Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Tracking your finances allows you to keep tabs on the money coming in and going out of your business. It also helps you identify ways to grow your enterprise.

Tracking your business’s finances helps you cut costs, understand your tax liability and identify growth opportunities. Having a clear idea of how money moves in and out of your company ensures you don’t face a shortfall later on. This guide covers the basics you need to know about financial tracking, including accounting methods, best practices and tools to support you.

Financial tracking, also known as expense tracking, is the process of keeping tabs on your income and spending — ideally on a daily basis. It’s achieved by recording receipts, invoices and business expenses on an accounting ledger. Tracking your finances goes hand in hand with creating a business budget.

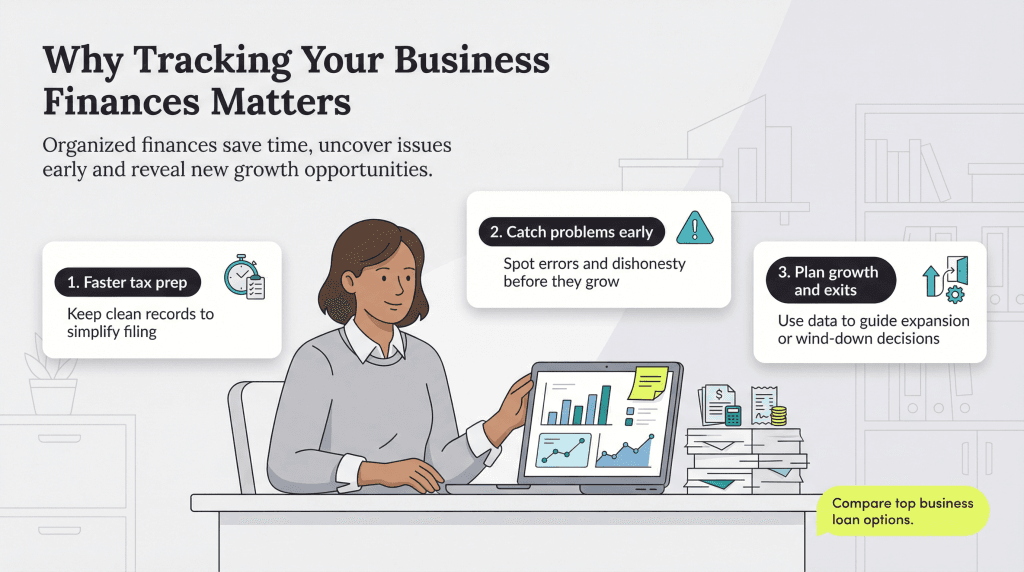

Over time, financial tracking will give you a clear picture of how cash is moving in and out of your business. This practice enables you to increase cash flow, forecast your finances, find ways to slash business costs and identify growth opportunities. It can also help you apply for a business loan, curtail employee fraud and prevent you from scrambling at tax time.

Without financial tracking, “you will have no idea of whether you are making a profit or have a loss,” Maxine Stern, a former business mentor for Chapel Hill-Durham SCORE, told business.com. “I’ve had clients who think they are making a profit but, for various reasons, didn’t see they were losing money. If they were tracking expenses, they would have noticed.”

Editor’s note: Looking for the right accounting software for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

Tracking finances may seem like a no-brainer, but it can easily fall by the wayside for time-crunched small business owners. That can be disastrous for your business — both now and in the future. Finance tracking reduces the time it takes to prepare for taxes and allows you to identify potential issues quickly, which keeps employees honest. Financial tracking is vital to identifying profitable growth opportunities, creating an exit strategy for businesses that aren’t performing well and managing expenses.

You have several options for tracking finances. Some small business owners prefer to track expenses and income the old-fashioned way: via pen and paper. But, most businesses use technology.

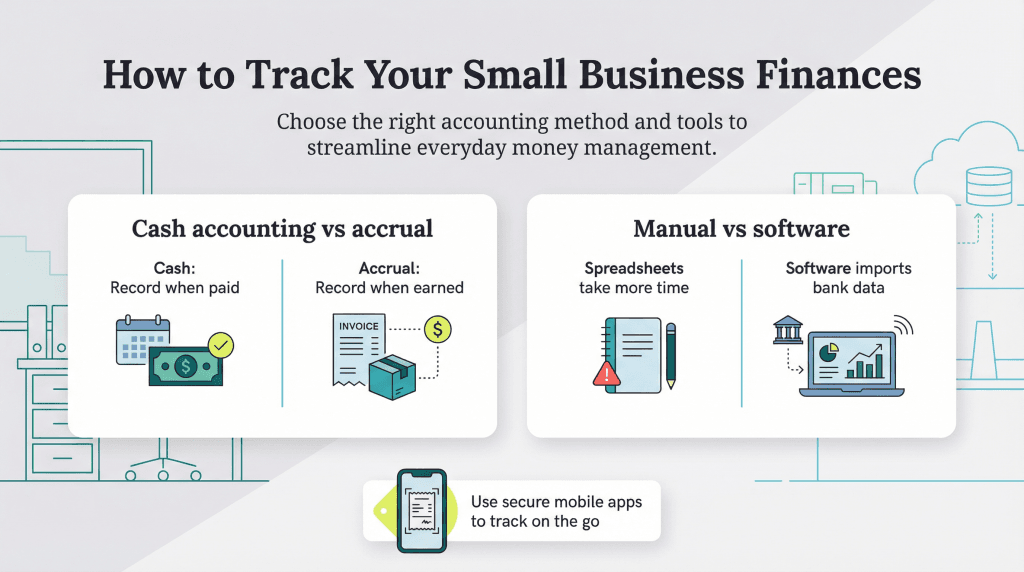

Before you begin budgeting and tracking your finances, you must choose whether to use a cash-basis or accrual-accounting method.

With cash accounting, you record transactions as they occur. As soon as a payment is received, you recognize it as income. The same concept applies to business expenses. When you make a payment, you record that transaction as an expense. Cash accounting is best for freelancers, sole proprietors and very small businesses that don’t have inventory.

Accrual accounting often makes more sense for small businesses that carry inventory and/or get paid after a service is provided. With this accounting method, you record income as soon as the product is sold or the service is performed — even if you haven’t received payment yet. You record an expense when you receive the bill, not when you pay it.

One benefit of accrual accounting is that it tells you precisely how much money you make and spend in a certain time frame. That information gives you insight into when your business is busy and slow; this knowledge helps you project further out than you could with a cash-accounting method.

“Most small businesses start off with cash accounting, and as they grow and get bigger, they move to accrual accounting,” said Robert Smith, managing director at accounting and tax advisory firm CBIZ & MHM.

After you choose an accounting method, you must decide if you’ll do the financial tracking yourself or use software. Tech-averse small business owners may prefer a manual process, while others will likely turn to accounting software or a mobile app.

Small business owners who don’t want to purchase accounting software can use top spreadsheet software, such as Microsoft Excel or Google Sheets. However, remember that using a spreadsheet is more time-consuming and prone to errors. Accounting software is generally more efficient and accurate.

Once you choose an accounting software or application, consider connecting your financial institutions with the software. This makes tracking your income and expenses much more manageable than it would be if you had to input every transaction manually.

When you share financial information with an application, be mindful of the software’s security level; the last thing you want is for your small business’s financial information to fall into the wrong hands. Make sure the software vendor follows best practices for cybersecurity.

Some accounting software makers also provide mobile apps, which you can use to run your business from a smartphone. A mobile component will enable you to input expenses and income on the go; that can mean snapping a picture of a receipt or inputting income after you leave a winning sales meeting. Not all accounting software offers a mobile app, but it will become a budget lifesaver if you are out of the office often.

One of the best ways for small business owners to ensure they track finances accurately is to keep personal expenses separate from business ones.

“You want to have a totally separate bank account, or otherwise it’s just bad business,” Stern said. “You won’t be able to see what’s happening to your business.”

While a pen and paper may seem sufficient for very small businesses or sole proprietors, accounting software and apps are better options. These tools represent a financial investment. But, they can end up saving you time and money while also supporting your financial tracking with useful features.

Many accounting software platforms allow you to create customized reports. Streamlining your finance tracking may require some upfront work, but creating standard templates will save time in the long run. Also, it will reduce the likelihood of accounting mistakes.

With a business credit card, you can track your business expenses with ease. Furthermore, you may be able to earn valuable rewards, such as cash back and travel points. As long as you use business credit cards responsibly and always repay your balances on time, these tools can also improve your business credit score. Before you apply for a business credit card, shop around and explore all your options. This way, you can zero in on the best cards for your business.

It’s a good idea to design a clear expense policy so that everyone is on the same page with what constitutes an acceptable expenditure. Your expense policy should meet your company’s unique needs. But, you’ll want to outline what is considered a valid business expense, set limits for certain expenses and explain the acceptable methods for business purchases. Don’t forget to clarify reimbursements so employees know how they’ll get reimbursed for business expenses.

While it may be tempting to simply ignore receipts or toss them, doing so can be problematic in the long run. By keeping tabs on your receipts, you’ll be able to track and claim your business expenses. This practice can ensure proper tax filing and even help you lower your tax bill; the receipts may also come in handy in the event of an audit. The IRS requires that you keep business documents, including receipts, for at least three years.

You can’t just set up finance tracking and then forget about it. You should comb over your finances regularly to spot any inconsistencies that raise red flags or point to inefficiencies that could be streamlined.

“You want to close your books every month and start fresh,” Smith said. “If you’re tracking your expenses monthly, you will know how you are doing and can make changes in real time.”

The reality is that federal rules and laws are not set in stone. In fact, they change all the time. These regulations can impact the way you track your business finances and file your taxes. So, it’s important to stay current on them. A reputable financial planner or accountant can help keep you in the know and answer any questions that may pop as new laws come about.

Several tools are available to help small businesses track their income and expenses. Here are a few common financial tracking solutions and their benefits:

The cheapest way to keep track of your money is through Google Sheets. This spreadsheet program is free to use but has some limitations in the number of cells and columns per sheet. Google Sheets can be an ideal expense tracker if you operate a very small business with one income stream and only a handful of expenses.

Microsoft Excel is another option. It isn’t free, but you probably already have it if you are among the legions of business owners who use Microsoft’s suite of productivity tools. Excel is an attractive option for businesses because it is easy to use and many people are familiar with it. With Excel, you can track finances, run reports, and set up templates and formulas that are unique to your business.

Whether based in the cloud or installed locally on a computer, accounting software enables small businesses to automate many finance-tracking processes. With accounting software, you can send one-time invoices or schedule them at regular intervals, send automated payment reminders, and reconcile your bank transactions. This software also generates financial reports, giving you an overall picture of your financial position.

There are many accounting software programs to choose from, such as:

The best accounting software programs also offer mobile apps, which give you the flexibility of accessing your financial data from any mobile device. Mobile apps may not provide all of the bells and whistles that accounting software offers. But, if you’re looking for a quick and easy way to stay on top of the money coming in and going out of your business anytime and anyplace, these tools can be useful.

Anna Baluch contributed to this article. Source interviews were conducted for a previous version of this article.