Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

A break-even analysis is an essential element of financial planning. Here’s how to apply it to your business.

A break-even analysis is an indispensable financial planning tool that helps you understand your business’s revenue, expenses and cash flow so you can work toward profitability. Below, we’ll examine break-even analyses and how this essential form of financial planning helps business owners make informed decisions.

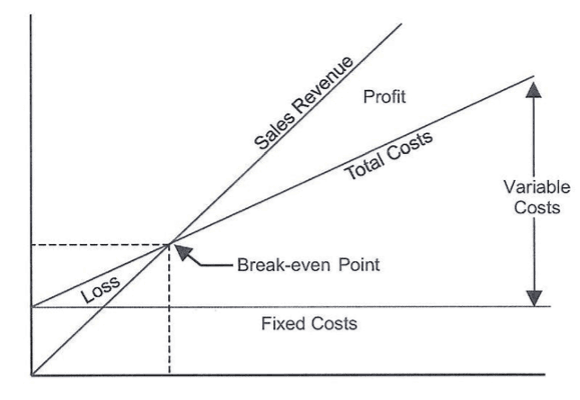

A break-even analysis is a calculation that determines the number of products or services a business must sell to cover its expenses, especially fixed costs. It is expressed by this formula:

Fixed Costs / (Average Price – Variable Cost) = Break-Even Point

A break-even analysis helps determine when your company will generate enough revenue to cover its expenses and begin earning a profit. It could also be run on a single product or service, rather than an entire business.

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

According to the U.S. Small Business Administration, a break-even analysis is crucial for limiting business decisions made on emotions and helps potential businesses avoid failure by providing realistic analysis of potential outcomes. The SBA notes that this analysis is usually a requirement when seeking investors or debt funding for your business.

Let’s work through a comprehensive example using sample cost figures for a software-as-a-service (SaaS) startup:

Monthly subscription price: $149 per customer

Run your break-even analysis using the formula. Using the figures above, the equation would look like:

$72,800 ÷ ($149 – $31) = 617 customers

Result: This SaaS company needs 617 paying customers to break even each month. At 618 customers, they begin generating profit of $118 per additional customer (this is the contribution margin — the difference of $149 – $31).

Revenue at Break-Even: 617 customers × $149 = $91,933 monthly revenue

A break-even analysis gives you a clearer path forward and supports informed decision-making around budgeting, price setting and future planning.

A break-even analysis helps you set a clear target for covering costs, and also identifies the threshold at which your business becomes profitable. When you know how many units you need to sell, how many subscribers you need to sign up or how many hours you need to bill in order to start turning a profit, it becomes easier to devise strategies to do so and measure whether or not you’re on track.

When most people think about pricing, they primarily consider how much their product costs to create (fixed costs), and they fail to take into account variable costs. This leads businesses to underprice their products. Finding your break-even point will help you price your products correctly, taking into account both fixed and variable costs.

Using your break-even analysis, you can create a strategy for the future. Knowledge of your break-even point helps you determine whether it’s realistic, as well as ways to reach it sooner. These include taking steps like reducing your overall fixed costs, lowering the variable costs per unit, improving the sales mix by selling more of the products that have larger contribution margins, and increasing prices.

You should use a break-even analysis to answer the following questions about your business:

“It’s much easier for people to decide whether they can beat that minimum than guessing how many sales they may make,” said Rob Stephens, founder of CFO Perspective.

Here are three times you should consider performing a break-even analysis.

Stephens suggested using a break-even analysis to assess how long it will take for any planned investments or changes in your business to become profitable.

“These investments might be a new product or location,” Stephens said. “I’ve done break-even calculations many times for modeling the minimum sales needed to cover the costs of a new location.”

This analysis is also helpful when you’re lowering your prices to beat a competitor or increasing prices to keep up with inflation.

“The most common use of break-even analysis in my career has been modeling price changes,” Stephens said. “You can … use break-even analysis to determine how many more units you need to sell to offset a price decrease.”

When making changes to your business, you may be bombarded with various scenarios and possibilities, which can be overwhelming when you’re trying to make a decision. Stephens suggested using a break-even analysis to narrow down your choices to scenarios with straightforward yes-or-no questions.

For example, “Can we do better than the minimum needed for success?”

The following hypothetical examples show how break-even analysis applies across different business types and decisions.

Imagine a women’s clothing boutique considering whether to open a second location. With monthly fixed costs of $18,500 and an average gross margin of 65 percent on clothing items, the owner calculates she needs $28,462 in monthly sales to break even ($18,500 ÷ 0.65). By analyzing local foot traffic data and nearby competitor performance, she determines the new location could realistically generate $35,000 per month — providing a $6,538 monthly profit cushion above the break-even threshold. That kind of clarity makes it much easier to move forward with confidence.

Consider a manufacturer of electronic components with fixed costs of $180,000 per month. Each unit costs $22 to produce and sells for $58, creating a $36 contribution margin per unit. The break-even point is 5,000 units monthly ($180,000 ÷ $36). When a major client requests a 15 percent price reduction — dropping the sale price to roughly $49.30 — the contribution margin falls to about $27.30 per unit, pushing the new break-even point to approximately 6,593 units. Armed with that data, the manufacturer can enter negotiations with a clear alternative: pursuing cost reductions elsewhere rather than absorbing a margin-eroding price cut.

Imagine a business advisory firm with monthly fixed costs of $42,000 that charges clients an average of $275 per hour. With variable costs of $85 per billable hour (primarily consultant wages and overhead), the contribution margin works out to $190 per hour.

That firm would need to bill 221 hours monthly to break even ($42,000 ÷ $190). Running this kind of break-even analysis can reveal utilization gaps — and often prompts decisions like adopting project management software or tightening scheduling practices to improve billable efficiency.

While break-even analysis is a valuable tool, it’s important to understand its limitations:

Many businesses fail to include all variable costs such as payment processing fees, shipping costs or sales commissions. If some variable costs are not included, the break-even analysis may not be accurate.

Semi-variable costs (like utilities that have both fixed and variable components) are often incorrectly categorized. It is recommended that the fixed portion be separated from the variable portion of mixed costs.

When calculating break-even for target profits, many forget to account for taxes. As noted by ICAEW, “profits are derived post tax, so we need to gross up the target figure by (1 – tax rate).”

Failing to consider seasonal changes, competitor actions or market demand fluctuations can lead to unrealistic break-even projections.

A break-even analysis requires current, accurate data. Using historical pricing or cost information without adjusting for inflation or market changes reduces accuracy.

Break-even analysis works best when combined with other financial planning tools. We recommend incorporating the following.

While break-even analysis shows profitability, cash flow projections reveal when money actually enters and leaves your business. This timing difference is crucial for maintaining operations.

Test how changes in key variables (price, costs, volume) affect your break-even point. This helps identify which factors have the greatest impact on profitability.

Create best-case, worst-case and most-likely scenarios to understand the range of possible outcomes and prepare contingency plans.

Combine break-even analysis with key financial ratios like gross margin, operating margin and return on investment for a comprehensive financial picture.

Particularly important for startups, burn rate analysis shows how quickly you’re spending cash and when you’ll need additional funding.

Consider consulting with financial professionals when:

Running a break-even analysis isn’t a one-time exercise:

Julie Thompson and Julianna Lopez contributed to the reporting and writing in this article. Source interviews were conducted for a previous version of this article.