Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Track your finances, catch discrepancies early and keep your business financially healthy.

Keeping up with financial tracking is essential to running a healthy business. When you know exactly where your money is coming from, where it’s going and how each transaction affects your bottom line, it’s much easier to make smart decisions and spot potential issues before they become bigger problems.

That’s where the accounting cycle comes in. When you follow a consistent accounting cycle, your financial records stay organized, accurate and easy for internal stakeholders, investors and lenders to review. The accounting cycle follows each transaction from the moment it happens to the point it’s reflected in your financial statements. Whether you’re managing the process manually or using accounting software, the cycle helps track money coming in, money going out and how those transactions affect your business over time.

Below, we’ll explain how the accounting cycle works and break down each step of the process.

The accounting cycle is a structured process for identifying, recording and maintaining your company’s financial transactions. This work is often handled by a bookkeeper or accountant who documents, categorizes and summarizes each transaction your business makes during a specific accounting period.

That period can vary depending on your business model, industry and reporting needs. However, many businesses start a new accounting cycle at the beginning of each fiscal year.

Once the accounting period ends, the books are closed and financial statements are prepared to summarize what happened during that period. Those records may be reviewed internally, shared with investors or lenders, or used to support tax filings and other financial obligations.

“[The accounting cycle] ensures that all financial activities are accurately captured and reported in the company’s financial statements,” explained Paul Ursich, partner-in-charge of advisory services at Wiss & Company. “The steps include identifying transactions, recording them, posting to the ledger, preparing a trial balance, making adjustments, preparing financial statements, and closing the books.”

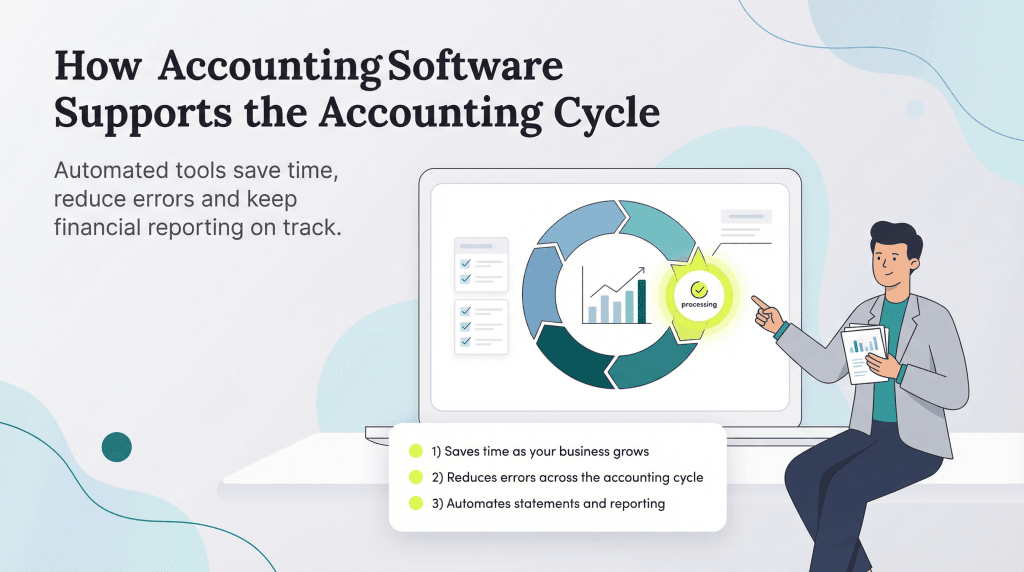

Many businesses now use accounting software to automate much of the accounting cycle, reducing the manual data entry that can lead to accounting mistakes like bookkeeping errors, missed transactions or inaccurate asset tracking.

It’s easy to confuse the accounting cycle with the budget cycle. While both rely on similar financial data, they serve very different purposes in your business.

In short, the accounting cycle looks backward, while the budget cycle looks forward. Following a consistent budget cycle can help your business make smarter financial decisions, control costs and put resources where they’ll have the biggest impact.

The exact steps of the accounting cycle can vary depending on a company’s size, industry and specific needs. That said, the core process for tracking financial activity and producing accurate financial statements remains consistent. Here’s a breakdown of each step.

The first step in the accounting cycle is identifying every transaction that creates a financial event in your business. These events can include sales, refunds, bill payments through accounts payable and any other activity that affects your finances.

“Although this step sounds simple and somewhat mundane, it is one of the most critical steps of the accounting cycle,” said Ashford Chancelor, founder of Great Shift, a strategic foresight and advisory platform. “Identifying transactions and classifying them correctly in this initial stage is a key step that will reduce the time needed in the reconciliation and review stages before the financial statements are issued.”

In accounting, transactions usually fall into one of three buckets: cash, noncash or credit events. Businesses typically spot these through invoices, receipts, bank records and other source documents that reflect what’s happening day to day.

“For many companies, cash receipts and disbursements comprise a significant portion of the transaction volume,” Chancelor explained. “To facilitate accurate and swift identification, many companies will establish specific email addresses to which vendors will send invoices to be paid or separate bank accounts to receive payments for a predetermined purpose.”

Next, document each transaction as a journal entry. The journal (often called the “book of original entry”) is the book, spreadsheet or software record where transactions are first recorded.

Each entry should include key details about the transaction in chronological order. If your company uses double-entry accounting, every entry will include both a debit and a credit. This method makes it easier to track how each transaction affects your accounts, cash flow and overall financial picture.

After you enter transactions into the journal, the next step is posting them to your general ledger. Posting moves those chronological journal entries into the general ledger, where they’re grouped by account type instead of by date.

Transactions in the general ledger are typically organized into five key accounts:

Organizing transactions this way makes it much easier to review activity, spot discrepancies and find specific entries when needed. And if your debits and credits don’t balance, it’s a strong sign something needs to be reviewed before your financial statements are finalized.

Once journal entries are posted to the appropriate general ledger accounts, it’s time to prepare an unadjusted trial balance. This report is used to review account balances and confirm that total debits and credits in the ledger are equal.

“A trial balance is an accounting report that lists the general ledger account balances at a specific time,” Chancelor said. “It is used to generate the balance sheet, income statement and statement of cash flow and is also a primary control used to ensure that the total debits equal the total credits. A trial balance helps identify errors in the general ledger before financial statements are prepared.”

To create an unadjusted trial balance, list all general ledger account balances before making any adjusting entries. It gives you a quick read on where your books stand and can help you catch small issues before they snowball into bigger ones later in the accounting cycle.

While you can prepare a trial balance manually, most modern accounting software platforms handle this step automatically, making the process faster and reducing the chances of manual entry errors.

This step matters whether your trial balance is out of balance or something just feels off. To track down the issue, compare any entries that raise questions with the original journal entries in your spreadsheet, accounting software or supporting records.

One common mistake is posting a transaction to the wrong account. In those cases, your debits and credits may still balance, but a number might show up where it doesn’t belong or an account may suddenly look unusually high or low. This is where you slow down, dig into any discrepancies and make sure your books are clean before moving on.

As the accounting period winds down, you’ll need to record adjusting entries in your journal. These end-of-period updates help make sure your accounts reflect the revenue you’ve earned and the expenses you’ve actually incurred during that stretch of time.

Adjusting entries often include prepayments, accruals and noncash expenses such as depreciation. This step is especially important for transactions that span multiple accounting periods — for example, a 12-month software subscription paid upfront that needs to be recognized a little at a time over the months it actually covers.

Now that your adjusting entries are recorded, it’s time to prepare an adjusted trial balance and complete your financial statements. The adjusted trial balance lists the final balances for each general ledger account after all end-of-period updates have been made.

Once that’s done, you can generate financial statements that pull all of your financial data into one organized, easy-to-read set of reports. Tax authorities, investors, lenders and other stakeholders may review these documents to see how your business is performing, how healthy your finances look and whether anything needs a closer look.

The three major financial statements are the balance sheet, income statement and cash flow statement. Together, these reports show where your business stands financially and can reveal how effectively it’s operating.

After your financial statements are prepared, it’s time to officially wrap up the accounting period. This step involves recording closing entries to finalize your revenue and expense accounts.

The closing process typically transfers your net income to retained earnings or another appropriate equity account. Once that transfer is complete, all temporary accounts — including revenue and expense accounts — should be closed.

“Closing the books resets revenue and expenses back to zero so that they don’t carry over to the next accounting period,” Chancelor explained. “Net income or loss is transferred to a permanent account that records retained earnings.”

The final step is preparing a post-closing trial balance to make sure your debits and credits still line up before the next accounting cycle begins. At this point, temporary accounts have been reset to zero, so this report includes only balance sheet accounts — giving you a clean set of numbers to work from when the next period rolls around.

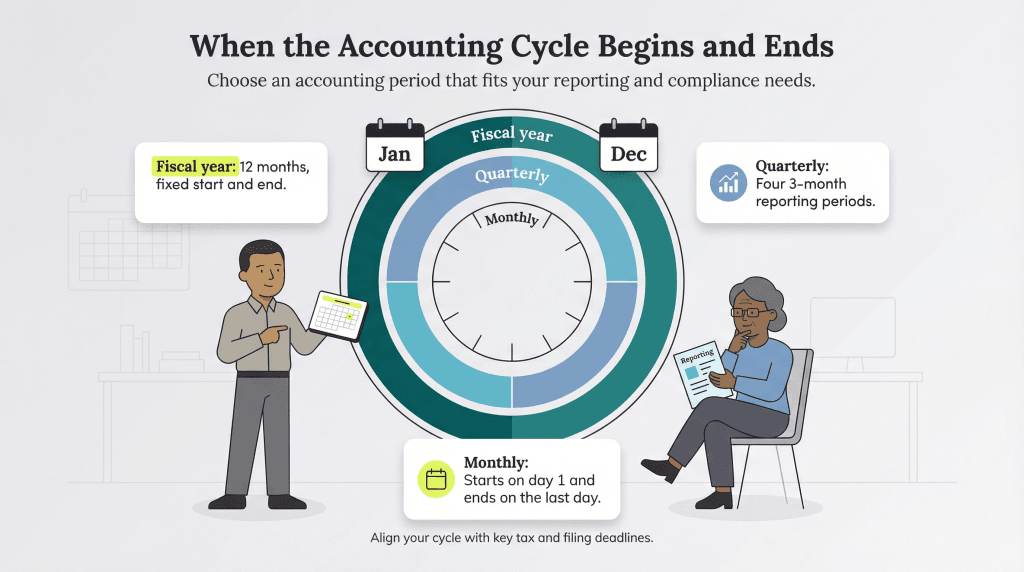

The length of an accounting cycle depends on the accounting period your business chooses based on its reporting, tax and operational needs. During each cycle, financial transactions are recorded, reviewed and ultimately turned into financial statements.

Many businesses complete a full accounting cycle annually for tax, reporting and compliance purposes. However, others close their books more frequently using quarterly, monthly or even semiannual accounting periods.

In the U.S., businesses aren’t required to follow a traditional calendar year for tax and reporting purposes. Many companies use a fiscal year that starts and ends on dates that make sense for their operations, and some even use a 52-week fiscal year instead of following the calendar exactly — a setup that’s especially common in seasonal industries like retail, hospitality and manufacturing.

Here’s how Ursich described fiscal year, quarterly and monthly accounting cycles:

Accounting software can take much of the manual work out of the accounting cycle. As your business grows, handling every step by hand becomes harder to manage — and much easier to get wrong. Investing in one of the best accounting software platforms can help you work more efficiently, reduce errors and keep long-term accounting costs in check.

Even if you work with a CPA or hire a bookkeeper to oversee your accounting cycle, the right software can still take a lot off your plate. These tools can record transactions, organize financial data and automatically generate key financial statements. A reliable platform can also help your team avoid costly mistakes and stay on track with reporting as your business grows.

Amanda Hoffman contributed to this article. Source interviews were conducted for a previous version of this article.