Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Commercial auto liability insurance protects a business against the costly outcomes of at-fault accidents involving company vehicles.

When you have vehicles that are used for business purposes, you are at risk of road incidents that can lead to serious liabilities. If you don’t have the right insurance coverage tailored specifically for your commercial vehicles, your business could be on the hook for those liabilities. This can cause financial strain and legal repercussions.

To mitigate these risks, you’ll want to purchase a commercial auto liability insurance policy. This business insurance policy helps absorb the financial impact of at-fault accidents involving your business vehicles, protecting your assets and providing you peace of mind. This guide will review what commercial liability auto insurance covers (and doesn’t).

“Businesses rely on vehicles to operate — whether for deliveries, transporting employees or service calls. Accidents happen and when they do, the costs can be devastating,” said Chris Peterie, CEO and co-founder of Tower Street Insurance. Commercial auto liability insurance is a component of an auto insurance policy that pays up to a policy limit for bodily injuries and property damage in at-fault accidents. Commercial auto liability insurance covers the same types of liabilities as personal liability auto insurance, except the policy is rated for the risk of commercial vehicles.

For example, let’s say a florist has a delivery truck that it uses to bring bouquets to recipients. This means the delivery truck is used for business purposes and needs commercial auto liability insurance, not personal auto liability insurance. If the delivery driver rear-ends another car at a stoplight, the commercial liability policy would pay for the damages to the other vehicle and any injuries to the other vehicle’s driver and passengers. Payments will not exceed policy limits.

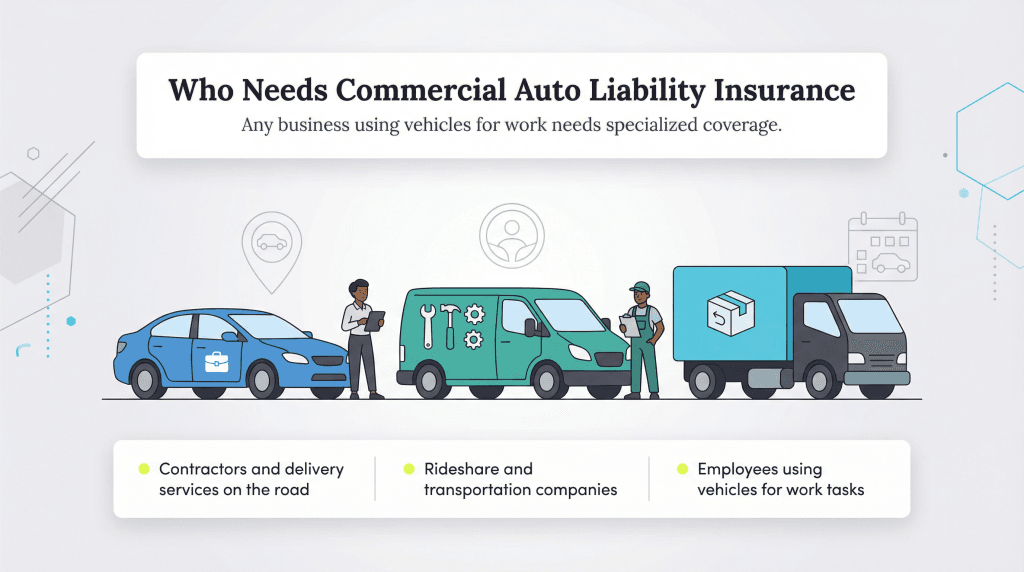

If you’re a business owner who owns or rents company vehicles that you or your employees operate, then you need the added protection of commercial liability auto insurance. This type of coverage is also necessary if your employees use their personal vehicles for business-related responsibilities. “Commercial liability auto insurance is structured to handle the higher legal exposure and potential damage businesses face,” said Dennis Shirshikov, an adjunct professor of economics at City University of New York. [Find the right carrier in our best business insurance guide]

Any business that owns, leases or uses vehicles for work purposes needs commercial auto liability insurance, according to Shirshikov, including:

Liability insurance is required by law in most states. If your vehicle is designated for commercial use, it must have commercial liability auto insurance. However, there are some exceptions. For example, if you use your personal vehicle for some business activities as real estate agents often do, then your personal auto policy may allow a special “for business pursuits” designation that will cover you when the auto is used for work.

If you live or do business in one of the few states that don’t require liability insurance for vehicles, such as New Hampshire and Virginia, it’s important to know that drivers or business owners are still liable for the damages an accident causes. If the accident were severe enough, a person or business could become financially devastated trying to cover the costs.

When you buy commercial auto insurance, you are first and foremost buying liability coverage. The liability coverage amounts required may vary from state to state, with many insurance carriers setting minimum policy amounts. For example, Nationwide recommends at least $500,000 and requires a minimum of $100,000 in commercial auto liability coverage per vehicle.

If your coverage were $100,000/$300,000/$100,000, your protection would look like this:

Let’s look at an example with these sample limits. Assume three people are injured in an accident, with injury expenses costing $110,000, $90,000 and $100,000. The total amount of the injuries is $300,000, so it’s covered by the cap. However, the per-person limit is $100,000, which means the first person isn’t covered for the extra $10,000 — and they could sue you for the difference.

This is why Nationwide and other insurance carriers recommend having at least $500,000 in coverage and going as high as $1 million on commercial auto policies.

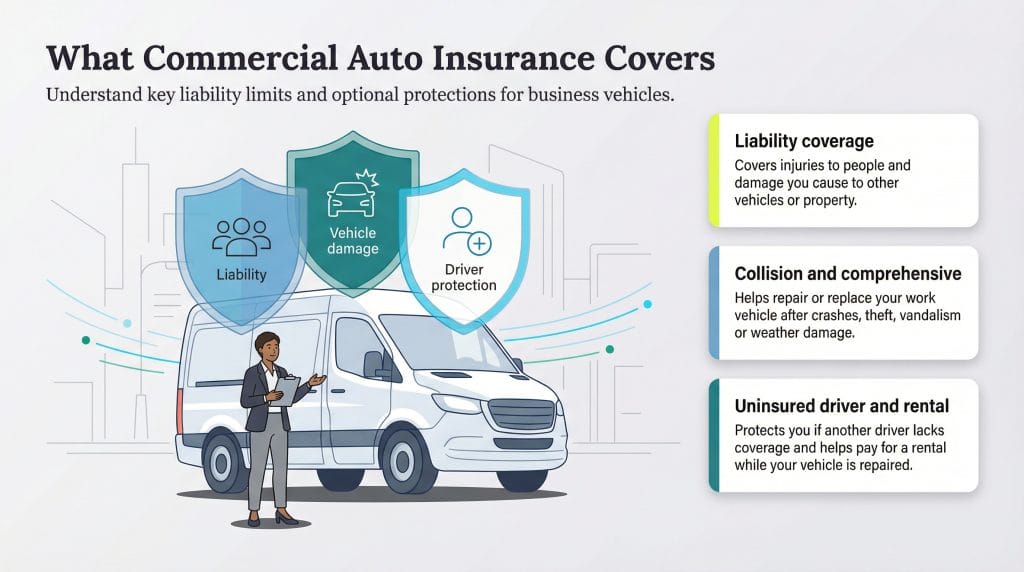

These are some other coverages you should consider including in your commercial auto insurance policy:

Any vehicle that is used for business purposes can be covered by commercial liability auto insurance, including delivery vehicles, service trucks, food trucks and company cars. In addition to company-owned vehicles, commercial auto insurance can cover any personal vehicles that you or your employees use for your business. This type of coverage applies to large fleets with dozens of vehicles as well as small businesses with a single car or truck.

While a commercial auto insurance policy can be very robust, it doesn’t cover everything. The following are not included coverages in commercial auto insurance:

The primary purpose of a commercial auto policy is to provide liability insurance. As such, every commercial auto policy will have some level of liability coverage within it. Other coverage types are optional.

However, the minimum coverage amounts may not be enough to absorb the financial ramifications of accidents. Business owners should consider increasing limits or adding a commercial umbrella policy to their insurance portfolio.

It’s hard to gauge how much coverage a business will need. While most insurance carriers have minimum amounts, the minimum may not be enough for all business owners. When figuring out how much liability coverage you need, consider the following:

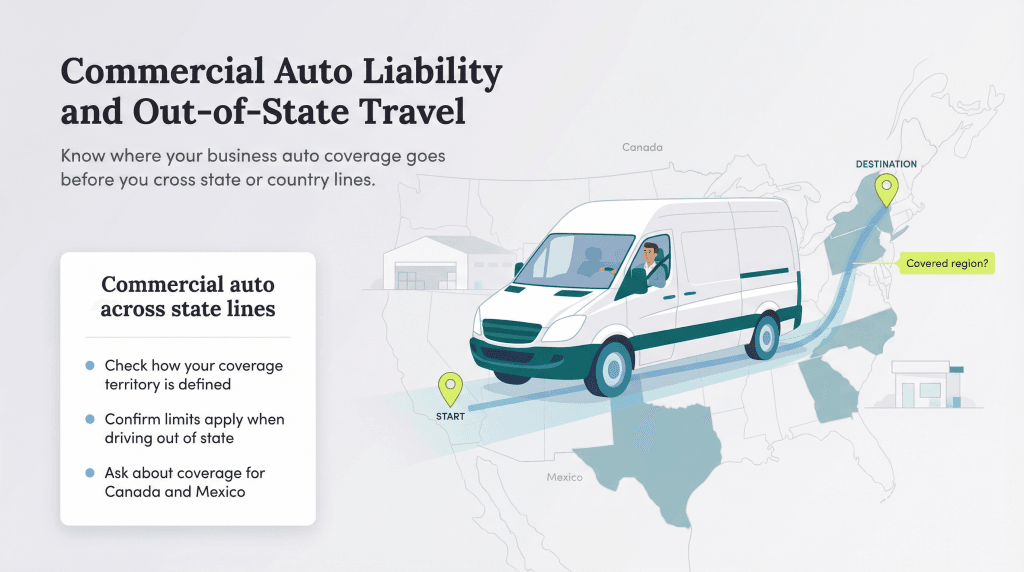

Your business’s travel needs are an essential consideration when choosing business insurance.

When you buy commercial auto insurance, you’re buying it in the state in which your vehicle is registered. This is where your state’s Department of Motor Vehicles will check that you meet the minimum insurance requirements. However, many vehicles are driven across state lines in the course of work. In these instances, the insurance policy’s coverage territory comes into effect.

Most insurance carriers will extend coverage throughout the United States so that you have the same coverage limits wherever you go. Some carriers may limit coverage out of the state, however, so it’s best to check with your provider to see how coverage works with your policy.

Some carriers may also extend coverage to Canada and Mexico. If so, you won’t need to get international coverage for cross-border commutes. Again, these coverage nuances are carrier-specific, and you should check with your provider if you think you need this type of coverage.

Sean Peek contributed to the reporting and writing of this article.