Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Learn how general ledger accounting can help you gauge your business's overall financial health.

As a busy business owner, you may not have much interest in basic accounting principles, such as maintaining a general ledger. While most accounting activities are best left to your accountant, understanding what a general ledger is and how it works can be beneficial.

Maintaining a general ledger is one of the best ways to gauge your business’s overall financial health. It also helps ensure you’re not making any typical accounting mistakes that could cost you time and money down the road.

Editor’s note: Looking for the right accounting software for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

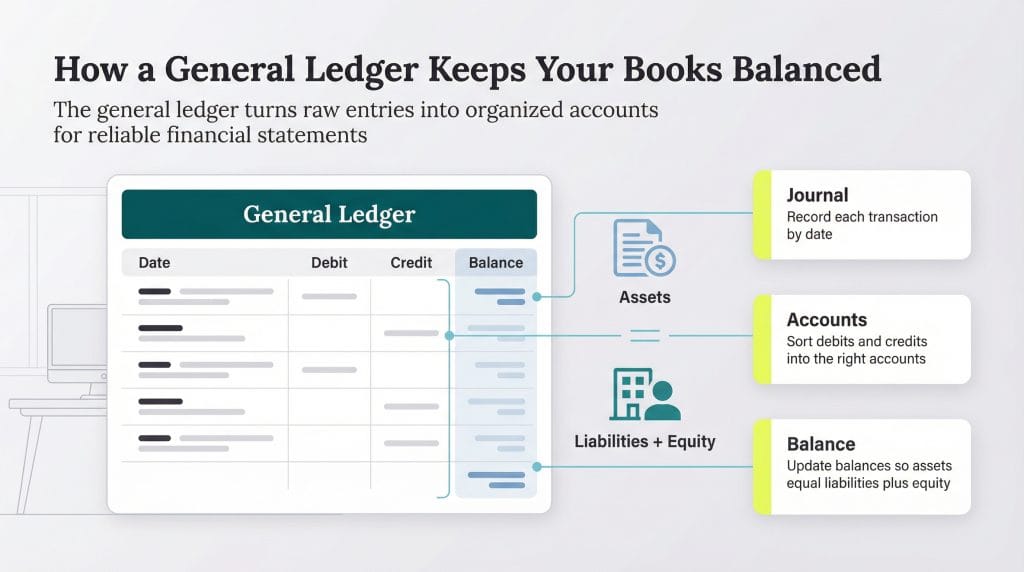

A general ledger is a record of a company’s financial transactions. General ledger accounting summarizes and sorts a company’s financial information. Most businesses track this financial accounting data with accounting software.

“A general ledger is a master record that contains all the accounts used by a company or organization,” explained Max Avery, co-author of Wealth in Numbers and chief business development officer at Digital Family Office. “These accounts include assets, liabilities, equity, revenue and expenses.”

A general ledger includes the following:

Avery explained that a general ledger outlines all transactions and sorts them by type. “For instance, if a company purchases a new piece of equipment, that transaction will be recorded in the general ledger under the asset account for equipment,” Avery noted. “If the company takes out a loan, it will be recorded in the liability account.”

Companies use general ledger data to compile their financial statements and track business performance.

Businesses use general ledgers as part of the accounting process. Without a detailed general ledger, your accounting can quickly become disorganized and inaccurate. Inaccurate financial records cause significant problems down the road.

A general ledger provides the information necessary to create a balance sheet or cash flow statement and gives a quick overview of your organization’s financial health. A general ledger also creates a comprehensive audit trail, which will be helpful if you ever face a tax audit.

“The general ledger is essentially the backbone of any accounting system,” explained Dana Ronald, president of the Tax Crisis Institute. “It’s where all the financial transactions of a business are compiled — think of it as the master file that records everything. Every expense, every sale and every transfer is logged in the general ledger, forming the basis for the business’s financial reports. It provides a clear, organized record that keeps you aware of your income, expenses, assets and liabilities.”

There are four primary components of a general ledger:

To get started, create a journal and record each business transaction as it occurs. Ensure each transaction is assigned to the correct account. Once your journal is complete, transfer the data to the general ledger.

A general ledger takes information from the journal and categorizes it into the appropriate accounts. Each entry may also include subaccounts to provide further transaction details.

For instance:

Double-entry bookkeeping states that every financial transaction affects a company’s finances in two ways. The following equation summarizes this concept:

Liabilities + Equity = Assets

In a double-entry system, a company’s total assets must equal the sum of its liabilities and the owner’s equity. This ensures that the balance sheet stays balanced every time and that each debit has a corresponding credit.

“Double-entry bookkeeping is a system built for accuracy,” Ronald said. “Every transaction has at least two entries: a debit in one account and a credit in another, ensuring everything balances — what comes in equals what goes out. For example, buying business equipment means debiting the equipment account (asset) and crediting the cash account. This balance adds consistency and reliability to your financial records.”

The key principle of double-entry bookkeeping is that every transaction affects at least two accounts. For example:

Double-entry bookkeeping ensures the business maintains accurate records with a corresponding relationship between each liability and asset.

General ledgers help generate financial statements for financial institutions or stakeholders. They can also help you understand and track your business’s finances. Here are a few ways they do this:

A general ledger is used to record your business’s financial transactions. Here are some examples of common general ledger entries:

Here is an example of what a general ledger entry would look like:

Date | Transaction number | Transaction | Debit | Credit |

|---|---|---|---|---|

1/15/26 | 1001 | Office Supplies | $350 | BLANK |

1/15/26 | 1001 | Cash | BLANK | $350 |

2/1/26 | 1002 | Accounts Receivable | $5,500 | BLANK |

2/1/26 | 1002 | Sales Revenue | BLANK | $5,500 |

2/28/26 | 1003 | Salaries Expense | $8,200 |

BLANK |

2/28/26 | 1003 | Cash | BLANK | $8,200 |

3/10/26 | 1004 | Cash | $5,500 | BLANK |

3/10/26 | 1004 | Accounts Receivable | BLANK | $5,500 |

3/22/26 | 1005 | Equipment | $12,000 | BLANK |

3/22/26 | 1005 | Accounts Payable | BLANK | $12,000 |

4/5/26 | 1006 | Rent Expense | $2,400 | BLANK |

4/5/26 | 1006 | Cash | BLANK | $2,400 |

As shown in this example, purchasing inventory impacts both the debit and credit columns. The inventory purchase increases assets (debit), while cash decreases (credit) to reflect the transaction.

Most businesses use feature-rich accounting software to manage their general ledger efficiently.

“Using accounting software to manage a general ledger boosts efficiency and accuracy,” Ronald noted. “It automates tasks, reduces errors and ensures compliance with standards. Advanced tools also generate real-time reports, perform analytics and integrate with other systems for smooth financial management.”

When choosing accounting software, ensure the solution supports general ledger accounting. Here are some excellent options:

“Accounting software automates the double-entry bookkeeping process, making it easier and less time-consuming to record transactions,” Avery explained. “Accounting software also allows you to generate financial reports instantly, giving you a real-time view of your business’s financial performance. [Many] programs offer features such as budgeting and forecasting, helping you make strategic decisions based on your financial data.”

Amanda Clark contributed to this article.