time, your digital presence is just as important as your physical one. Most businesses need a website, a claimed Google Business Profile and at least a few social media accounts so customers can find and evaluate them online.

“‘Location, location, location’ is cliché, but times have changed,” Salerno said. “[Y]ou have to think of location in both physical terms … and digital terms.”

When designing your website, take time to compare the best website builders available so you can choose a platform that meets your immediate needs and can support future functionality, such as online ordering, booking or e-commerce. You may also want to factor in the costs and operational differences that come with running a brick-and-mortar vs. e-commerce store.

Once your site is live, search engine optimization (SEO) becomes critical. Optimizing your site’s structure, content and listings via an SEO strategy helps customers actually find you, not just admire your design.

Business insurance isn’t just a formality; it’s protection against risks that could otherwise derail your company early on. The right coverage depends on what your business does, where it operates and the kinds of risks you’re exposed to, from customer injuries to property damage or data loss.

There are many types of business insurance to consider, including:

Not every business needs every type of insurance, but most need some combination tailored to their situation.

“Get the right advice from the right specialist for business insurance: different regulations, different states,” Salerno said. “Don’t get caught up in not being covered properly.”

Skipping insurance to save money early on can be tempting, but it often creates far more risk than reward. Take time to assess your specific exposure, whether that’s physical work at customer sites, employee-related risks or cybersecurity concerns, and make sure you’re covered before you start operating.

It’s also important to understand local and industry-specific requirements. Some businesses are legally required to carry certain types of insurance to operate. For example, trades like plumbing or carpentry typically require liability coverage. Review what applies to your business so you can stay compliant and protected from day one.

No business succeeds in a vacuum. Early on, surrounding yourself with the right professionals, including lawyers, accountants or advisors, can help you avoid costly mistakes and make smarter decisions as you build from the ground up. While professional help can feel expensive at first, it’s often money well spent.

“Enlist experts such as accountants, lawyers or consultants to handle complex matters like taxes, contracts and compliance,” Kowalski advised.

As your business grows, you’ll also need to think carefully about who you bring on to help run it day to day. Depending on your hiring process timeline and needs, that might mean recruiting employees, working with contractors or engaging a professional recruiter to find specialized talent. Recruiters can save significant time by sourcing and vetting candidates who match your culture and skill requirements — an upfront cost that can pay off if it helps you build a strong team faster.

Starting a business doesn’t mean figuring everything out on your own. Many public, nonprofit and educational organizations offer free or low-cost resources to help entrepreneurs validate ideas, navigate compliance and access funding.

“Your state’s economic development office and local startup ecosystem, including local colleges and universities, often offer complimentary services to help, including writing business plans, reviewing legal contracts, et cetera,” said Meredith Bowen, a partner at Walker Bowen Talent Partners.

You can also lean on guidance from your state or local business authority, as well as national organizations like the SBA and the IRS, during the planning and setup process. Groups such as Service Corps of Retired Executives (SCORE) offer free mentoring, workshops and educational resources designed specifically for small business owners.

Taking advantage of these resources can save you time, reduce costly mistakes and give you access to expertise that would otherwise be expensive to replicate on your own.

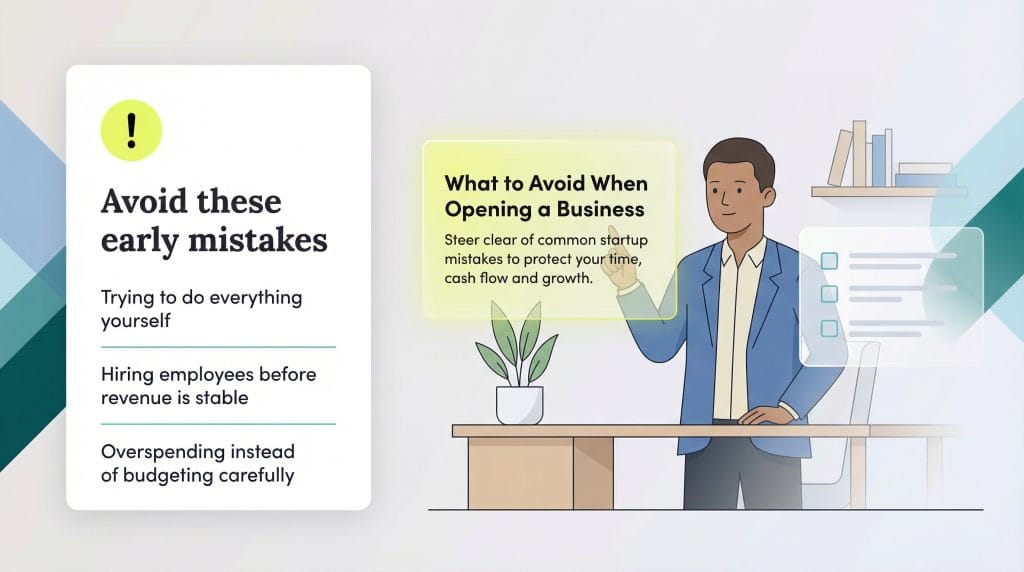

Knowing what not to do can be just as valuable as having a solid plan. Here are some of the most common missteps entrepreneurs make and how to avoid them when you’re getting started.

Entrepreneurs are natural go-getters, but attempting to handle every task on your own is a fast track to burnout. Small business owners wear a lot of hats, but that doesn’t mean you should wear all of them forever.

Take an honest look at which responsibilities pull you away from the work that has the biggest impact on your business. If you’re a product visionary but struggle with numbers, for example, outsourcing bookkeeping can improve accuracy while freeing you to focus on growth.

While you shouldn’t do everything alone, rushing to hire full-time employees can strain your finances. Staffing your business increases payroll, benefits and overhead costs, all of which can put pressure on cash flow before your revenue is ready to support it.

Early on, freelancers or contractors can offer flexibility. You can bring in help on an as-needed basis and scale those roles into full-time positions as your business stabilizes. This approach lets your workforce grow in step with your revenue.

When you’re launching a business, restraint matters. Focus your spending on tools and resources that directly support revenue, and question every expense that doesn’t clearly move the business forward.

Working with an accountant can help you build a realistic business budget based on your current and projected income. They can also help you identify tax deductions and prioritize spending so you’re investing in growth, not unnecessary upgrades.

Being first to market doesn’t help if your product or service isn’t ready. First impressions are hard to undo, and launching before you’ve worked out key issues can cost you early customers who are difficult to win back.

Take the time to test, refine and validate your offering so you’re confident in what you’re delivering when you go live.

Many new owners don’t realize how much day-to-day attention a business demands. When the workload outpaces your capacity, the first thing to suffer is usually the work itself.

It’s better to be upfront about timelines and limits than to overpromise. Telling clients when you’re booked can reinforce trust; it shows you’re in demand and focused on doing the job well.

Sean Peek contributed to this article. Source interviews were conducted for a previous version of this article.