Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Accounts Payable vs Accounts Receivable: What You Need to Know

Accounts receivable is the money your business brings in, while accounts payable is the money your business owes its suppliers and vendors.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Accounts payable and accounts receivable both play critical roles in your day-to-day business operations. Accounts receivable refers to the money your company brings in from the sale of its products and services. In contrast, accounts payable is the money your business owes to suppliers and vendors. We’ll explain how each one works, how they affect your business and how to accurately track this financial data.

Editor’s note: Looking for the right accounting software for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

What are accounts payable?

Accounts payable (AP) refers to short-term debts owed to your suppliers and vendors; these are typically classified as liabilities. “If a business buys something from a vendor but doesn’t pay for it right away, then the money that they owe is called accounts payable,” explained Jackie Rockwell, the co-founder of Brass Jacks, an online bookkeeping academy.

Here are some examples of accounts payable transactions:

Purchase of goods or services from another company

Purchase of raw materials

Travel expenses

Equipment purchases

Leasing

Transportation

There are different types of accounts payable, including the following:

Trade payables

Nontrade payables

Taxes

Loans payable

Wages payable

All of these items (except wages payable) are handled through your accounts payable process. Wages payable is processed separately when your company runs payroll.

It’s essential to stay on top of your accounts payable. Knowing how much your company owes to vendors and suppliers helps you avoid late payments and additional fees.

When recording an accounts payable transaction in your general ledger, you’ll debit the expense account and credit accounts payable. For instance, if your business purchases $500 in office supplies from Staples, your ledger should reflect the following:

Date

Accounts

Debit

Credit

03-Dec-24

Office supplies

$500

N/A

Accounts payable – Staples

N/A

$500

Purchased supplies on account

N/A

N/A

Tip

An automated accounts payable process speeds up invoice approvals and payments and helps keep your cash flow steady.

What are accounts receivable?

Accounts receivable (AR) is money owed to your business by your customers. “[It] is technically a short-term loan or credit line provided to customers so they can buy now and pay later,” Rockwell explained.

Because accounts receivable payments generate future cash flow, they’re considered accounting assets. Managing accounts receivable well means developing a system for billing customers and collecting payments efficiently.

“When a good or service is purchased, it is usually done by cash, debit or credit. If it is done by cash or debit, then the customer receives a receipt [for] the goods or service, and the transaction is complete,” Chapin said. “If the purchase is done by credit, however, then the goods or service [are] provided while the actual payment is delayed and the customer receives an invoice.”

An example of accounts receivable is a phone company billing a customer for monthly cell service. While waiting for payment, the accounting department marks the charge as an unpaid invoice under accounts receivable. Any unpaid sale of a good or service becomes a receivable.

It’s your company’s responsibility to bill customers for services rendered. Your invoice should clearly include the product or service provided, the amount due, sales tax and the due date.

To record accounts receivable, you’ll debit the accounts receivable account and credit your revenue account. When the customer pays, you’ll debit cash and credit accounts receivable.

If the sale involves products, you’ll also need to reduce inventory. For example, if your company completes a $30,000 sale, and $15,000 of that is the cost of inventory, your general ledger would look like this:

Category

Debit

Credit

Accounts receivable

$30,000

N/A

Sales

N/A

$30,000

Cost of goods sold

$15,000

N/A

Inventory

N/A

$15,000

Bottom Line

Keeping accounts receivable up to date helps ensure you collect the money you're owed. If customers aren't paying invoices on time, your business may struggle with cash flow sooner than you expect.

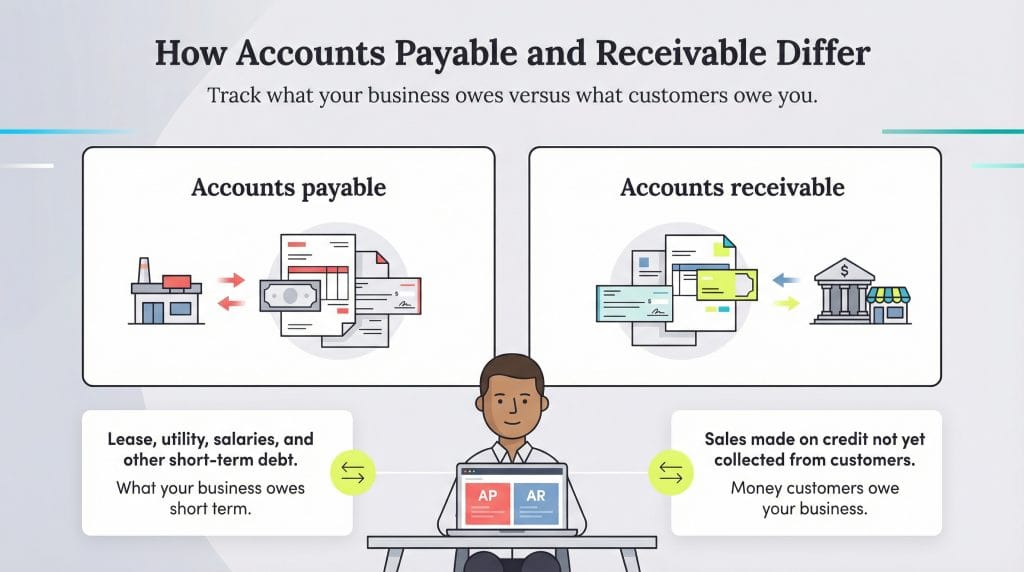

How accounts payable and receivable differ

Accounts payable and accounts receivable are two sides of the same financial coin: One reflects what your business owes, the other what it’s owed.

Accounts payable: AP represents the money your business owes to others, typically suppliers or vendors. It’s considered a liability because it reflects short-term debts that your company is expected to pay.

Accounts receivable: In contrast, AR is the money owed to your business by customers who purchased goods or services on credit. It’s considered an asset, as it reflects future income your business expects to receive.

In other words, accounts payable tracks what your business owes, while accounts receivable tracks what your customers owe you.

Here’s a side-by-side comparison:

Category

Accounts Payable

Accounts Receivable

Definition

Money your business owes

Money owed to your business

Role in accounting

Liability

Asset

Recorded when

You buy something and haven’t paid yet

You sell something and haven’t been paid

Common examples

Vendor bills, utility payments

Client invoices, product or service sales on credit

Impact on cash flow

Money going out

Money coming in

Discounts on accounts payable and receivable

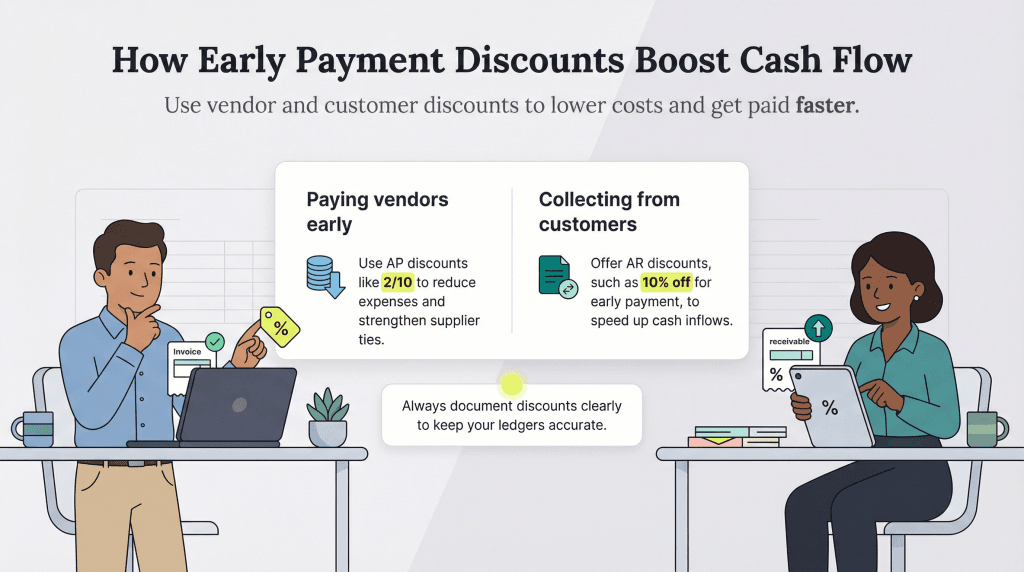

There are benefits to both paying your bills early and collecting early payments.

Paying bills early

Many vendors offer early payment discounts as an incentive to receive cash sooner. If your business takes advantage of these offers, you can cut costs and strengthen supplier relationships. Rockwell explained that discounts vary by industry. “Different industries have different terms that they use for when a payment is due,” Rockwell said. “Some industries will offer discounts if a bill is paid within a specified number of days. So it can be beneficial to a company to pay its bills within that time frame.”

For example, a vendor may offer a 2 percent discount if the invoice is paid within 10 days. These terms are often written on the invoice as “2/10.” Paying early can reduce your expenses and free up cash for other uses, and over time, these savings can make a noticeable impact on your bottom line. Just be sure to record any discounts in your ledger to prevent discrepancies later.

Here’s how you might track a 2 percent discount on a $1,000 vendor payment:

Category

Debit

Credit

Accounts payable

$1,000

N/A

Cash

N/A

$980

Discounts taken

N/A

$20

Collecting early payments

On the accounts receivable side, your business can also offer early payment discounts to customers to incentivize them to part with cash sooner. For example, you might give a 10 percent discount if a customer pays at least a week before the due date. Loyalty discounts are another way to show appreciation to long-term customers.

As with AP discounts, proper documentation is essential. Here’s how you’d record a customer’s early payment on a $1,000 invoice with a 10 percent discount:

Category

Debit

Credit

Cash

$900

N/A

Discount

$100

N/A

Accounts receivable

N/A

$1,000

There are usually guidelines on how to track the discount being offered. For example, if you pay an invoice within 10 days for a 4 percent discount, the notation on the invoice should read “4/10.” Both numbers can change depending on the exact discount and the due date for receiving the discount.

FYI

Offering credit makes it easier for customers to purchase goods and services, helping create goodwill and build customer loyalty.

Tracking accounts payable and receivable

You must track your accounts payable and accounts receivable to truly understand your finances and stay on top of cash flow. Rockwell emphasized the importance of using a schedule to track what is owed and by when. “If you don’t track AP and AR, you might look at your books and not realize how much money you are expecting to bring in or how much money you still owe and need to pay out,” Rockwell explained.

Here are some best practices for tracking accounts payable and receivable:

Monitor cash flow to support forecasting. Accurate tracking makes it easier to forecast your cash flow and plan for upcoming expenses. “You can look at your accounts receivable and see if there is enough money expected to come in to cover what you still owe to your vendors, your payables,” Rockwell said.

Stay organized: To stay organized, save every receipt, invoice and order. If even one invoice slips through the cracks, your records will be off balance. Tracking your financial accounts properly from the start shows professionalism and sets your business up for long-term success. Chapin also noted that sloppy tracking can affect how your business is valued. “Without knowing where all your money is, including those pending transactions coming and going, it will be much more difficult to calculate the value of the company,” Chapin cautioned.

Stay current on due dates: Managing what you owe and what you’re owed ensures payments are made and received on time. “We’ve all witnessed what can happen when payments are late,” Chapin said. “There can be additional fines and fees, but that’s just the start. If a pattern of delinquency develops, or if the sum of the missed payments is large enough, it can result in a loss of trust between people as well as a potentially serious hit to your reputation.”

Watch aging accounts: Keep a close eye on aging accounts — those overdue receivables or payables that can easily slip through the cracks. Addressing them proactively helps you maintain steady cash flow and build stronger relationships with vendors and customers.

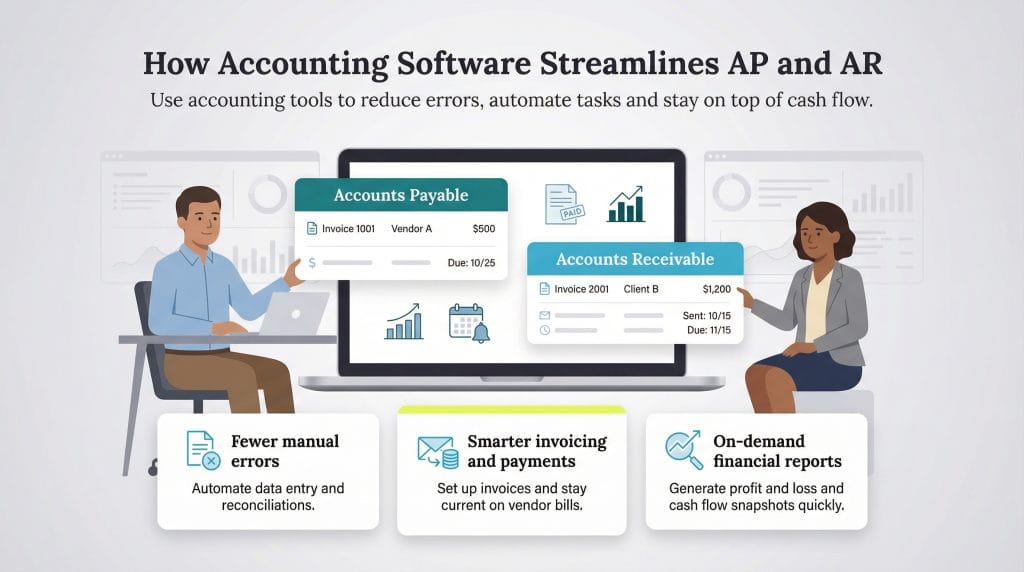

How accounting software can help track accounts payable and receivable

Investing in feature-rich accounting software can make it much easier to manage both accounts payable and accounts receivable. Here are a few key advantages of using accounting software to track your assets and liabilities:

It reduces errors. Accounting software can minimize accounting mistakes by eliminating the need for manual data entry.

You can set up invoices. Most accounting platforms include tools to create professional invoices and track customer information.

You can track vendor payments. Built-in reminders and dashboards help you stay on top of vendor payments and avoid missed due dates.

You can run reports. Accounting software makes it easy to generate daily, monthly or on-demand reports, including profit and loss statements, balance sheets and cash flow statements. These reports are critical for sound financial management. [Learn more about accounts payable reporting.]

In addition to improving accuracy, accounting software can save time by automating some of the more tedious tasks involved in managing AP and AR. The best solution will depend on your business type and size, but most platforms offer customization options to fit your specific needs.

Jamie Johnson has spent more than five years providing invaluable financial guidance to business owners, leading them through the financial intricacies of entrepreneurship. From offering investment lessons to recommending funding options, business loans and insurance, Johnson distills complex financial matters into easily understandable and actionable advice, empowering entrepreneurs to make informed decisions for their companies. As a business owner herself, she continually tests and refines her business strategies and services.

At business.com, Johnson covers accounting practices, budgeting, loan forgiveness and more.

Johnson's expertise is also evident in her contributions to various finance publications, including Rocket Mortgage, InvestorPlace, Insurify and Credit Karma. Moreover, she has showcased her command of other B2B topics, ranging from sales and payroll to marketing and social media, with insights featured in esteemed outlets such as the U.S. Chamber of Commerce, CNN, USA Today, U.S. News & World Report and Business Insider.