An efficient accounts payable (AP) process is a necessity for any business as it ensures that vendors and suppliers are paid on time and reduces waste by eliminating late fees and duplicate payments. This article will explain how the AP process works and the differences between AP and accounts receivable (AR). We’ll also show you how to set up your own AP process.

Editor’s note: Are you looking for the right accounting software for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

What are accounts payable?

Accounts payable are the payments due for goods or services purchased from a vendor or supplier. You can track these liabilities on a balance sheet to monitor outstanding payments and ensure no overdue balances.

Payment due dates vary, so check individual invoices to verify the dates. If payments aren’t made on time, your company could get hit with late fees.

An AP term you may hear frequently is “days payable outstanding” (DPO). This financial ratio measures the average number of days a company takes to pay its vendors or suppliers. The longer it takes you to pay your suppliers, the higher your DPO.

Accounts payable are considered liabilities because they represent money your business owes. This differs from accounts receivable, which are typically considered

business assets.

AP vs. AR

It’s easy to confuse AP with AR, the latter of which involves collecting unpaid invoices. While there’s some overlap, AP and AR aren’t the same.

Accounts payable are the money your business owes its vendors and suppliers for goods and services purchased. In contrast, accounts receivable are the money owed to your company, usually by its customers. While accounts payable are considered liabilities, accounts receivable are assets.

Both AP and AR are crucial aspects of the accounting cycle and work together to ensure your business functions smoothly. Both should be recorded to ensure accuracy and to track when outgoing and incoming payments are due. Without bringing in a profit, your company will be unable to meet its financial obligations.

Examples of AP

Here are a few examples of AP:

- Equipment

- Leases

- Subcontracting services

- Raw materials

- Travel

- Supplies

There are two types of payables in

business accounting: Trade payables and expense payables. Trade payables represent the purchase of physical goods, while expense payables refer to the purchase of expensed services, such as travel or supplies.

What is an AP process?

An AP process is the steps a company takes to pay its suppliers and vendors for any goods or services it purchased. Here’s an overview of how the process works from start to finish:

- Receiving the invoice: The first step in the AP process happens when your company receives an invoice. The invoice details all relevant information about the transaction, including a description of the product or service provided, the amount due and the payment terms.

- Invoice matching: Next, your AP department needs to ensure the invoice is accurate and that there are no discrepancies. AP will check to see that the invoice matches the purchase order and that the company received the goods or services as expected.

- Invoice approval: Once AP has verified the invoice is accurate, it needs to be approved. How long this process takes depends on the size of your company and how complex your workflow is.

- Scheduling the payment: Once the invoice is approved, it’ll be scheduled for payment according to the payment terms. If the vendor offers an early payment discount, this can be a great way to save some money and improve cash flow.

- Reconciliation: Once the payment is made, the AP department will reconcile the transaction to ensure it matches any bank records. Documents like purchase orders or invoices will be saved in case of a future audit.

How to set up an AP process

When you’re setting up an AP system, Paul Wnek, founder and CEO of ExpandAP, said finding the right process for your needs is essential. “The key to ushering in the new age of AP automation relies on finding the right partner and avoiding piecemealing systems,” he explained.

Here’s a step-by-step guide for setting up an AP process.

1. Create a chart of accounts.

First, you must create a chart of accounts to track your transactions. You can easily make one in Excel or accounting software. A chart of accounts should include the following information for each transaction:

- Vendor name

- Account number

- Invoice number

- Invoice date

- Expense type

- Payment deadline and status

2. Set up your vendors.

Next, create a spreadsheet with a list of your vendors. Here, you can detail exactly how each vendor is paid and when the payment is due. Maintaining a solid relationship with vendors will help your business in the long run and ensure no hiccups arise when you’re buying their goods or services.

Make sure you enter the correct payment terms. Some vendors offer discounts if the invoice is paid in full before a specific date. This is referred to as Net D, with the “D” indicating the number of days. The terms will change depending on your agreement with the vendor.

For example, a 2 percent net 30 provides a company with a 2 percent discount if the invoice is paid within 30 days. If your vendors don’t offer this currently, see if it’s an option. It’s an incentive for the company and vendor to ensure smooth, on-time payments.

3. Receive invoices from suppliers.

Once you receive an invoice, review the bill to ensure there are no errors and confirm that all goods have been accounted for. Then, enter the invoice information. The only exception would be if a vendor provided a service instead of a product.

Match the invoice to the purchase order to double-check that everything is correct. Once the invoice is paid, you may be unable to correct the order.

4. Process payments for outstanding invoices.

Check your AP at least once weekly to ensure there are no unpaid invoices. You want to stay on top of payments to avoid penalties on unpaid invoices, such as interest and late fees. There are many ways to pay your invoices, so it’s always best to see which method a specific vendor prefers.

“The whole idea is based on creating a clear system,” said Paul Carlson, managing partner at Law Firm Velocity. “Create a list of your vendors or service providers and what you usually order from them. Next, when you get an invoice, check it against what you ordered. This is called a three-way match — invoice, purchase order and receiving report. It helps catch mistakes before you pay.”

Accounting software can help you avoid oversights in making payments. You can also set up payment alerts to ensure you have no outstanding invoices. Any extra step you can take to pay on time is highly recommended.

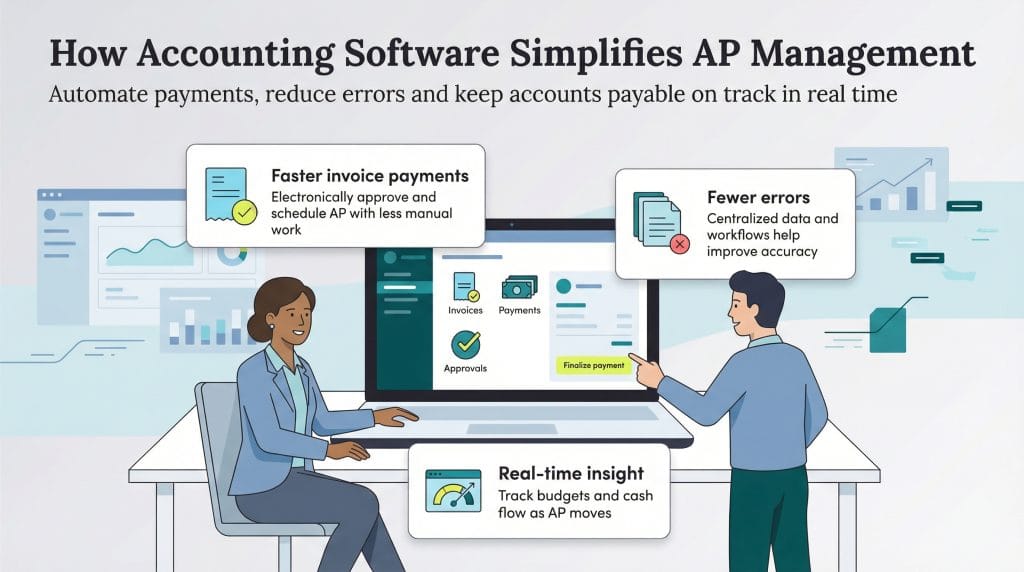

How accounting software can help manage the APs process

Accounting software provides numerous advantages to streamline your AP process:

- Easy invoice payment: Online accounting software makes it easy to pay invoices electronically, thereby helping you avoid past-due penalties.

- Saves time: According to Wnek, accounting software can save you time. “Backend office tasks that require significant time and data entry, such as AP, may be offloaded to programs that can take care of expense reporting and budget tracking to show where the budget is in real-time.”

- Reduced errors: Having all accounting information in one place makes it easier to track and manage your accounts. Handling everything manually leaves a lot of room for human error. “Accounting software can automatically match invoices to purchase orders, so you don’t have to do it by hand,” explained Carlson. “That saves time and cuts down on errors. Plus, a lot of these programs have built-in approval workflows.”

- Automated accounting: Accounting software helps you automate your AP process to avoid late payments. You can also automatically link bank and credit card accounts so you won’t have to input that information manually. “Fraud prevention can also be streamlined through artificial intelligence-identity and document verification services,” Wnek added.

- Electronic record: Accounting software provides an electronic record for reference in case of discrepancies.

Accounting software helps you process payments automatically while avoiding late fees and minimizing common business

accounting mistakes.

An AP process streamlines accounting

All businesses, regardless of their size or industry, should be familiar with the AP process. You must know when outstanding invoices are due to avoid late fees or strained supplier relationships. If you’re creating your own AP process, using the right feature-rich accounting software can help you prevent many common mishaps.