Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Staying on top of your company’s finances isn’t easy. Be aware of these potential obstacles to success and their solutions.

Most small business owners wear several hats: marketing manager, human resources (HR) director and customer service representative, among many others. However, managing the company’s business accounting is perhaps the most significant challenge many small business owners face.

Small business accounting involves recording, summarizing and analyzing your business’s financial transactions. While navigating your business’s finances isn’t always easy, understanding common problems and their solutions is well worth the effort — and can make the difference between a business that survives and one that doesn’t.

Editor’s note: Looking for the right accounting software for your business? Complete the questionnaire below to have our vendor partners contact you with free information.

Here are the top 12 accounting challenges most entrepreneurs face and some accounting tips that can help you overcome them.

Poor cash flow management can be deadly for small businesses. Many small business owners find it challenging to earmark funds to cover recurring costs and keep the business alive.

“Difficulty in tracking the status of invoices and payments can result in a lack of visibility into cash flow and liabilities,” cautioned Paul Wnek, founder and CEO of ExpandAP. “For example, inefficient [accounts payable] processes can lead to higher processing costs per invoice, including labor costs and potential penalties.”

Solution: To stay on top of cash flow, analyze your bills carefully and stay diligent about collecting customer payments. A robust accounts receivable process is key. You should also monitor your monthly expenses closely and cut business costs wherever possible. If you have equipment you no longer use, consider selling it to generate cash quickly.

If a retail store earns $150,000 per year after expenses, it may seem to be in good shape. It probably is ― until an unexpected expense or emergency arises.

For example, say an employee slips and falls at work, and your business doesn’t have adequate workers’ compensation insurance coverage. The medical costs and potential lawsuits could easily cost your business over $1 million.

Even smaller surprises — like a one-time government tax on all businesses in a particular area or a vendor’s sudden price hike — can take a significant toll on your bottom line. “Based on this volatility, it is challenging for small business owners to put aside money for a ‘rainy day,’ such as unexpected expenses,” said Dave Bunce, head of finance and operations at xGrowth.

Solution: Optimize your existing credit to manage short-term expenses and monitor long-term profitability to ensure cost increases don’t threaten your liquidity. Bunce also advised businesses to build savings specifically for rainy-day expenses.

“I typically recommend [allocating] a certain percentage of all cash inflows to a savings account with a target of [2 to 3] months of expenses in it to have the necessary reserves to handle unexpected expenses,” Bunce said. “By having it in a separate account and a disciplined allocation approach, it reduces the temptation to extract any excess cash in the operating account when times are good.”

For many small businesses — especially those offering securities or seeking outside investment — keeping up with financial disclosures required by the U.S. Securities and Exchange Commission (SEC) can be a major challenge. But, even for businesses that don’t report to the SEC, accurate financial reporting is essential in case of a tax audit or financial review. Lenders, investors and tax authorities all expect well-documented records at various stages of business growth.

“The most significant challenge isn’t actually the measurement of metrics, it is deciding what the metrics are going to be,” Bunce noted. “This takes the form of knowing what information is needed for each stakeholder and where the data will be coming from.”

Solution: To meet reporting requirements and avoid issues during a review, consider outsourcing some of the work. Hire a bookkeeper or accountant who specializes in small business finances to help keep your books accurate, organized and stakeholder-ready.

Federal and state taxes are stressful for everyone, but they can be especially challenging for small business owners. While your business structure determines your tax obligations, most businesses must pay income, unemployment and payroll taxes.

Wnek noted that U.S. corporate taxes are complicated by varying state regulations. “Not only does each state determine its own tax rate, but the rules about what qualifies as a tax credit and what qualifies as a tax deduction vary as well,” Wnek explained. “With state and local tax laws always in flux and more employers hiring remote workers, it’s hard to keep track of which expenses are tax-deductible for businesses and individuals.”

Additionally, small businesses are required to pay estimated quarterly taxes if they expect to owe $1,000 or more when their return is filed. Failing to make those payments on time can result in fines and penalties from the IRS.

Solution: Taking advantage of deductions can drastically reduce your bill come tax day. If your small business is home-based, home office deductions are a crucial consideration. Section 179 of the tax code allows you to deduct the cost of certain business property in the year it’s purchased, and those savings can be reinvested into your company.

One reason taxes are so challenging is that tax laws change constantly. Tax code and policy updates can significantly impact your business — and if you’re not prepared, you could end up overpaying at the end of the year.

Solution: Again, professional help can be critical. Consider hiring a certified public accountant (CPA) to manage your taxes. CPAs stay up-to-date on tax laws and can advise you on how to use those rules to your advantage.

Playing the role of an HR or payroll expert is incredibly challenging, but there’s little room for error. HR and payroll mistakes come with serious consequences. For example, if you don’t correctly classify new employees, you could incur costly penalties. Additionally, you must ensure taxes are filed correctly; pay employees accurately each pay period; properly track employee time off; and deal with a host of HR compliance challenges.

Solution: The best online payroll services can remove many of these headaches for your small business. Check out our review of Paychex and our Gusto review to learn about affordable payroll services that can handle HR functions.

Business owners and professionals must track receipts and recurring expenses to claim them as small business deductions. These deductions reduce your taxable income and help you better understand your company’s profits and losses. However, the IRS requires documentation — and it’s easy to misplace receipts or forget to track certain expenses.

Solution: Today, financial tracking tools help you digitize receipts and record recurring expenses. Additionally, many excellent accounting software platforms can help you create a paperless office and digitally store all documentation.

Reconciling your books can be grueling — especially without reliable accounting software to lean on. It’s easy to make accounting mistakes that lead to inaccurate data, and that risk increases for small business owners who don’t have a formal accounting background.

“Most small business owners became business owners because of their expertise or skillset in a particular industry or service and do not have formal training or experience in business,” Bunce noted. “In other words, they are learning to fly the plane while it’s already in the air.”

Making sound financial decisions involves three steps: interpreting, analyzing and advising. Regardless of the reports you use, generating the numbers is only the first stage. What do those numbers mean? More importantly, how do you improve them?

Solution: Take a multipronged approach to solving this problem:

Every time you expand your business’s online presence, you also increase the risk of being targeted by cybercriminals. And it’s not just large companies that need to watch out — hackers often go after small businesses because they typically have weaker cybersecurity and risk management protocols.

A single breach can cost your business hundreds of thousands of dollars and do lasting damage to your reputation. Businesses of all sizes must take cybersecurity seriously.

Solution: Run a cybersecurity risk assessment to determine your business’s level of vulnerability. Consider working with a cybersecurity professional to evaluate your systems, identify weaknesses and develop a plan to address them.

When it comes to your business’s accounting, trying to do it alone can be costly. You may be an expert on your business, but that doesn’t mean you’re a bookkeeping expert.

Solution: Hiring a skilled accountant ensures your books are accurate and up-to-date. A second set of eyes can reduce errors, uncover cost-saving opportunities and free up your time so you can focus on growing your business.

Many businesses offer remote work plans and appreciate the productivity benefits. However, telecommuting can create accounting headaches — especially when it comes to tax compliance. For example, if an employee doesn’t disclose that they’re working out of state, you may unknowingly fail to withhold the correct payroll taxes and face penalties if you’re audited.

Solution: You may need to consider adopting a new remote work policy for your employees. If necessary, find ways to track your employees’ work locations so you know you’re meeting tax requirements.

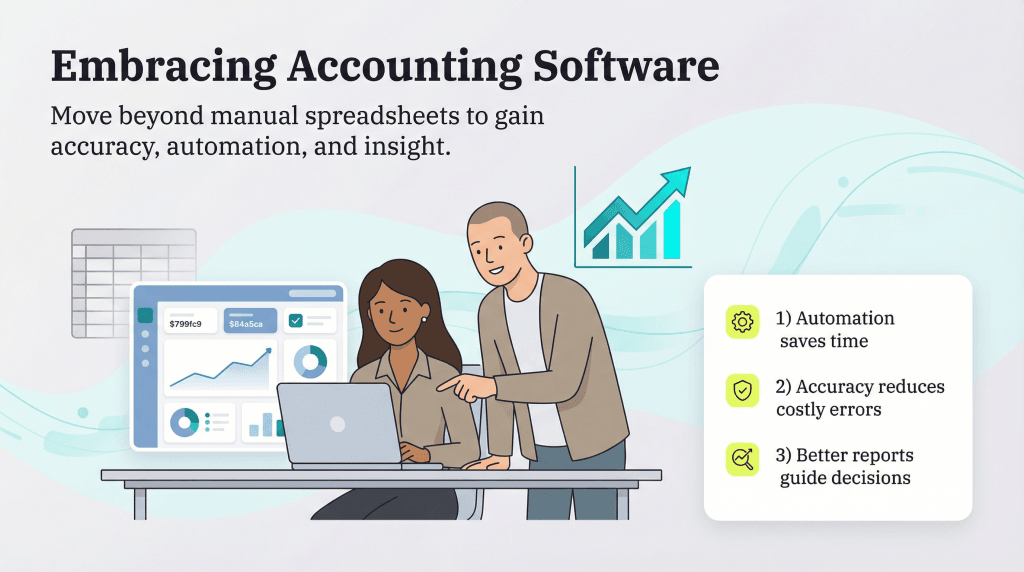

Some business owners still rely on old-school spreadsheets that have served them well for years. But sticking to manual methods can actually hold your business back, increase risk and limit your company’s growth.

If accounting software feels like an unnecessary expense, consider the time and money it can save in the long run. Increased accuracy can help you avoid fines and penalties, while automation frees up your time to focus on other priorities.

“Yes, implementing a new system requires training time and has a cost, but what is the cost savings over time?” Bunce said. “Is it not needing to hire another accounting clerk as the company grows? Is it more intangible, like being able to get better reporting and information in order to make better decisions?”

Business owners often hesitate to switch systems, but those who do usually see the benefits quickly. “It’s a lot like embracing any new kind of technology when you are simply used to doing things a different way,” noted Adam Hamilton, CEO of REI Hub. “I think a lot more people and businesses would embrace accounting software if they realized just how beneficial and easy it is.”

Solution: Choosing the right accounting software can be a game-changer. Look for a platform with features that suit your business without overwhelming your team. Learn it, train your staff and take advantage of its full potential.

“One way to get past this challenge is simply by talking to colleagues from other small businesses who use this kind of software,” Hamilton said. “Ask them their honest opinion, what they like [and] dislike, and if they would recommend a particular platform. The more anecdotal research you can do, the easier it can become to fully see the benefit accounting software might provide your business.”

Amanda Hoffman contributed to the reporting and writing in this article. Source interviews were conducted for a previous version of this article.